INTERMEDIATE ACCOUNTING RMU 9TH EDITION

9th Edition

ISBN: 9781260998726

Author: SPICELAND

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 12, Problem 12.7BYP

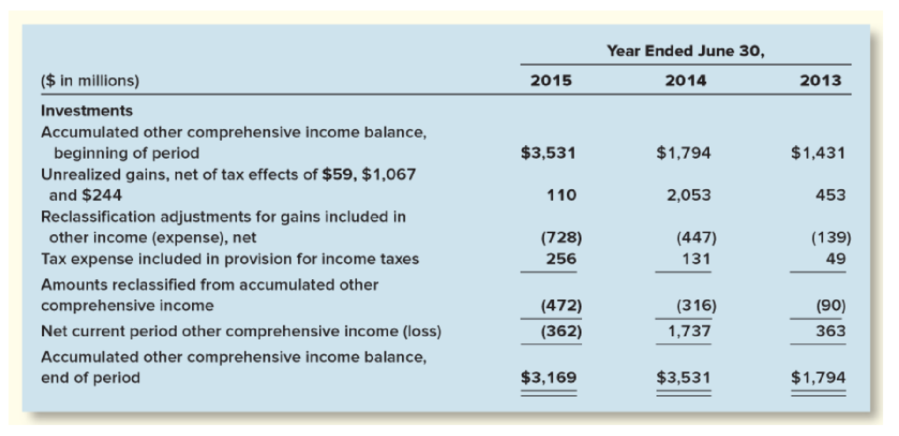

Real World Case 12–7

Comprehensive income —Microsoft

• LO12-4

Microsoft’s 2015 10-K includes the following information in Note 20—Accumulated Other Comprehensive Income relevant to its available-for-sale investments:

Required:

1. Prepare a

2. Prepare a journal entry to record Microsoft’s reclassification adjustment for 2015.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

WhyRU Company usually depreciates its equipment using straight line method for accounting purposes, but

for tax purposes its sum-of-the-years method. WhyRU Company acquired the equipment through purchase

amounting to P2,400,000 on January 1,2018. Assume a tax rate of 30%. Useful life is 4 years.

WhyRU Company made the following income in its income tax return available through reports for 2018 –

P800,000; 2019 – P890,0000; 2020 – P1,200,000; 2021 – P1,500,000 There is no other differences between

WhyRU's accounting income and taxable income for years 2018, 2019, 2020 and 2021 other than for the

difference in depreciation for the equipment described.

Required information

Problem 16-8 Multiple differences; taxable income given; two years; balance sheet classification; change

in tax rate [LO16-4, 16-6, 16-8]

[The following information applies to the questions displayed below.]

Arndt, Inc., reported the following for 2018 and 2019 ($ in millions):

2018

2019

Revenues

$ 995

$1,073

Expenses

Pretax accounting income (income statement)

Taxable income (tax return)

800

840

$ 195

$ 195

233

$ 245

Tax rate: 40%

a. Expenses each year include $30 million from a two-year casualty insurance policy purchased in 2018 for $60 million.

The cost is tax deductible in 2018.

b. Expenses include $2 million insurance premiums each year for life insurance on key executives.

c. Arndt sells one-year subscriptions to a weekly journal. Subscription sales collected and taxable in 2018 and 2019 were

$39 million and $57 million, respectively. Subscriptions included in 2018 and 2019 financial reporting revenues were

$36 million ($14 million collected in 2017 but not…

Consider the information for AGL provided in the two tables below and answer the following questions. (Note: numbers in red are negative)

Balance Sheet $'m

cash

Receivables

Inventory

Other assets

Total Current Assets

Inventory

Financial Assets & Investments

Plant

Intangibles

Other assets

Total Non-Current Assets

Total Assets

Trade payables

Borrowings

Other liabilities

Total Current Liabilities

Debt

Other liabilities

Total non-current liabilities

Total Liabilities

Net Assets

Issued Capital

Reserves

Retained earnings

Total Equity

2021

88

1,889

418

1,280

3,675

46

950

6,283

3,302

1,194

11,775

15,450

1,838

305

832

2,975

2,880

4,089

6,969

9,944

5,506

5,601

20

(115)

5,506

2020

141

1,571

400

1,010

3,122

59

688

6,640

3,638

460

11,485

14,607

1,351

38

999

2,388

3,070

1,177

4,247

6,635

7,972

5,603

(80)

2,449

7,972

Chapter 12 Solutions

INTERMEDIATE ACCOUNTING RMU 9TH EDITION

Ch. 12 - All investments in debt securities are classified...Ch. 12 - When market rates of interest rise after a...Ch. 12 - Does GAAP distinguish between fair values that are...Ch. 12 - When a debt investment is acquired to be held for...Ch. 12 - Prob. 12.5QCh. 12 - What is comprehensive income? Its composition...Ch. 12 - Why are holding gains and losses treated...Ch. 12 - Prob. 12.8QCh. 12 - Prob. 12.9QCh. 12 - Prob. 12.10Q

Ch. 12 - Under IFRS No. 9, which reporting categories are...Ch. 12 - Prob. 12.12QCh. 12 - Do U.S. GAAP and IFRS differ in the amount of...Ch. 12 - Under what circumstances is the equity method used...Ch. 12 - The equity method has been referred to as a...Ch. 12 - In the application of the equity method, how...Ch. 12 - Prob. 12.17QCh. 12 - Prob. 12.18QCh. 12 - Prob. 12.19QCh. 12 - How does IFRS differ from U.S. GAAP with respect...Ch. 12 - What is the effect of a company electing the fair...Ch. 12 - Define a financial instrument. Provide three...Ch. 12 - Some financial instruments are called derivatives....Ch. 12 - (Based on Appendix 12A) Northwest Carburetor...Ch. 12 - Prob. 12.25QCh. 12 - Prob. 12.26QCh. 12 - (Based on Appendix 12B) Reporting an investment at...Ch. 12 - Prob. 12.28QCh. 12 - Explain how the CECL model (introduced in ASU No....Ch. 12 - Prob. 12.30QCh. 12 - Prob. 12.1BECh. 12 - Prob. 12.2BECh. 12 - Trading securities LO12-3 For the Coca-Cola bonds...Ch. 12 - Available -for-sale securities LO12-4 SL...Ch. 12 - Available -for-sale securities LO12-4 For the...Ch. 12 - Prob. 12.6BECh. 12 - Prob. 12.7BECh. 12 - Prob. 12.8BECh. 12 - Prob. 12.9BECh. 12 - Prob. 12.10BECh. 12 - Equity investments and dividends LO12-5 Turner...Ch. 12 - Prob. 12.12BECh. 12 - Prob. 12.13BECh. 12 - Equity method investments LO12-6, LO12-9 Kim...Ch. 12 - Change in principle; change to the equity method ...Ch. 12 - Fair value option; equity method investments ...Ch. 12 - Prob. 12.17BECh. 12 - Impairments (AFS Credit Loss Model) (Appendix 12B)...Ch. 12 - Prob. 12.19BECh. 12 - Prob. 12.20BECh. 12 - Prob. 12.1ECh. 12 - Prob. 12.2ECh. 12 - Securities held-to-maturity LO12-1 FFT...Ch. 12 - Prob. 12.4ECh. 12 - Prob. 12.5ECh. 12 - Trading securities LO12-1 [This is a variation of...Ch. 12 - Various transactions relating to trading...Ch. 12 - Prob. 12.8ECh. 12 - Securities available-for-sale; adjusting entries ...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Available -for-sale securities LO12-1, LO12-4...Ch. 12 - Classification of securities; adjusting entries ...Ch. 12 - Prob. 12.14ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Equity investments; fair value through net income ...Ch. 12 - Prob. 12.17ECh. 12 - Equity investments; fair value through net income ...Ch. 12 - Investment securities and equity method...Ch. 12 - Equity method; purchase; investee income;...Ch. 12 - Error corrections; equity method investment ...Ch. 12 - Prob. 12.22ECh. 12 - Prob. 12.23ECh. 12 - Prob. 12.24ECh. 12 - Prob. 12.25ECh. 12 - Prob. 12.26ECh. 12 - Prob. 12.27ECh. 12 - Prob. 12.28ECh. 12 - Prob. 12.29ECh. 12 - Prob. 12.30ECh. 12 - Prob. 12.31ECh. 12 - Prob. 12.32ECh. 12 - Accounting for impairments under IFRS (Appendix...Ch. 12 - Prob. 12.1PCh. 12 - Prob. 12.2PCh. 12 - Securities available-for-sale; bond investment;...Ch. 12 - Prob. 12.4PCh. 12 - Various transactions related to trading securities...Ch. 12 - Various transactions related to securities...Ch. 12 - Prob. 12.7PCh. 12 - Various transactions relating to trading...Ch. 12 - Securities held-to-maturity; securities available...Ch. 12 - Investment securities and equity method...Ch. 12 - Prob. 12.11PCh. 12 - Prob. 12.12PCh. 12 - Prob. 12.13PCh. 12 - Equity method LO12-6, LO12-7 On January 2, 2018,...Ch. 12 - Prob. 12.15PCh. 12 - Prob. 12.16PCh. 12 - Accounting for debt and equity investments ...Ch. 12 - Prob. 12.18PCh. 12 - Real World Case 121 Intels investments LO12-4 The...Ch. 12 - Prob. 12.2BYPCh. 12 - Prob. 12.4BYPCh. 12 - Prob. 12.6BYPCh. 12 - Real World Case 127 Comprehensive income Microsoft...Ch. 12 - Continuing Cases Target Case LO12-4, LO12-6...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Problem 16-6 (IAA) Complex Company reported the following information relating to income before tax for accounting purposes: 2021 2022 2023 2024 Income tax rate In 2021, the entity recognized doubtful accounts of P100,000. The doubtful accounts were considered worthless or uncollectible in 2022. 2,000,000 3,000,000 4,000,000 5,000,000 25% Analysis of the tax and book records disclosed P120,000 in unearned rent income on December 31, 2021 that had been recognized as taxable income in 2021 when the cash was received. Also on December 31, 2021, estimated warranty cost of P300,000 had been recognized as expense on the books in 2021 when the product sales were made but is not deductible for tax purposes until paid. The unearned rent income on December 31, 2021 was realized and the actual warranty payments were made in the following years: Rent income per book Actual warranty payments 40,000 40,000 40,000 2022' 2023 2024 20,000 80,000 200,000 Required: 1. Prepare journal entries for 2021,…arrow_forwardFormula: Add, Subtract; Cell Referencing Using Excel to Determine Income Tax Effects PROBLEM At December 31, 2022 and 2023, Secor Inc. reported amounts for a deferred tax asset. Information concerning the company's income taxes is provided here. Deferred tax asset, December 31, 2022 Deferred tax asset, December 31, 2023 Current tax expense 2023 Ś 40,000 62,000 70,000 Student Work Area Required: Provide input into cells shaded in yellow in this template. Use mathematical formulas with cell references to the Problem area or to this work area. What amount should Secor report as total 2020 income tax expense? 2023 income tax expense Current Tax Expense Prepare the journal entries to record income taxes for 2020. Income Tax Payable Deferred Tax Expense $ Current Tax Expense 22,000 Debit 70,000 22,000 Credit 70,000 22,000arrow_forwardhapter 15, 16, and 17 Saved education.com%252F#/activity/q Help Save & E Isaac Incorporated began operations in January 2024. For some property sales, Isaac recognizes income in the period of sale for financial payments. reporting purposes. However, for income tax purposes, Isaac recognizes income when it collects cash from the buyer's installment In 2024, Isaac had $712 million in sales of this type. Scheduled collections for these sales are as follows: 2024 $ 68 million 2025 148 million 233.53 2026 147 million 2027 170 million pped 179 million eBook eferences 2028 $ 712 million Assume that Isaac has a 25% income tax rate and that there were no other differences in income for financial statement and tax purposes. Ignoring operating expenses, what deferred tax liability would Isaac report in its year-end 2024 balance sheet? Note: Round your answer to the nearest whole million. MC Graw Type here to search Multiple Choice # 2 3 W E R 4. S Z Alt C 85 00 9:25 PM High winds soon ^ la 4»)…arrow_forward

- 1. Ch03 Financial Planning Exercise 4 Chapter 3 Financial Planning Exercise 4 Effect of tax credit vs. tax exemption By defining after-tax income, demonstrate the differences resulting from a $1,500 tax credit versus a $1,500 tax deduction for a single taxpayer in the 25% tax bracket with $41,000 of pre- tax income. Round your answers to two decimal places. (Use Exhibit 3.3.) Deduction $ Credit $arrow_forwardE 18-1 Comprehensive The following is from the 2018 annual report of Kaufman Chemicals, Inc.: Statements of Comprehensive Income Years Ended December 31 income • LO18-2 2018 2017 2016 Net income $856 $766 $594 Other comprehensive income: Change in net unrealized gains on investments, net of tax of $22, ($14), and $15 in 2018, 2017, and 2016, respectively 34 (21) 23 Other (2) $888 (1) $744 $618 Total comprehensive income Kaufman reports accumulated other comprehensive income in its balance sheet as a component of shareholders equity as follows: ($ in millions) 2018 2017 Shareholders' equity: Common stock 355 355 Additional paid-in capital Retained earnings Accumulated other comprehensive income 8,567 6,544 8,567 5,988 107 75 Total shareholders'equity $15,573 $14,985 Required: 1. What is comprehensive income and how does it differ from net income? 2. How is comprehensive income reported in a balance sheet? 3. Why is Kaufman's 2018 balance sheet amount different from the 2018 amount…arrow_forwardnment Required information Problem 6-4A & 6-5A (Algo) [The following information applies to the questions displayed below.] Problem 6-4A (Algo) F2 Federal income tax withholding Social Security tax Medicare tax State income tax withholding Gerald Utsey earned $48,700 in 2021 for a company in Kentucky. He is single with one dependent under 17 and is paid weekly. The FUTA rate in Kentucky for 2021 is 0.6 percent on the first $7,000 of employee wages, and the SUTA rate is 5.4 percent with a wage base of $11,100. Use the percentage method in Appendix Cand the state information in Appendix D. Manual payroll system is used and Box 2 is not checked. 3 Required: Compute the following employee share of the taxes. (Do not round intermediate calculation. Round your final answers to 2 decimal places.) JUL 15 80 F3 $ 4 E R Q F4 % 5 DII F8 ( 9 A F9 U I O Help ) 0 Save & Exit F10 P Check my wom 4 F11 Sub { + [ Farrow_forward

- NOPAT 8250000 EBITDA 17725000 Net Income 5050000 Capital Expenditures 6820000 After tax capital costs 6820000 Tax rate 40%Calculate the interest expense and EVAarrow_forwardPartial Income Statement Excel Exercise Compute the Following ՀԱՐ Sales COGS SG&A Depreciation Debt Int. Rate Tax Rate* 2019 100 40 EBITDA EBIT 25 Interest 10 EBT 0.08 Tax 0.25 Net Income ? ? ? ? ? ? Partial Balance Sheet Debt and Loans 150 Total Equity 150 Total Assets 300 Inv. Change 10 A/R Change A/P Change 35 20 Net Profit Margin Equity Multiplier Verify Dupont ROE ? סיי ? ? ? ? ? * Assume all taxes paid in current period (no accrued taxes) for rest of course CF from Operations ROE Asset Turnover CED Tt O 24arrow_forwardIntel-period Tax Allocation Chris Green, CPA, is auditing Rayne Co.s 2019 financial statements. For the year ended December 31, 2019, Rayne is applying GAAP for income taxes. Raynes controller, Dunn, has prepared a schedule of all differences between financial statement and income tax return income. Dunn believes that as a result of pending legislation, the enacted tax rate at December 31, 2019, will be increased for 2020. Dunn is uncertain which differences to include and which rates to apply in computing deferred taxes. Dunn has requested an overview of GAAP from Green. Required: Prepare a brief memo to Dunn from Green that identifies the objectives of accounting for income taxes, defines temporary differences, explains how to measure deferred tax assets and liabilities, and explains how to measure deferred income tax expense or benefit.arrow_forward

- Exercise 18-1 (Algo) Comprehensive Income [LO18-2] The following is from the 2024 annual report of Kaufman Chemicals, Incorporated: Years Ended December 31 Statements of Comprehensive Income Net income 2024 $ 878 2023 $ 708 2022 $ 563 Other comprehensive income: Change in net unrealized gains on AFS investments, net of tax of $20, ($18), and $18 in 2024, 2023, and 2022, respectively Other 33 (2) (26) (1) 25 1 $ 909 $ 681 $ 589 Total comprehensive income Kaufman reports accumulated other comprehensive income in its balance sheet as a component of shareholders' equity as follows: ($ in millions) Shareholders' equity: Common stock Additional paid-in capital Retained earnings Accumulated other comprehensive income Total shareholders' equity 2024 2023 $ 340 8,373 7,453 107 $ 16,273 $ 340 8,373 6,897 76 $ 15,686 Required: 3. From the information provided, determine how Kaufman calculated the $107 million accumulated other comprehensive income in 2024. Note: Negative amount should be…arrow_forward1-What will be the net income? a. 72000 b. 56000 c. 16000 d. 338000 Clear my choice Question 43 Not yet answered Marked out of 1.00 Flag question Question text What will be the Gross Profit at the end of the year December 2019 a. OMR 56000 b. OMR 16000 c. OMR 338,000 d. OMR 336,000 2-What is the Gross Margin in terms of Percentage? a. 16.66 b. 16.56 c. Cannot be determined d. 20.66 3-What will be the total operating expense? a. 21500 b. 53200 c. 41200 d. 19700 4-What will be the total Selling and distribution expense? a. 41200 b. 19700 c. 14800 d. 17200arrow_forward#14 Objective G-1-2 continued. 14. In prior years, the taxpayer's adjusted AMT and minimum tax credit were as follows: Minimum Tax Credit Year 2014. 2015. 2016. 2017. Adjusted AMT $25,000 $15,000 $10,000 $12,000 The taxpayer's minimum tax credit for 2018 (before any limitation) is: 14. o a $52,000 Ob $42,000 OC. $27,000 od. $17,000arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...

Finance

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:Cengage Learning

Chapter 19 Accounting for Income Taxes Part 1; Author: Vicki Stewart;https://www.youtube.com/watch?v=FMjwcdZhLoE;License: Standard Youtube License