Videos

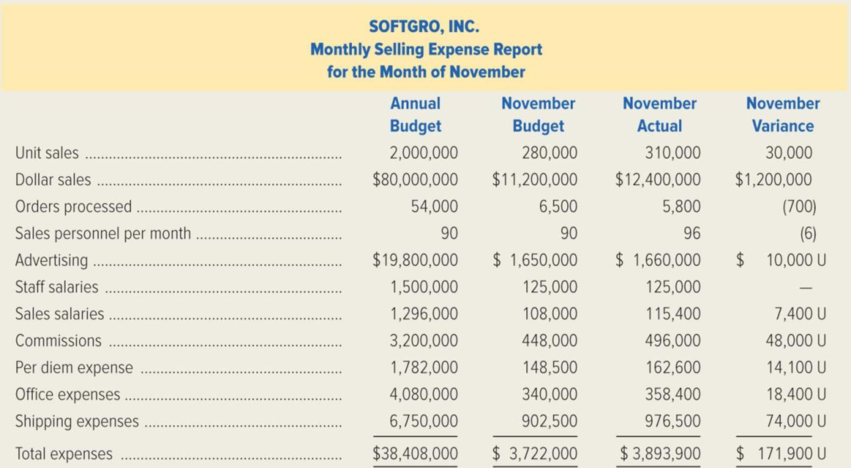

Mark Fletcher, president of SoftGro, Inc., was looking forward to seeing the performance reports for November because he knew the company’s sales for the month had exceeded budget by a considerable margin. SoftGro, a distributor of educational software packages, had been growing steadily for approximately two years. Fletcher’s biggest challenge at this point was to ensure that the company did not lose control of expenses during this growth period. When Fletcher received the November reports, he was dismayed to see the large unfavorable variance in the company’s Monthly Selling Expense Report that follows.

Fletcher called in the company’s new controller, Susan Porter, to discuss the implications of the variances reported for November and to plan a strategy for improving performance. Porter suggested that the company’s reporting format might not be giving Fletcher a true picture of the company’s operations. She proposed that SoftGro implement flexible budgeting. Porter offered to redo the Monthly Selling Expense Report for November using flexible budgeting so that Fletcher could compare the two reports and see the advantages of flexible budgeting.

Porter discovered the following information about the behavior of SoftGro’s selling expenses.

- The total compensation paid to the sales force consists of a monthly base salary and a commission; the commission varies with sales dollars.

- Sales office expense is a semi variable cost with the variable portion related to the number of orders processed. The fixed portion of office expense is $3,000,000 annually and is incurred uniformly throughout the year.

- Subsequent to the adoption of the annual budget for the current year, SoftGro decided to open a new sales territory. As a consequence, approval was given to hire six additional sales people effective November 1. Porter decided that these additional six people should be recognized in her revised report.

- Per diem reimbursement to the sales force, while a fixed amount per day, is variable with the number of sales personnel and the number of days spent traveling. SoftGro’s original budget was based on an average sales force of 90 people throughout the year with each salesperson traveling 15 days per month.

- The company’s shipping expense is a semi variable cost with the variable portion, $3.00 per unit, dependent on the number of units sold. The fixed portion is incurred uniformly throughout the year.

Required:

- 1. Citing the benefits of flexible budgeting, explain why Susan Porter would propose that Soft Grouse flexible budgeting in this situation.

- 2. Prepare a revised Monthly Selling Expense Report for November that would permit Mark Fletcher to more clearly evaluate SoftGro’s control over selling expenses. The report should have a line for each selling expense item showing the appropriate budgeted amount, the actual selling expense, and the monthly dollar variance.

Trending nowThis is a popular solution!

Chapter 11 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- Howard Rockness was worried. His company, Rockness Bottling, showed declining profits over the past several years despite an increase in revenues. With profits declining and revenues increasing, Rockness knew there must be a problem with costs. Rockness sent an e-mail to his executive team under the subject heading, “How do we get Rockness Bottling back on track?” Meeting in Rockness’s spacious office, the team began brainstorming solutions to the declining profits problem. Some members of the team wanted to add products. (These were marketing people.) Some wanted to fire the least efficient workers. (These were finance people.) Some wanted to empower the workers. (These people worked in the human resources department.) And some people wanted to install a new computer system. (It should be obvious who these people were.) Rockness listened patiently. When all participants had made their cases, Rockness said, “We made money when we were a smaller, simpler company. We have grown, added…arrow_forwardThe executives at Stark Inc., a plumbing supply manufacturer, recently reviewed production capacity for the upcoming year and set production budgets. Based on the number of units that they expected to produce, they budgeted sales and set sales targets for each of their retail locations. They did not ask for the input of the individual store managers as they believed that they had sufficient information and they wanted to ensure that the store targets were not easily attainable. When the actual sales numbers started to come in, they were much lower than the budget. In investigating the variance, the company found that one location had a new competitor that had just opened down the street, and another had significant road construction that impeded the traffic flow and cut down on customers. There were also some new products on the market that were cutting into the company’s market share. Because of the missed sales budget, the company had overproduced, resulting in excess inventory.…arrow_forwardSteve Morgan, controller for Newton Industries, was reviewing production cost reports for the year. One amount in these reports continued in to bother him – advertising. During the year the company had instituted an expensive advertisement campaign to sell some of its slower-moving products. It was still too early to tell whether the advertising campaign was successful. There had been much internal debate as how to report advertising cost. The vice president of finance argued that advertising costs should be reported as cost of production, just like direct material and direct labor. He therefore recommended that this cost be identified as manufacturing overhead and reported as part of inventory costs until sold. Others disagreed. Morgan believed that this cost should be reported as an expense of the current period, so as not to overstate net income. Others argued that it should be reported as prepaid advertising and reported as a current asset. The president finally had to decide…arrow_forward

- The Customer Service Department of Door Industries Inc. asked the Publications Department to prepare a brochure for its training program. The Publications Department delivered the brochures and charged the Customer Service Department a rate that was 25% higher than could be obtained from an outside printing company. The policy of the company required the Customer Service Department to use the internal publications group for brochures. The Publications Department claimed that it had a drop in demand for its services during the fiscal year, so it had to charge higher prices in order to recover its payroll and fixed costs. Recommend how the cost of the brochure should be transferred to the Customer Service Department.arrow_forwardBendOR, Inc., manufactures control panels for the electronics industry and has just completed its first year of operations. The following discussion took place between the controller, Gordon Merrick, and the company president, Matt McCray: Matt: I’ve been looking over our first year’s performance by quarters. Our earnings have been increasing each quarter, even though our sales have been flat and our prices and costs have not changed. Why is this? Gordon: Our actual sales have stayed even throughout the year, but we’ve been increasing the utilization of our factory every quarter. By keeping our factory utilization high, we will keep our costs down by allocating the fixed plant costs over a greater number of units. Naturally, this causes our cost per unit to be lower than it would be otherwise. Matt: Yes, but what good is this if we are unable to sell everything that we make? Our inventory is also increasing. Gordon: This is true. However, our unit costs are lower because of the…arrow_forwardThe salespeople at Larkspur, a notebook manufacturer, commonly pressured operations managers to keep costs down so the company could give bigger discounts to large customers. David, the operations supervisor, leaked the $0.80 total unit cost to salespeople, who were thrilled, since that was slightly lower than the previous year's unit cost. Budgets were not yet finalized for the upcoming year, so it was unclear what the target unit cost would be. David knew the current year's operating capacity was two million notebooks, and Larkspur produced and sold just that many. The detailed breakdown of the $0.80 total unit cost is as follows. Direct material Direct labor Variable overhead Fixed overhead Total cost per unit $0.05 0.20 0.15 0.40 $0.80arrow_forward

- The salespeople at Metlock, a notebook manufacturer, commonly pressured operations managers to keep costs down so the company could give bigger discounts to large customers. Richard, the operations supervisor, leaked the $0.65 total unit cost to salespeople, who were thrilled, since that was slightly lower than the previous year's unit cost. Budgets were not yet finalized for the upcoming year, so it was unclear what the target unit cost would be. Richard knew the current year's operating capacity was two million notebooks, and Metlock produced and sold just that many. The detailed breakdown of the $0.65 total unit cost is as follows. Direct material Direct labor Variable overhead Fixed overhead Total cost per unit (a) (b) Total fixed costs Gross margin Your answer is correct. What were Metlock's total fixed costs? If the average selling price was $2.10, how much gross margin did the company generate? $0.15 Fixed costs 0.15 Total cost per unit 0.15 Gross margin 0.20 $0.65 Save for…arrow_forwardJamison examined monthly data for 2016 (not given in the case), and she detected an improving pattern during the year. Monthly sales were rising, costs were falling, and large losses in the early months had turned to a small profit by December. Thus, the annual data look somewhat worse than the final monthly data. Also, it appears to be taking longer for the advertising program to get the message out, for the new sales offices to generate sales, and for the new manufacturing facilities to operate efficiently. In other words, the lags between spending money and deriving benefits were longer than D’Leon’s managers had anticipated. For these reasons, Jamison and Campo see hope for the company—provided it can survive in the short run. Jamison must prepare an analysis of where the company is now, what it must do to regain its financial health, and what actions should be taken. Your assignment is to help her answer the following questions. Provide clear explanations, not yes or no answers.…arrow_forward6. Person X has managed a downtown store in a major metropolitan city for several years. The firm has ten stores in varying locations. In the past, senior management noticed Person X's work and he has received very good annual evaluations for his management of the store. \\nThis year his store has generated steady growth in sales, but earnings have been deteriorating. After examining the monthly performance report generated by the company budgeting department, he noticed that increasing fixed costs is causing the decrease in earnings. \\nAdministrative corporate costs, primarily fixed costs, are allocated to individual stores each month based on actual sales for that month. Two of these stores are currently growing at a rapid pace, while four other stores are having operating difficulties. \\n\\nRequired:\\nFrom the information presented, what do you think is the cause of Person X's reported decrease in earnings? How can this be corrected?arrow_forward

- The salespeople at Ayayai, a notebook manufacturer, commonly pressured operations managers to keep costs down so the company could give bigger discounts to large customers. Kenneth, the operations supervisor, leaked the $1.20 total unit cost to salespeople, who were thrilled, since that was slightly lower than the previous year's unit cost. Budgets were not yet finalized for the upcoming year, so it was unclear what the target unit cost would be. Kenneth knew the current year's operating capacity was two million notebooks, and Ayayai produced and sold just that many. The detailed breakdown of the $1.20 total unit cost is as follows. Direct material Direct labor Variable overhead Fixed overhead Total cost per unit (a) Total fixed costs Gross margin tA $ $0.10 What were Ayayai's total fixed costs? If the average selling price was $1.95, how much gross margin did the company generate? LA 0.25 0.05 0.80 $1.20arrow_forwardDue to erratic sales of its sole product — a high capacity battery for laptop computers — PEM, Inc., has been experiencing financial difficulty for some time. The company's contribution format income statement for the most recent month is given below (see image attached): Required:2. The president believes that a $6,600 increase in the monthly advertising budget, combined with an intensified effort by the sales staff, will result in an $81,000 increase in monthly sales. If the president is right, what will be the increase (decrease) in the company's monthly net operating income? (CM ratio: 40%, Break-even point in unit sales: 14,800, Break-even point in dollar sales: $296,000).arrow_forwardJerry Prior, Beeler Corporation’s controller, is concerned that net income may be lower this year. He is afraid upper-level management might recommend cost reductions by laying off accounting staff, including him. Prior knows that depreciation is a major expense for Beeler. The company currently uses the double-declining-balance method for both financial reporting and tax purposes, and he’s thinking of selling equipment that, given its age, is primarily used when there are periodic spikes in demand. The equipment has a carrying value of $2,000,000 and a fair value of $2,180,000. The gain on the sale would be reported in the income statement. He doesn’t want to highlight this method of increasing income. He thinks, “Why don’t I increase the estimated useful lives and the salvage values? That will decrease depreciation expense and require less extensive disclosure, since the changes are accounted for prospectively. I may be able to save my job and those of my staff.” Instructions Answer…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education