Concept explainers

Videos

Calculating the WACC In the previous problem, suppose the company’s stock has a beta of 1.15. The risk-free rate is 3.7 percent, and the market risk premium is 7 percent. Assume that the overall cost of debt is the weighted average implied by the two outstanding debt issues. Both bonds make semiannual payments. The tax rate is 35 percent. What is the company’s WACC?

To determine: The WACC of the Company.

Introduction: The WACC (Weighted Average Cost of Capital) is the total rate of return for a company which anticipates reimbursing all their investors. It is considered as a financing resource in the target capital structure of a company and it measured in terms of weights of fractions.

Answer to Problem 9QP

The WACC of the Company is 9.87%

Explanation of Solution

Determine the Cost of Equity using CAPM

Therefore the Cost of Equity is 11.75%

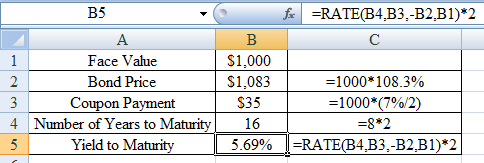

Determine the Yield to Maturity for First Bond Issue

Using excel function =rate we calculate the yield to maturity as,

Excel Spreadsheet:

Therefore the Yield to Maturity for First Bond Issue is 5.69%

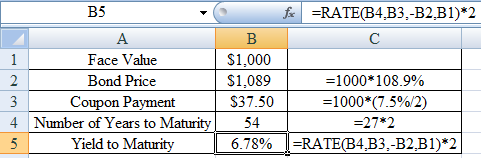

Determine the Yield to Maturity for Second Bond Issue

Using excel function =rate we calculate the yield to maturity as,

Excel Spreadsheet:

Therefore the Yield to Maturity for Second Bond Issue is 6.78%

Determine the Total Market Value of Debt

Therefore the Total Market Value of Debt is $141,150,000

Determine the Market Value of Equity

Therefore the Total Market Value of Equity is $439,900,000

Determine the Total Market Value of Company

Therefore the Total Market Value of Company is $581,050,000

Determine the Market Value Weights of Debt

Therefore the Market Value Weights of Debt is 75.71%

Determine the Market Value Weights of Equity

Therefore the Market Value Weights of Equity is 24.29%

Determine the Weight of First Bond Issue

Therefore the Weight of First Bond Issue is 53.71%

Determine the Weight of Second Bond Issue

Therefore the Weight of Second Bond Issue is 46.29%

Determine the Weighted Average After-tax for both the bond issues

Therefore the Weighted Average After-tax for both the bond issues is 4.03%

Determine the WACC of the Company

Therefore the WACC of the Company is 9.87%.

Want to see more full solutions like this?

Chapter 13 Solutions

CORPORATE FINANCE CUSTOM W/CONNECT >BI

- A company had WACC (weighted average cost of capital) equal to 8. % If the company pays off mortgage bonds with an interest rate of 4% and issues an equal amount of new stock considered to be relatively risky by the market, which of the following is true? a. residual income will increase. b. ROI will decrease. c. WACC will increase. d. WACC will decrease.arrow_forwardAssume that Temp Force has a beta coefficient of 1.2, that the risk-free rate (the yield on T-bonds) is 7.0%, and that the market risk premium is 5%. What is the required rate of return on the firms stock?arrow_forwardPremium for Financial Risk Ethier Enterprise has an unlevered beta of 1.0. Ethier is Financed with 50% debt and has a levered beta of 1.6. If the risk-free rate is 5.5% and the market risk premium is 6%, how much is the additional premium that Ethier’s shareholders require to be compensated for financial risk?arrow_forward

- Consider a firm whose debt has a market value of $35 million and whose stock has a market value of $55 million. The firm pays a 7 percent rate of interest on its new debt and as a beta of 1.23. The corporate tax rate is 21%. Assume that the security market line holds, that the risk premium on the market is 10.5 percent, and that the current Treasury bill is rate is 1 percent. Using the answers from Questions 7 and 8, what is the firm’s WACC?arrow_forwardA) For questions A, B, and C, use the following information: Consider a firm whose debt has a market value of $35 million and whose stock has a market value of $55 million. The firm pays a 7 percent rate of interest on its new debt and has a beta of 1.23. The corporate tax rate is 21%. Assume that the security market line holds, that the risk premium on the market is 10.5 percent, and that the current Treasury bill is rate is 1 percent. What is the aftertax cost of debt? Format as a percentage and round to two places past the decimal point as "X.XX B) Consider a firm whose debt has a market value of $35 million and whose stock has a market value of $55 million. The firm pays a 7 percent rate of interest on its new debt and has a beta of 1.23. The corporate tax rate is 21%. Assume that the security market line holds, that the risk premium on the market is 10.5 percent, and that the current Treasury bill is rate is 1 percent. Using the pretax cost of debt from Question 7, what is the…arrow_forwardAssume that the risk-free rate (i.e., Rf) is 2.8%. If, for a particular company bond issue, the default risk premium (i.e., DP) is 3.1%, the maturity risk premium ( i.e., MP) is 0.9%, and the market risk premium ( i.e., MRP) for that company's stock is 12.9% what is the required rate of return for the company's fixed income securities ? Record your answer as a percent , rounded to one decimal place , but do not include a percent sign in your answer . For example , enter 0.1578658 = 15.78625% as 15.8 .arrow_forward

- Morrison Medical Inc., an all-equity firm, has earnings before interest and taxes of $950,000, an un-levered beta of .80 and a tax rate = 35%. In the market, you observe that Government T-bills are being sold to yield 2% and the S&P/TSX Composite Index is expected to yield 9%. Assume a world with taxes and a cost for the risk of default. All general M&M assumptions apply. You have also been provided the following information: Value of Debt Cost of Debt (Rd) Beta PV of Financial Distress Costs $ 0 - .80 0 $ 5,000,000 5.5% ? $800,000 $ 7,000,000 7.0% 2 ? What is the market value of the firm? What is the market value of the firm and the market value of the equity if they issue $5,000,000 in debt with a coupon rate of 4.5% and use the proceeds to repurchase shares? What is the new cost of equity? According to CAPM, what is the new beta? What is the market value of the firm if the firm issues $7,000,000 in debt? What would be the PV of financial distress costs if…arrow_forwardMorrison Medical Inc., an all-equity firm, has earnings before interest and taxes of $950,000, an un-levered beta of .80 and a tax rate = 35%. In the market, you observe that Government T-bills are being sold to yield 2% and the S&P/TSX Composite Index is expected to yield 9%. Assume a world with taxes and a cost for the risk of default. All general M&M assumptions apply. You have also been provided the following information: Value of Debt Cost of Debt (Rd) Beta PV of Financial Distress Costs $ 0 - .80 0 $ 5,000,000 5.5% ? $800,000 $ 7,000,000 7.0% 2 ? What is the market value of the firm if the firm issues $7,000,000 in debt? What would be the PV of financial distress costs if the firm issues $7,000,000 in debt?arrow_forwardConsider the information below relating to the monthly rates of return for two companies X and Y over a period of 4 months: Y 2 xRate of return yRate of Return Date Month 1 -4.76 -4.75 Month 2 5.34 7.65 Month 3 12.09 6.98 Month 4 -2.98 9.65 a) If a firm increases its financial risk by selling a large bond issue that increases its financial leverage explain this assumption? Also what is the relationship between risk and return. Explain with examples.arrow_forward

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning

Intermediate Financial Management (MindTap Course...FinanceISBN:9781337395083Author:Eugene F. Brigham, Phillip R. DavesPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning