Corporate Finance

3rd Edition

ISBN: 9780132992473

Author: Jonathan Berk, Peter DeMarzo

Publisher: Prentice Hall

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 13, Problem 2P

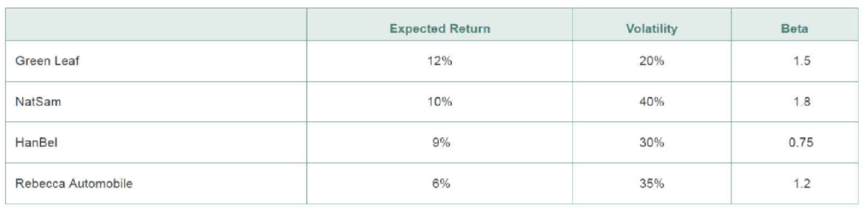

Assume that the

a. At current market prices, which stocks represent buying opportunities?

b. On which stocks should you put a sell order in?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 13 Solutions

Corporate Finance

Ch. 13.1 - If investors attempt to buy a stock with a...Ch. 13.1 - What is the consequence of investors exploiting...Ch. 13.2 - How can an uninformed or unskilled investor...Ch. 13.2 - Under what conditions will it be possible to earn...Ch. 13.3 - Do investors hold well-diversified portfolios?Ch. 13.3 - Why is the high trading volume observed in markets...Ch. 13.3 - What must be true about the behavior of small,...Ch. 13.4 - What are several systematic behavioral biases that...Ch. 13.4 - Prob. 2CCCh. 13.5 - Prob. 1CC

Ch. 13.5 - Prob. 2CCCh. 13.6 - Prob. 1CCCh. 13.6 - Prob. 2CCCh. 13.7 - Prob. 1CCCh. 13.7 - How can you use the Fama-French-Carhart factor...Ch. 13.8 - Which is the most popular method used by...Ch. 13.8 - Prob. 2CCCh. 13 - Assume that all investors have the same...Ch. 13 - Assume that the CAPM is a good description of...Ch. 13 - Prob. 3PCh. 13 - Prob. 4PCh. 13 - Prob. 5PCh. 13 - Explain what the following sentence means: The...Ch. 13 - You are trading in a market in which you know...Ch. 13 - Prob. 8PCh. 13 - Your brother Joe is a surgeon who suffers badly...Ch. 13 - Prob. 11PCh. 13 - Suppose that all investors have the disposition...Ch. 13 - Prob. 14PCh. 13 - Prob. 15PCh. 13 - Prob. 16PCh. 13 - Prob. 17PCh. 13 - Prob. 18PCh. 13 - Prob. 19PCh. 13 - Prob. 20PCh. 13 - Prob. 21PCh. 13 - Prob. 22PCh. 13 - Prob. 23PCh. 13 - Prob. 24PCh. 13 - Prob. 25PCh. 13 - Prob. 26PCh. 13 - Prob. 27PCh. 13 - Prob. 28P

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, finance and related others by exploring similar questions and additional content below.Similar questions

- An analyst has modeled the stock of a company using the Fama-French three-factor model. The market return is 10%, the return on the SMB portfolio (rSMB) is 3.2%, and the return on the HML portfolio (rHML) is 4.8%. If ai = 0, bi = 1.2, ci = 20.4, and di = 1.3, what is the stock’s predicted return?arrow_forwardYou have observed the following returns over time: Assume that the risk-free rate is 6% and the market risk premium is 5%. What are the betas of Stocks X and Y? What are the required rates of return on Stocks X and Y? What is the required rate of return on a portfolio consisting of 80% of Stock X and 20% of Stock Y?arrow_forwardNow assume that the stock is currently selling at $30.29. What is its expected rate of return?arrow_forward

- Market equity beta measures the covariability of a firms returns with all shares traded on the market (in excess of the risk-free interest rate). We refer to the degree of covariability as systematic risk. The market prices securities so that the expected returns should compensate the investor for the systematic risk of a particular stock. Stocks carrying a market equity beta of 1.20 should generate a higher return than stocks carrying a market equity beta of 0.90. Nonsystematic risk is any source of risk that does not affect the covariability of a firms returns with the market. Some writers refer to nonsystematic risk as firm-specific risk. Why is the characterization of nonsystematic risk as firm-specific risk a misnomer?arrow_forwardA stock is trading at $80 per share. The stock is expected to have a yearend dividend of $4 per share (D1 = $4), and it is expected to grow at some constant rate, g, throughout time. The stock’s required rate of return is 14% (assume the market is in equilibrium with the required return equal to the expected return). What is your forecast of gL?arrow_forwardYour client has decided that the risk of the bond portfolio is acceptable and wishes to leave it as it is. Now your client has asked you to use historical returns to estimate the standard deviation of Blandy’s stock returns. (Note: Many analysts use 4 to 5 years of monthly returns to estimate risk, and many use 52 weeks of weekly returns; some even use a year or less of daily returns. For the sake of simplicity, use Blandy’s 10 annual returns.)arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...

Finance

ISBN:9781337395083

Author:Eugene F. Brigham, Phillip R. Daves

Publisher:Cengage Learning

EBK CONTEMPORARY FINANCIAL MANAGEMENT

Finance

ISBN:9781337514835

Author:MOYER

Publisher:CENGAGE LEARNING - CONSIGNMENT

Financial Reporting, Financial Statement Analysis...

Finance

ISBN:9781285190907

Author:James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Publisher:Cengage Learning

Portfolio return, variance, standard deviation; Author: MyFinanceTeacher;https://www.youtube.com/watch?v=RWT0kx36vZE;License: Standard YouTube License, CC-BY