Concept explainers

Videos

Volume Trade-off Decisions

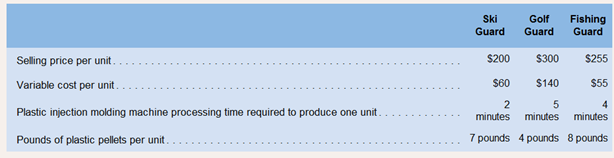

Outdoor Luggage, Inc., makes high-end, hard-sided luggage for sports equipment. Data concerning three of the company’s most popular models appear below.

Required:

1. If we assume that the total time available on the plastic injection molding machine is the constraint in the production process, how much contribution margin per minute of the constrained resource is earned by each product?

2. Which product offers the most profitable use of the plastic injection molding machine?

3. If we assume that a severe shortage of plastic pellets has required the company to cut back its production so much that its new constraint has become the total available pounds of plastic pellets, bow much contribution margin per pound of the constrained resource is earned by each product?

4. Which product offers the most profitable use of the plastic pellets?

5. Which product has the largest contribution margin per unit? Why wouldn’t this product be the most profitable use of the constrained resource in either case?

Want to see the full answer?

Check out a sample textbook solution

Chapter 11 Solutions

Introduction To Managerial Accounting

- Sensitivity Cost-Volume-Profit Analysis and Production Versus Period Costs, Multiple-Product Setting If both the variable and fixed production costs (refer to your answer to Requirement 1) associated with the canoe product line increased by 5% (beyond the estimate from the high-low analysis), how many canoes and paddles would need to be sold in order to earn a target income of 96,000? Assume the same sales mix and additional fixed costs as in Requirement 3.arrow_forwardSalvador Manufacturing builds and sells snowboards, skis and poles. The sales price and variable cost for each follows: Their sales mix is reflected in the ratio 7:3:2. If annual fixed costs shared by the three products are $196,200, how many units of each product will need to be sold in order for Salvador to break even?arrow_forwardSegment variable costing income statement and effect on operating income of change in operations Valdespin Company manufactures three sizes of camping tentssmall (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used. If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by 46,080 and 32,240, respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of 34,560 for the rental of additional warehouse space would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M. The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended June 30, 20Y9, is as follows: Instructions 1. Prepare an income statement for the past year in the variable costing format. Use the following headings: Data for each size should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the Total column, to determine operating income. 2. Based on the income statement prepared in (1) and the other data presented, determine the amount by which total annual operating income would be reduced below its present level if Proposal 2 is accepted. 3. Prepare an income statement in the variable costing format, indicating the projected annual operating income if Proposal 3 is accepted. Use the following headings: Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the Total column. For purposes of this problem, the expenditure of 34,560 for the rental of additional warehouse space can be added to the fixed operating expenses. 4. By how much would total annual operating income increase above its present level if Proposal 3 is accepted? Explain.arrow_forward

- Manufacturing builds and sells switch harnesses for glove boxes. The sales price and variable cost for each follows: Their sales mix is reflected in the ratio 4:4:1. If annual fixed costs shared by the three products are $1 8840 how many units of each product will need to be sold in order forJj to break even?arrow_forwardNutterco, Inc., produces two types of nut butter: peanut butter and cashew butter. Of the two, peanut butter is the more popular. Cashew butter is a specialty line using smaller jars and fewer jars per case. Data concerning the two products follow: aPractical capacity less expected usage (all unused capacity is permanent). bIn some cases, activity capacity must be purchased in steps (whole units). These steps are provided as necessary. The cost per step is the fixed activity rate multiplied by the step units. The fixed activity rate is the expected fixed activity costs divided by practical activity capacity. Annual overhead costs are listed below. These costs are classified as fixed or variable with respect to the appropriate activity driver. aCosts associated with practical activity capacity. The machine fixed costs are all depreciation with direct labor hours as the driver. bThese costs are for the actual levels of the cost driver. Required: 1. Prepare a traditional segmented income statement, using a unit-level overhead rate based on direct labor hours. Using this approach, determine whether the cashew butter product line should be kept or dropped. 2. Prepare an activity-based segmented income statement. Repeat the keep-or-drop analysis using an ABC approach.arrow_forwardConstrained Optimization Analysis: Product-Mix Decision Sandalwood Company producesvarious lines of high-end carpeting in its Asheville, North Carolina, plant. This question pertains to twodifferent grades of carpet in its Symphony line: commercial and residential. The former sells for $16per square yard, while the latter sells for $25 per square yard (wholesale). Variable costs are $10 persquare yard and $15 per square yard for the commercial and residential grade products, respectively.On average, it takes 12 labor hours to produce 100 square yards of commercial carpeting, and18 labor hours for each 100 square yards of residential carpeting. Currently, the company isproducing 28,000 square yards per week of commercial carpet and 6,000 square yards per week ofresidential carpet. Total labor-hour consumption at the plant is currently 4,440 hours per week. Fixedmanufacturing costs ($17,300 per week), are allocated to products on the basis of labor hours. At thecurrent volume and mix,…arrow_forward

- JJ Manufacturing builds and sells switch harnesses for glove boxes. The sales price and variable cost for each follows: Their sales mix is reflected in the ratio 4:4:1. A. What is the overall Composite Unit Contribution Margin for JJ Manufacturing with their current product mix? B. If annual fixed costs shared by the three products are $18,840, how many units of each product are to be sold in order for JJ Manufacturing to break even? Trunk Switch Gas Door Switch Glove Box Light C. Determine their break-even point in sales dollars. Trunk Switch Gas Door Switch Glove Box Lightarrow_forwardDifferential Costs and Sunk Costs Required: 1. What is the incremental manufacturing cost incurred if the company increases production from 20,000 to 20,001 units? 2. What is the incremental cost incurred if the company increases production and sales from 20,000 to 20,001 units? 3. Assume that Kubin Company produced 20,000 units and expects to sell 19,800 of them. If a new customer unexpectedly emerges and expresses interest in buying the 200 extra units that have been produced by the company and that would otherwise remain unsold, what is the incremental manufacturing cost per unit incurred to sell these units to the customer? 4. Assume that Kubin Company produced 20,000 units and expects to sell 19,800 of them. If a new customer unexpectedly emerges and expresses interest in buying the 200 extra units that have been produced by the company and that would otherwise remain unsold, what incremental selling and administrative cost per unit is incurred to sell these units to the customer?arrow_forwardProduct pricing and profit analysis with bottleneck operationsHercules Steel Company produces three grades of steel: high, good, andregular grade. Each of these products (grades) has high demand in themarket, and Hercules is able to sell as much as it can produce of allthree. The furnace operation is a bottleneck in the process and isrunning at 100% of capacity. Hercules wants to improve steel operationprofitability. The variable conversion cost is $15 per process hour. Thefixed cost is $200,000. In addition, the cost analyst was able to determinethe following information about the three products: The furnace operation is part of the total process for each of these threeproducts. Thus, for example, 4.0 of the 12.0 hours required to processHigh Grade steel are associated with the furnace.Instructions1. Determine the unit contribution margiñ for each product.2. Provide an analysis to determine the relative productprofitability, assuming that the furnace is a bottleneck.arrow_forward

- Product Pricing and Profit Analysis with Bottleneck Operations Hercules Steel Company produces three grades of steel: high, good, and regular grade. Each of these products (grades) has high demand in the market, and Hercules is able to sell as much as it can produce of all three. The furnace operation is a bottleneck in the process and is running at 100% of capacity. Hercules wants to improve steel operation profitability. The variable conversion cost is $15 per process hour. The fixed cost is $200,000. In addition, the cost analyst was able to determine the following information about the three products: HighGrade Good Grade Regular Grade Budgeted units produced 5,000 5,000 5,000 Total process hours per unit 12 11 10 Furnace hours per unit 4 3 2.5 Unit selling price $280 $270 $250 Direct materials cost per unit $90 $84 $80 The furnace operation is part of the…arrow_forwardShort-run pricing, capacity constraints. Fashion Fabrics makes pants from a special material. The fabric is special because of the way it fits many body types. The pants sell for $142. A well-known retail establishment has asked Fashion Fabrics to produce 3,000 shorts from the same fabric. The factory has unused capacity, so Barbara Brooks, the owner of Fashion Fabrics, calculates the cost of making a pair of shorts from the fabric. Costs for the pants and shorts are as follows:arrow_forwardProduct Pricing and Profit Analysis with Bottleneck Operations Hercules Company produces three grades of steel: high, good, and regular grade. Each of these products (grades) has high demand in the market, and Hercules is able to sell as much as it can produce of all three. The furnace operation is a bottleneck in the process and is running at 100% of capacity. Hercules wants to improve steel operation profitability. The variable conversion cost is $10 per process hour. The fixed cost is $513,000. In addition, the cost analyst was able to determine the following information about the three products: High Grade Good Grade Regular Grade Budgeted units produced 3,000 3,000 3,000 Total process hours per unit 15 13 10 Furnace hours per unit 4 3 5 Unit selling price $299 $247 $264 Direct materials cost per unit $113 $105 $99 The furnace operation is part of the total process for each of these three products. Thus, for example, 4 of…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College