Concept explainers

Videos

FIFO method (continuation of 17-41).

- 1. Complete Problem 17-41 using the FIFO method of

process costing .

Required

- 2. If you did Problem 17-41, explain any difference between the cost of work completed and transferred out and the cost of ending work in process in the assembly department under the weighted-average method and the FIFO method. Should McKnight’s managers choose the weighted-average method or the FIFO method? Explain briefly.

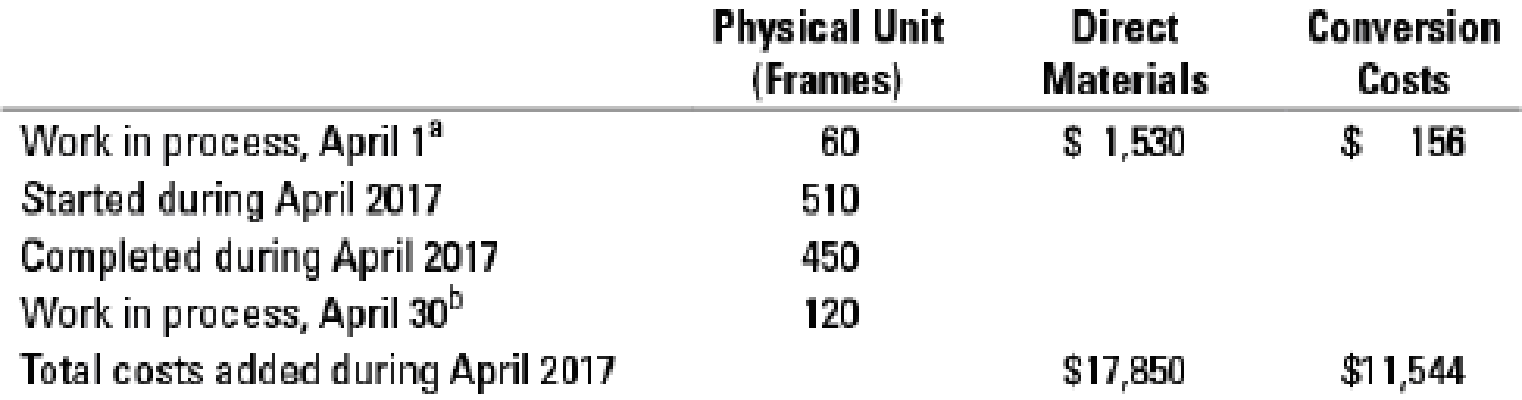

17-41 Weighted-average method. McKnight Handcraft is a manufacturer of picture frames for large retailers. Every picture frame passes through two departments: the assembly department and the finishing department. This problem focuses on the assembly department. The process-costing system at McKnight has a single direct-cost category (direct materials) and a single indirect-cost category (conversion costs). Direct materials are added when the assembly department process is 10% complete. Conversion costs are added evenly during the assembly department’s process.

McKnight uses the weighted-average method of process costing. Consider the following data for the assembly department in April 2017:

a Degree of completion: direct materials, 100%; conversion costs, 40%.

b Degree of completion: direct materials, 100%; conversion costs, 15%.

- 1. Summarize the total assembly department costs for April 2017, and assign them to units completed (and transferred out) and to units in ending work in process.

Required

- 2. What issues should a manager focus on when reviewing the equivalent units calculation?

Want to see the full answer?

Check out a sample textbook solution

Chapter 17 Solutions

Horngren's Cost Accounting Plus MyLab Accounting with Pearson eText -- Access Card Package (16th Edition)

- For E2-17, prepare any journal entries that would have been different if the only trigger points had been the purchase of materials and the sale of finished goods. Davis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forwardLampierre makes brass and gold frames. The company computed this information to decide whether to switch from the traditional allocation method to ABC: The estimated overhead for the material cost pool is estimated as $12,500, and the estimate for the machine setup pool is $35,000. Calculate the allocation rate per unit of brass and per unit of gold using: A. The traditional allocation method B. The activity-based costing methodarrow_forward

- Mt. Palomar Manufacturing Co. uses a process cost system. Its manufacturing operation is carried on in two departments: Machining and Finishing. The Machining Department uses the weighted average cost method, and the Finishing Department uses the FIFO cost method. Materials are added in both departments at the beginning of operations, but the added materials do not increase the number of units being processed. Units are lost in the Machining Department throughout the production process, and inspection occurs at the end of the process. The lost units have no scrap value and are considered to be a normal loss. Production statistics for July show the following data: Required: Prepare a cost of production summary for each department. (Round unit costs to three decimal places.) Which department will have an easier time determining how its unit costs compare from month to month? Why?arrow_forwardThe management of Gwinnett County Chrome Company, described in Problem 1A, now plans to use the multiple production department factory overhead rate method. The total factory overhead associated with each department is as follows: Instructions 1. Determine the multiple production department factory overhead rates, using direct labor hours for the Stamping Department and machine hours for the Plating Department. 2. Determine the product factory overhead costs, using the multiple production department rates in (1).arrow_forwardYellowstone Fabricators uses a process cost system and applies actual factory overhead to work in process at the end of the month. The following data came from the records for March: There were no beginning inventories and no ending work in process inventory. From the information presented, compute the following: 1. Unit cost of production under absorption costing and variable costing. 2. Cost of the ending inventory under absorption costing and variable costing.arrow_forward

- Davis Co. uses backflush costing to account for its manufacturing costs. The trigger points are the purchase of materials, the completion of goods, and the sale of goods. Prepare journal entries to account for the following: a. Purchased raw materials, on account, 70,000. b. Requisitioned raw materials to production, 70,000. c. Distributed direct labor costs, 15,000. d. Factory overhead costs incurred, 45,000. (Use Various Credits for the account in the credit part of the entry.) e. Completed all of the production started. f. Sold the completed production for 195,000, on account. (Hint: Use a single account for raw materials and work in process.)arrow_forwardA company has traditionally allocated its overhead based on machine hours but collected this information to change to activity based costing: A. How much overhead would be assigned to each unit under the traditional allocation method? B. How much overhead would be assigned to each unit under activity-based costing?arrow_forwardCarltons Kitchens three cost pools and overhead estimates are as follows: Compare the overhead allocation using: A. The traditional allocation method B. The activity-based costing method (Hint: the traditional method uses machine hours as the allocation base.)arrow_forward

- Which of the following product situations is better suited to job order costing than to process costing? A. Each product batch is exactly the same as the prior batch. B. The costs are easily traced to a specific product. C. Costs are accumulated by department. D. The value of work in process is based on assigning standard costs.arrow_forwardFIFO Method, Single Department Analysis, One Cost Category Refer to the data in Problem 6.33. Required: Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.arrow_forwardRoberts Company produces two weed eaters: basic and advanced. The company has four activities: machining, engineering, receiving, and inspection. Information on these activities and their drivers is given below. Overhead costs: Required: 1. Calculate the four activity rates. 2. Calculate the unit costs using activity rates. Also, calculate the overhead cost per unit. 3. What if consumption ratios instead of activity rates were used to assign costs instead of activity rates? Show the cost assignment for the inspection activity.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College