Videos

Effect of activity level and opportunity cost on segment elimination decision

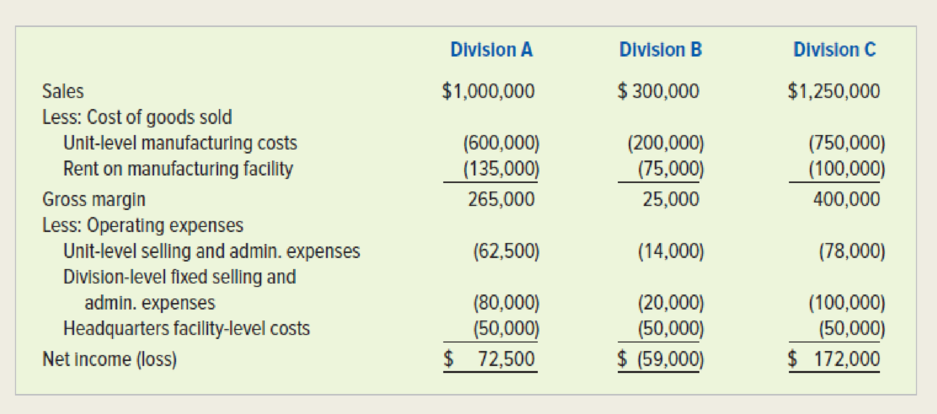

Lenox Manufacturing Co. produces and sells specialized equipment used in the petroleum industry. The company is organized into three separate operating branches: Division A, which manufactures and sells heavy equipment; Division B, which manufactures and sells hand tools; and Division C, which makes and sells electric motors. Each division is housed in a separate manufacturing facility. Company headquarters is located in a separate building. In recent years, Division B has been operating at a net loss and is expected to continue to do so. Income statements for the three divisions for 2017 follow:

Required

- a. Based on the preceding information, recommend whether to eliminate Division B. Support your answer by preparing companywide income statements before and after eliminating Division B.

- b. During 2017, Division B produced and sold 20,000 units of hand tools. Would your recommendation in response to Requirement a change if sales and production increase to 30,000 units in 2018? Support your answer by comparing differential revenue and avoidable cost for Division B, assuming that it sells 30,000 units.

- c. Suppose that Lenox could sublease Division B’s manufacturing facility for $160,000. Would you operate the division at a production and sales volume of 30,000 units, or would you close it? Support your answer with appropriate computations.

a.

Identify whether Division B is eliminated or not.

Explanation of Solution

Special order decisions: Special order decisions include circumstances in which the board must choose whether to acknowledge abnormal customer orders. These requests or orders normally necessitate special dispensation or include a demand for lesser price.

Outsourcing: It can be termed as conveying all or part of an activity to a supplier or a provider. While outsourcing was initially limited to fundamental activities, it as of now invades the administration of numerous organizations.

Opportunity cost: Opportunity cost is the forfeit of certain benefits such as cost savings, incomes, which is surrendered by not picking an option. Opportunity costs are applicable in decisions where the acknowledgment of one option disqualifies the likelihood of selecting different alternatives.

Determine the contribution to profit

Therefore the contribution to profit is ($9,000).

Prepare the companywide income statement before and after eliminating Division B.

The company wide income statement before eliminating Division B is as follows:

| Companywide Income Statement before Division B is eliminated | |

| Sales | S2,550,000 |

| Less: Cost of goods sold | |

| Unit level manufacturing costs | $1,550,000 |

| Rent on manufacturing facility | $310,000 |

| Gross margin | $690,000 |

| Less: Operating expenses | |

| Unit level selling & administrative costs | $154,500 |

| Division level fixed selling & administrative costs | $200,000 |

| Headquarters facility-level costs | $150,000 |

| Net income (loss) | $185,500 |

Table (1)

The company wide income statement after eliminating Division B is as follows:

| Companywide Income Statement after Division B is eliminated | |

| Sales | $2,250,000 |

| Less: Cost of goods sold | |

| Unit level manufacturing costs | $ 1,350,000 |

| Rent on manufacturing facility | $235,000 |

| Gross margin | $665,000 |

| Less: Operating expenses | |

| Unit level selling & administrative costs | $140,500 |

| Division level fixed selling & administrative costs | $180,000 |

| Headquarters facility-level costs | $ 150,000 |

| Net income (loss) | $194,500 |

Table (2)

From the results obtained above, the contribution to profit is negative at ($9,000). Hence the Division B should be eliminated.

Therefore, Division B should be eliminated.

b.

Identify whether the recommendations in Requirement A changes if the units increased to 30,000 units by comparing Division B’s differential avoidable costs and revenue.

Explanation of Solution

Initiate by calculating the cost price per unit and the selling per unit that will change in respect to the quantity of units produced and traded. The result is divided with the total cost for respective group by 20,000 units to get cost per unit. The headquarters facility-level costs are not considered from the investigation since these costs are not avoidable.

Determine the selling price per unit

Therefore, the selling price per unit is $15.

Determine the unit level manufacturing costs

Therefore, the unit level manufacturing costs is $10.

Determine the unit level selling and administrative costs

Therefore, the unit level selling and administrative costs is $0.70.

Determine the contribution to profit

The comparison between differential revenue and avoidable cost is determined in the below step.

Therefore, the contribution to profit is $34,000.

From the results obtained above, the profit contributed by Division B would be 30,000 units. Hence the division should not be eliminated. Additionally, it is vital to contemplate development prospective before choosing to eliminate a segment.

Therefore, Division B should not be eliminated.

c.

Identify whether to operate the division with volume of 30,000 units or it should be closed.

Explanation of Solution

Determine the profit or loss of the division

Therefore, the loss of the division is $51,000.

The reasons on whether to operate the division with volume of 30,000 units or it should be closed is as follows:

- It is mentioned that Company LM is paying $75,000 to lease the manufacturing facility for Division B.

- The business could earn $85,000

- By operating the division, the organization is allowing up the chance to sublease the office.

- This is an opportunity cost that would be avoidable by eradicating Division B.

- Consequently, it must be incorporated into the investigation. If the volume is 30,000 units Division B contributes $34,000 as profit.

When considering opportunity cost, the profit turns into a loss of $51,000. According to these conditions, Division B should be eliminated.

Therefore, Division B should be eliminated.

Want to see more full solutions like this?

Chapter 13 Solutions

SURVEY OF ACCOUNTING 360DAY CONNECT CAR

- Segment variable costing income statement and effect on operating income of change in operations Valdespin Company manufactures three sizes of camping tentssmall (S), medium (M), and large (L). The income statement has consistently indicated a net loss for the M size, and management is considering three proposals: (1) continue Size M, (2) discontinue Size M and reduce total output accordingly, or (3) discontinue Size M and conduct an advertising campaign to expand the sales of Size S so that the entire plant capacity can continue to be used. If Proposal 2 is selected and Size M is discontinued and production curtailed, the annual fixed production costs and fixed operating expenses could be reduced by 46,080 and 32,240, respectively. If Proposal 3 is selected, it is anticipated that an additional annual expenditure of 34,560 for the rental of additional warehouse space would yield an additional 130% in Size S sales volume. It is also assumed that the increased production of Size S would utilize the plant facilities released by the discontinuance of Size M. The sales and costs have been relatively stable over the past few years, and they are expected to remain so for the foreseeable future. The income statement for the past year ended June 30, 20Y9, is as follows: Instructions 1. Prepare an income statement for the past year in the variable costing format. Use the following headings: Data for each size should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin, as reported in the Total column, to determine operating income. 2. Based on the income statement prepared in (1) and the other data presented, determine the amount by which total annual operating income would be reduced below its present level if Proposal 2 is accepted. 3. Prepare an income statement in the variable costing format, indicating the projected annual operating income if Proposal 3 is accepted. Use the following headings: Data for each style should be reported through contribution margin. The fixed costs should be deducted from the total contribution margin as reported in the Total column. For purposes of this problem, the expenditure of 34,560 for the rental of additional warehouse space can be added to the fixed operating expenses. 4. By how much would total annual operating income increase above its present level if Proposal 3 is accepted? Explain.arrow_forwardPetoskey Company produces three products: Alanson, Boyne, and Conway. A segmented income statement, with amounts given in thousands, follows: Direct fixed expenses consist of depreciation and plant supervisory salaries. All depreciation on the equipment is dedicated to the product lines. None of the equipment can be sold. Refer to the information for Petoskey Company above. Assume that each of the three products has a different supervisor whose position would be eliminated if the associated product were dropped. Required: Conceptual Connection Estimate the impact on profit that would result from dropping Conway. Explain why Petoskey should keep or drop Conway.arrow_forwardPetoskey Company produces three products: Alanson, Boyne, and Conway. A segmented income statement, with amounts given in thousands, follows: Direct fixed expenses consist of depreciation and plant supervisory salaries. All depreciation on the equipment is dedicated to the product lines. None of the equipment can be sold. Refer to the information for Petoskey Company above. Assume that each of the three products has a different supervisor whose position would remain if the associated product were dropped. Required: Conceptual Connection Estimate the impact on profit that would result from dropping Conway. Explain why Petoskey should keep or drop Conway.arrow_forward

- Departmental Cost Allocation; Outsourcing McKeoun Enterprises is a large machine toolcompany now experiencing alarming increases in maintenance expense in each of its four productiondepartments. Maintenance costs are currently allocated to the production departments on the basisof direct labor hours incurred in the production department. To provide pressure for the productiondepartments to use less maintenance, and to provide an incentive for the maintenance department tobecome more efficient, McKeoun has decided to investigate new methods of allocating maintenancecosts. One suggestion now being evaluated is a form of outsourcing. The producing departmentscould purchase maintenance service from an outside supplier. That is, they could choose either touse an outside supplier of maintenance or to be charged an amount based on their use of direct laborhours. The following table shows the direct labor hours in each department, the allocation of maintenance cost based on labor hours, and…arrow_forwardDepartmental Cost Allocation in Profit Centers Elvis Wilbur owns two restaurants, the BeefBarn and the Fish Bowl. Each restaurant is treated as a profit center for performance evaluation.Although the restaurants have separate kitchens, they share a central baking facility. The principalcosts of the baking area include depreciation and maintenance on the equipment, materials, supplies,and labor.Required2. In May, total fixed and unit variable costs remained the same, but the Beef Barn served 2,000 tables andthe Fish Bowl served 3,000. How much should be allocated to each restaurant? a. Beef Barn: $8,000; Fish Bowl: $16,000b. Beef Barn: $8,800; Fish Bowl: $13,200c. Beef Barn: $9,600; Fish Bowl: $14,400d. Beef Barn: $10,000; Fish Bowl: $12,000arrow_forwardTransfer-pricing dispute. The Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase thecomponent for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its…arrow_forward

- Classify the following decisions as being characteristic of strategic planning, tactical planning, managerial control, or operational control. Determining the mix of products to manufacture this year Examining whether the number of defective goods manufactured is within a certain range Expanding a product line overseas Determining the best distribution route Examining whether the cost of raw materials is within a certain range Examining whether personnel development cost is rising Employing more automated manufacturing this year Examining whether the amount of scrap material is acceptable Building a new plant facility Examining whether employees’ attitudes are improving Examining whether production levels are within a predicted range Making purchasing arrangements with a new supplier Increasing production capabilities this year by purchasing a more efficient piece of machinery Closing a plantarrow_forwardSan Jose Company operates a Manufacturing Division and an Assembly Division. Both divisions are evaluated as profit centers. Assembly buys components from Manufacturing and assembles them for sale. Manufacturing sells many components to third parties in addition to Assembly. Selected data from the two operations follow. Manufacturing Assembly Capacity (units) 408,000 208,000 Sales pricea $ 416 $ 1,340 Variable costsb $ 200 $ 496 Fixed costs $ 40,080,000 $ 24,080,000 a For Manufacturing, this is the price to third parties. b For Assembly, this does not include the transfer price paid to Manufacturing. Suppose Manufacturing is located in Country A with a tax rate of 70 percent and Assembly in Country B with a tax rate of 30 percent. All other facts remain the same. Required: a. Current production levels in Manufacturing are 208,000 units. Assembly requests an additional 48,000 units to produce a special order. What transfer price would…arrow_forwardSan Jose Company operates a Manufacturing Division and an Assembly Division. Both divisions are evaluated as profit centers. Assembly buys components from Manufacturing and assembles them for sale. Manufacturing sells many components to third parties in addition to Assembly. Selected data from the two operations follow. Manufacturing Assembly Capacity (units) 421,000 221,000 Sales pricea $ 442 $ 1,405 Variable costsb $ 265 $ 522 Fixed costs $ 40,210,000 $ 24,210,000 a For Manufacturing, this is the price to third parties. b For Assembly, this does not include the transfer price paid to Manufacturing. Required: a. Current production levels in Manufacturing are 221,000 units. Assembly requests an additional 61,000 units to produce a special order. What transfer price would you recommend? b. Suppose Manufacturing is operating at full capacity. What transfer price would you recommend? c. Suppose Manufacturing is operating at 390,500 units. What…arrow_forward

- Determining transfer pricing The Hernandez Company is decentralized, and divisions are considered investment centers. Hernandez has one division that manufactures oak dining room chairs with upholstered seat cushions. The Chair Division cuts, assembles, and finishes the oak chairs and then purchases and attaches the seat cushions. The Chair Division currently purchases the cushions for $32 from an outside vendor. The Cushion Division manufactures upholstered seat cushions that are sold to customers outside the company. The Chair Division currently sells 1,800 chairs per quarter, and the Cushion Division is operating at capacity, which is 1,800 cushions per quarter. The two divisions report the following information: Requirements Determine the total contribution margin for Hernandez Company for the quarter. Assume the Chair Division purchases the 1,800 cushions needed from the Cushion Division at its current sales price. What is the total contribution margin for each division and the…arrow_forwardEvaluating selling and administrative cost allocations Gordon Gecco Furniture Company has two major product lines with the following characteristics: Commercial office furniture: Few large orders, little advertising support, shipments in full truckloads, and low handling complexity Home office furniture: Many small orders, large advertising support, shipments in partial truckloads, and high handling complexity The company produced the following profitability report for management: The selling and administrative expenses are allocated to the products on the basis of relative sales dollars. Evaluate the accuracy of this report and recommend an alternative approach.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College