Videos

Make or Buy Decision

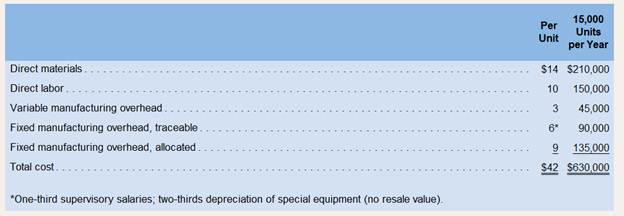

Troy Engines, Ltd, manufactures a variety of engines for use in have equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd, for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally:

Required:

1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (d advantage) of busing 15,000 carburetors from the outside supplier?

2. Should the outside supplier’s offer be accepted?

3. Suppose that if the carburetors were purchased. Troy Engines, Ltd. could use the freed capacity to launch a new product. The segment margin of the new product would be $150,000 per year. Given this new assumption, what would be the financial advantage (disadvantage) of buying 15,000 carburetors from the outside supplier’

4. Given the new assumption in requirement 3, should the outside suppliers offer be accepted?

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Introduction To Managerial Accounting

- Oat Treats manufactures various types of cereal bars featuring oats. Simmons Cereal Company has approached Oat Treats with a proposal to sell the company its top selling oat cereal bar at a price of $27,500 for 20,000 bars. The costs shown are associated with production of 20,000 oat bars currently. The manufacturing overhead consists of $3,000 of variable costs with the balance being allocated to fixed costs. Should Oat Treats make or buy the oat bars?arrow_forwardRolertyme Company manufactures roller skates. With the exception of the rollers, all parts of the skates are produced internally. Neeta Booth, president of Rolertyme, has decided to make the rollers instead of buying them from external suppliers. The company needs 100,000 sets per year (currently it pays 1.90 per set of rollers). The rollers can be produced using an available area within the plant. However, equipment for production of the rollers would need to be leased (30,000 per year lease payment). Additionally, it would cost 0.50 per machine hour for power, oil, and other operating expenses. The equipment will provide 60,000 machine hours per year. Direct material costs will average 0.75 per set, and direct labor will average 0.25 per set. Since only one type of roller would be produced, no additional demands would be made on the setup activity. Other overhead activities (besides machining and setups), however, would be affected. The companys cost management system provides the following information about the current status of the overhead activities that would be affected. (The supply and demand figures do not include the effect of roller production on these activities.) The lumpy quantity indicates how much capacity must be purchased should any expansion of activity supply be needed. The purchase price is the cost of acquiring the capacity represented by the lumpy quantity. This price also represents the cost of current spending on existing activity supply (for each block of activity). Production of rollers would place the following demands on the overhead activities: Producing the rollers also means that the purchase of outside rollers will cease. Thus, purchase orders associated with the outside acquisition of rollers will drop by 5,000. Similarly, the moves for the handling of incoming orders will decrease by 200. The company has not inspected the rollers purchased from outside suppliers. Required: 1. Classify all resources associated with the production of rollers as flexible resources and committed resources. Label each committed resource as a short- or long-term commitment. How should we describe the cost behavior of these short- and long-term resource commitments? Explain. 2. Calculate the total annual resource spending (for all activities except for setups) that the company will incur after production of the rollers begins. Break this cost into fixed and variable activity costs. In calculating these figures, assume that the company will spend no more than necessary. What is the effect on resource spending caused by production of the rollers? 3. Refer to Requirement 2. For each activity, break down the cost of activity supplied into the cost of activity output and the cost of unused activity.arrow_forwardTroy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 15,000 UnitsPer Year Direct materials $ 14 $ 210,000 Direct labor 10 150,000 Variable manufacturing overhead 3 45,000 Fixed manufacturing overhead, traceable 6 * 90,000 Fixed manufacturing overhead, allocated 9 135,000 Total cost $ 42 $ 630,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the…arrow_forward

- Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $36 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 20,000 Units Per Year Direct materials $ 17 $ 340,000 Direct labor 10 200,000 Variable manufacturing overhead 2 40,000 Fixed manufacturing overhead, traceable 9 * 180,000 Fixed manufacturing overhead, allocated 12 240,000 Total cost $ 50 $ 1,000,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying…arrow_forwardTroy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $33 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 18,000 UnitsPer Year Direct materials $ 15 $ 270,000 Direct labor 9 162,000 Variable manufacturing overhead 4 72,000 Fixed manufacturing overhead, traceable 6 * 108,000 Fixed manufacturing overhead, allocated 9 162,000 Total cost $ 43 $ 774,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the…arrow_forwardTroy Engines, Limited, manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Limited, for a cost of $35 per unit. To evaluate this offer, Troy Engines, Limited, has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 14,000 Units Per Year Direct materials $ 14 $ 196,000 Direct labor 10 140,000 Variable manufacturing overhead 4 56,000 Fixed manufacturing overhead, traceable 6* 84,000 Fixed manufacturing overhead, allocated 9 126,000 Total cost $ 43 $ 602,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial…arrow_forward

- Troy Engines, Limited, manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Limited, for a cost of $35 per unit. To evaluate this offer, Troy Engines, Limited, has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 22,000 Units Per Year Direct materials $ 15 $ 330,000 Direct labor 8 176,000 Variable manufacturing overhead 3 66,000 Fixed manufacturing overhead, traceable 3*Footnote asterisk 66,000 Fixed manufacturing overhead, allocated 6 132,000 Total cost $ 35 $ 770,000 *Footnote asteriskOne-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what…arrow_forwardTroy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $32 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Per Unit 17,000 Unitsper Year Direct materials $ 14 $ 238,000 Direct labor 8 136,000 Variable manufacturing overhead 3 51,000 Fixed manufacturing overhead, traceable 3 * 51,000 Fixed manufacturing overhead, allocated 6 102,000 Total cost $ 34 $ 578,000 *One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the…arrow_forwardTroy Engines Ltd manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburettors. An outside supplier has offered to produce and sell one type of carburettor to Troy Engines for a cost of £34 per unit. To evaluate this offer, Troy Engines has gathered the following information relating to its own cost of producing the carburettor internally: Per Unit 16,000 units per year Direct materials £14 £224,000 Direct labour 10 160,000 Variable manufacturing overhead 3 48,000 Fixed manufacturing overhead, traceable 6 * 96,000 Fixed manufacturing overhead, allocated 9 144,000 Total cost 42 672,000 *One-third supervisory salaries, who are directly associated with the manufacturing of the engine; two-thirds depreciation of special equipment (no resale value). Required: 1. Assuming that the company has no alternative use…arrow_forward

- Troy Engines Ltd. manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to produce and sell one type of carburetor to Troy Engines Ltd. for a cost of $91.0 per unit. To evaluate this offer, Troy Engines Ltd. has gathered the following information relating to its own cost of producing the carburetor internally: PerUnit 36,000 Unitsper Year Direct materials $ 21 $ 756,000 Direct labour 24 864,000 Variable manufacturing overhead 17 612,000 Fixed manufacturing overhead, traceable 27.0 * 972,000 Fixed manufacturing overhead, allocated 23 828,000 Total cost $ 112.0 $ 4,032,000 * One-third supervisory salaries; two-thirds depreciation of special equipment (no resale value). Suppose that if the carburetors were purchased,…arrow_forwardMake or Buy Decision Troy Engines, Ltd., manufactures a variety of engines for use in heavy equipment. The company has always produced all of the necessary parts for its engines, including all of the carburetors. An outside supplier has offered to sell one type of carburetor to Troy Engines, Ltd., for a cost of $35 per unit. To evaluate this offer, Troy Engines, Ltd., has gathered the following information relating to its own cost of producing the carburetor internally: Required: 1. Assuming the company has no alternative use for the facilities that are now being used to produce the carburetors, what would be the financial advantage (disadvantage) of buying 15,000 carburetors from the outside supplier? 2. Should the outside supplier’s offer be accepted? 3. Suppose that if the carburetors were purchased, Troy Engines, Ltd., could use the freed capacity to launch a new product. The segment margin of the new product would be $150,000 per year. Given this new assumption, what would be…arrow_forwardAssume that HASF furniture Inc., as described, currently purchases the chair cushions for its lawn set from an outside vendor for $30 per set. Modern Furniture’s chief operations officer wants an analysis of the comparative costs of manufacturing these cushions to determine whether bringing the manufacturing in-house would save the firm money. Additional information shows that if Modern furniture’s were to manufacture the cushions, the materials cost would be $16 and the labor cost would be $10 per set and that it would have to purchase cutting and sewing equipment, which would add $25,000 to annual fixed costs. Required Computation for 10,000 units What amount should have been inccrued if company produce 10,000 units What amount should have been inccrued if company purhcase 10,000 units from outside What amount company save if company make 10,000 cushionsarrow_forward

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning