Videos

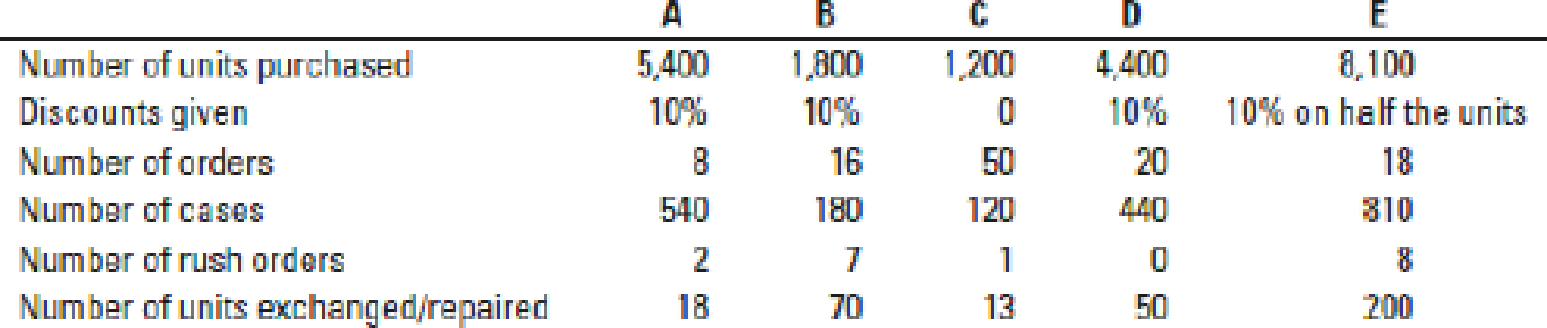

Customer profitability in a manufacturing firm. Mississippi Manufacturing makes a component called B2040. This component is manufactured only when ordered by a customer, so Mississippi keeps no inventory of B2040. The list price is $112 per unit, but customers who place “large” orders receive a 10% discount on price. The customers are manufacturing firms. Currently, the salespeople decide whether an order is large enough to qualify for the discount. When the product is finished, it is packed in cases of 10. If the component needs to be exchanged or repaired, customers can come back within 14 days for free exchange or repair.

The full cost of manufacturing a unit of B2040 is $95. In addition, Mississippi incurs customer-level costs. Customer-level cost-driver rates are:

| Order taking | $360 per order |

| Product handling | $15 per case |

| Rush-order processing | $560 per rush order |

| Exchange and repair costs | $50 per unit |

Information about Mississippi’s five biggest customers follows:

All customers except E ordered units in the same order size. Customer E’s order quantity varied, so E got a discount part of the time but not all the time.

- 1. Calculate the customer-level operating income for these five customers. Use the format in Figure 14-3. Prepare a customer-profitability analysis by ranking the customers from most to least profitable, as in Figure 14-4.

Required

Required

- 2. Discuss the results of your customer-profitability analysis. Does Mississippi have unprofitable customers? Is there anything Mississippi should do differently with its five customers?

Want to see the full answer?

Check out a sample textbook solution

Chapter 14 Solutions

COST ACCOUNTING PLUS NEW MYACCOUNTING L

- Many different businesses employ markup on cost to arrive at a price. For each of the following situations, explain what the markup covers and why it is the amount that it is. a. Department stores have a markup of 100 percent of purchase cost. b. Jewelry stores charge anywhere from 100 percent to 300 percent of the cost of the jewelry. (The 300 percent markup is referred to as keystone.) c. Johnson Construction Company charges 12 percent on direct materials, direct labor, and subcontracting costs. d. Hamilton Auto Repair charges customers for direct materials and direct labor. Customers are charged 45 per direct labor hour worked on their job; however, the employees actually cost Hamilton 15 per hour.arrow_forwardKimball Company has developed the following cost formulas: Materialusage:Ym=80X;r=0.95Laborusage(direct):Yl=20X;r=0.96Overheadactivity:Yo=350,000+100X;r=0.75Sellingactivity:Ys=50,000+10X;r=0.93 where X=Directlaborhours The company has a policy of producing on demand and keeps very little, if any, finished goods inventory (thus, units produced equals units sold). Each unit uses one direct labor hour for production. The president of Kimball Company has recently implemented a policy that any special orders will be accepted if they cover the costs that the orders cause. This policy was implemented because Kimballs industry is in a recession and the company is producing well below capacity (and expects to continue doing so for the coming year). The president is willing to accept orders that minimally cover their variable costs so that the company can keep its employees and avoid layoffs. Also, any orders above variable costs will increase overall profitability of the company. Required: 1. Compute the total unit variable cost. Suppose that Kimball has an opportunity to accept an order for 20,000 units at 220 per unit. Should Kimball accept the order? (The order would not displace any of Kimballs regular orders.) 2. Explain the significance of the coefficient of correlation measures for the cost formulas. Did these measures have a bearing on your answer in Requirement 1? Should they have a bearing? Why or why not? 3. Suppose that a multiple regression equation is developed for overhead costs: Y = 100,000 + 100X1 + 5,000X2 + 300X3, where X1 = direct labor hours, X2 = number of setups, and X3 = engineering hours. The coefficient of determination for the equation is 0.94. Assume that the order of 20,000 units requires 12 setups and 600 engineering hours. Given this new information, should the company accept the special order referred to in Requirement 1? Is there any other information about cost behavior that you would like to have? Explain.arrow_forwardSpecial-Order Decision, Qualitative Aspects Randy Stone, manager of Specialty Paper Products Company, was agonizing over an offer for an order requesting 5,000 boxes of calendars. Specialty Paper Products was operating at 70% of its capacity and could use the extra business. Unfortunately, the orders offering price of 4.20 per box was below the cost to produce the calendars. The controller, Louis Barns, was opposed to taking a loss on the deal. However, the personnel manager, Yatika Blaine, argued in favor of accepting the order even though a loss would be incurred. It would avoid the problem of layoffs and would help to maintain the companys community image. The full cost to produce a box of calendars follows: Later that day, Louis and Yatika met over coffee. Louis sympathized with Yatiks concerns and suggested that the two of them rethink the special-order decision. He offered to determine relevant costs if Yatika would list the activities that would be affected by a layoff. Yatika eagerly agreed and came up with the following activities: an increase in the state unemployment insurance rate from 1% to 2% of total payroll, notification costs to lay off approximately 20 employees, and increased costs of rehiring and retraining workers when the downturn was over. Louis determined that these activities would cost the following amounts: Total payroll is 1,460,000 per year. Layoff paperwork is 25 per laid-off employee. Rehiring and retraining is 150 per new employee. Required: 1. CONCEPTUAL CONNECTION Assume that the company will accept the order only if it increases total profits (without taking the potential layoffs into consideration). Should the company accept or reject the order? Provide supporting computations. 2. CONCEPTUAL CONNECTION Consider the new information on activity costs associated with the layoff. Should the company accept or reject the order? Provide supporting computations.arrow_forward

- Deuce Sporting Goods manufactures a high-end model tennis racket. The company’s forecasted income statement for the year, before any special orders, is as follows: Fixed costs included in the forecasted income statement are $400,000 in manufacturing cost of goods sold and $200,000 in selling expenses. A new client placed a special order with Deuce, offering to buy 1,000 tennis rackets for $100.00 each. The company will incur no additional selling expenses if it accepts the special order. Assuming that Deuce has sufficient capacity to manufacture 1,000 more tennis rackets, by what amount would differential income increase (decrease) as a result of accepting the special order? (Hint: First compute the variable cost per unit relevant to this decision.)arrow_forwardCarpetland salespersons average 8,000 per week in sales. Steve Contois, the firms vice president, proposes a compensation plan with new selling incentives. Steve hopes that the results of a trial selling period will enable him to conclude that the compensation plan increases the average sales per salesperson. a. Develop the appropriate null and alternative hypotheses. b. What is the Type I error in this situation? What are the consequences of making this error? c. What is the Type II error in this situation? What are the consequences of making this error?arrow_forwardReubens Deli currently makes rolls for deli sandwiches it produces. It uses 30,000 rolls annually in the production of deli sandwiches. The costs to make the rolls are: A potential supplier has offered to sell Reuben the rolls for $0.90 each. If the rolls are purchased, 30% of the fixed overhead could be avoided, If Reuben accepts the offer, what will the effect on profit be?arrow_forward

- Rugged Outfitters purchases one model of mountain bike at a wholesale cost of $520 per unit and resells it to end consumers. The annual demand for the company’s product is 49,000 units. Ordering costs are $500 per order and carrying costs are $100 per bike per year, including $40 in the opportunity cost of holding inventory. QWhat is the cost impact on the company of excluding the opportunity cost of carrying inventory when making EOQ decisions? Why do you think the company currently excludes the opportunity costs of carrying inventory when evaluating the manager’s performance? What could the company do to encourage the manager to make decisions more congruent with the goal of reducing total inventory costs?arrow_forwardBreok-Even and Target Profit Analysis The Shirt Works sells a large variety of tee shirts and sweatshirts. Steve Hooper, the owner, is thinking of expanding his sales by hiring high school students, on a commission basis, to sell sweatshirts bearing the name and mascot of the local high school. These sweatshirts would have to be ordered from the manufacturer six weeks in advance, and they could not be returned because of the unique printing required. The sweatshirts would cost Hooper $8 each with a minimum order of 75 sweatshirts. Any additional sweatshirts would have to be ordered in increments of 75. Since Hooper’s plan would not require any additional facilities, the only costs associated with the project would be the costs of the sweatshirts and the costs of the sales commissions. The selling price of the sweatshirts would be $13.50 each. Hooper would pay the students a commission of $1.50 for each shirt sold. Required: 1. What level of unit sales and dollar sales is needed to…arrow_forwardAlawi Company currently sells 10,000 units of product M for P 18.00 each. Variable costs are P 8.00 per unit. A discount store has offered P 16.00 for 4,000 units of product M. The managers believe that if they accept the special order, they will lose some sales at the regular price. Determine the number of units Alawi could lose before the order became unprofitable. a. 2,000 unitsb. 2,667 unitsc. 3,200 unitsd. 5,000 unitsarrow_forward

- JAM is a major manufacturer of household goods. Distribution method Total cost per year: Website Sales $20,000 Retailer Stockists $40,000 Wholesale Stockists $15,000 Industry Catalogue Sales $7,000 Sales made at factory site $4,500 Calculate the total cost saving that JAM would make if it eliminates all indirect distribution channels of sale. Give your answer to the nearest whole $. Do not include symbols, commas or letters in your response.arrow_forwardNUBD Co. currently sells 1,000 units of product M for P2 each. Variable costs are P1.50. A discount store has offered P1.70 per unit for 400 units of product M. The managers believe that if they accept the special order, they will lose some sales at the regular price. Determine the number of units they could lose before the order become unprofitablearrow_forwardTim’s Bicycle Shop sells 21-speed bicycles. For purposes of a cost-volume-profit analysis, the shop owner has divided sales into two categories, as follows: product type sales price price invoice cost sales commission high quality 1850 840 100 medium quality 920 620 40 Three-quarters of the shop’s sales are medium-quality bikes. The shop’s annual fixed expenses are $270,400. (In the following requirements, ignore income taxes.)a. What is the shop’s break-even sales volume in dollars? Assume a constant sales mix.b. How many bicycles of each type must be sold to earn a target net income of $126,750? Assume a constant sales mix.arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College