Concept explainers

Videos

1.

Allocate the company’s service department costs using the direct method combined with dual allocation.

1.

Explanation of Solution

Service department: A service department is a division in an organization which is not involved directly in producing the goods or services of an organization. But, the service department also offers a service that aids the organization to take place the goods or services that are produced.

Allocate the company’s service department costs using the direct method combined with dual allocation as follows:

Variable costs:

| Provider of Service | Cost to be allocated (a) | Production Departments | |||

| Machining | Assembly | ||||

| Proportion (b) | Amount ($) | Proportion (c) | Amount | ||

| Human resource | $50,000 | $22,222 | $27,778 | ||

| Maintenance | 80,000 | 37,333 | 42,667 | ||

| Computer aided design | 50,000 | 37,500 | 12,500 | ||

| Total | $180,000 | $97,055 | $82,945 | ||

| Grand total | $830,000 | ||||

Table (1)

Note:

The proportions are based on short-run usage.

Fixed costs:

| Provider of Service | Cost to be allocated (a) | Production Departments | |||

| Machining | Assembly | ||||

| Proportion (b) | Amount ($) | Proportion (c) | Amount | ||

| Human resource | $200,000 | $82,353 | $117,647 | ||

| Maintenance | 150,000 | 100,000 | 50,000 | ||

| Computer aided design | 300,000 | 240,000 | 60,000 | ||

| Total | $650,000 | $422,353 | $227,647 | ||

| Grand total | $650,000 | ||||

Table (2)

Note:

The proportions are based on long-run usage.

Total cost allocated:

| Particulars | Machining | Assembly |

| Variable costs | $ 97,055 | $ 82,945 |

| Fixed costs | 422,353 | 227,647 |

| Total costs | $519,408 | $310,592 |

| Grand total | 830,000 | |

Table (3)

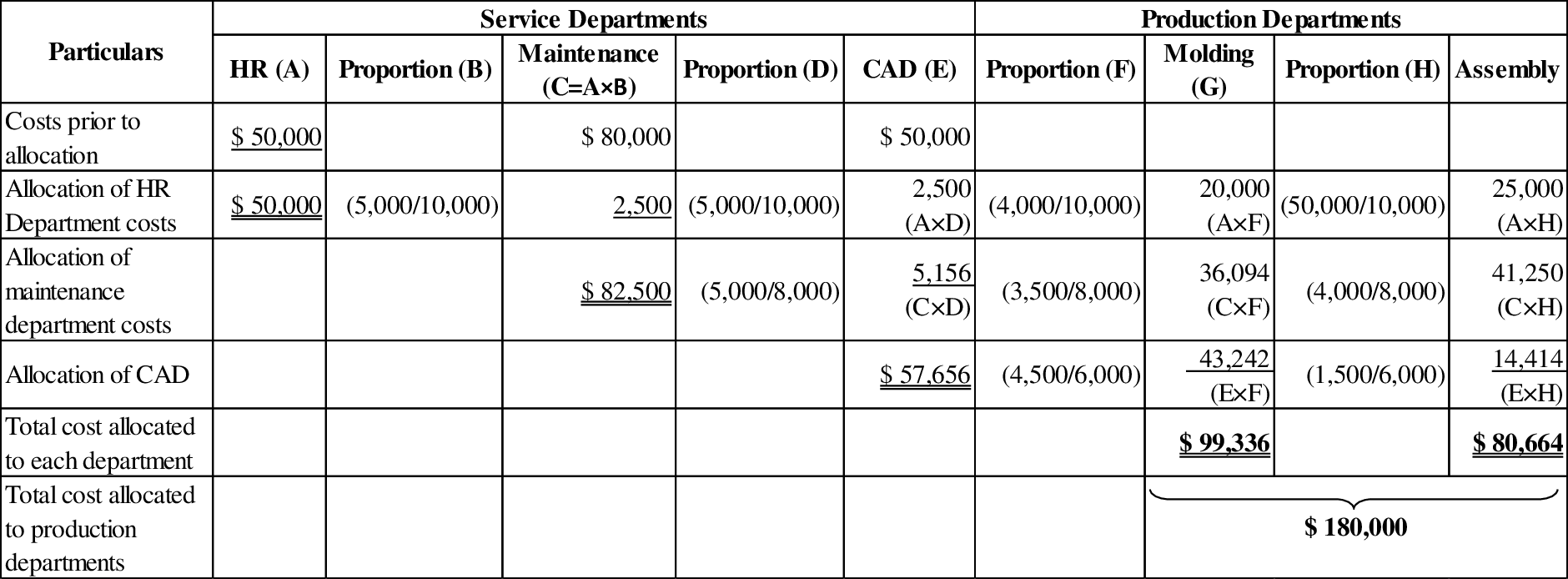

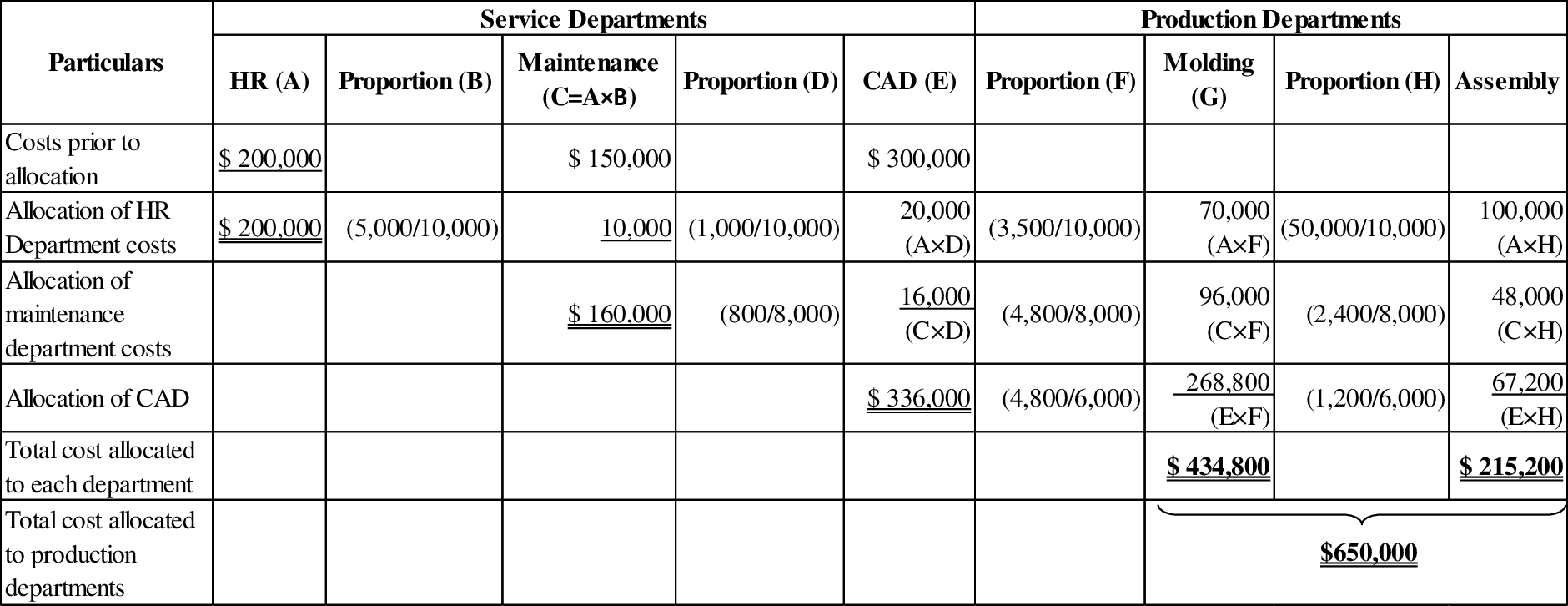

2.

Allocate the company’s service department costs using the step-down method combined with dual allocation.

2.

Explanation of Solution

Allocate the company’s service department costs using the step-down method combined with dual allocation:

Variable costs:

Table (4)

Fixed costs:

Table (5)

Total cost allocated:

| Particulars | Machining | Assembly |

| Variable costs | $ 99,336 | $80,664 |

| Fixed costs | 434,800 | 215,200 |

| Total costs | $534,136 | $295,864 |

| Grand total | 830,000 | |

Table (6)

Want to see more full solutions like this?

Chapter 17 Solutions

GEN COMBO MANAGERIAL ACCOUNTING; CONNECT ACCESS CARD

- Refer to the data in Exercise 7.22. The company has decided to simplify its method of allocating support service costs by switching to the direct method. Required: 1. Allocate the costs of the support departments to the producing departments using the direct method. (Round allocation ratios to four significant digits. Round allocated costs to the nearest dollar.) 2. Using direct labor hours, compute departmental overhead rates. (Round to the nearest cent.)arrow_forwardYoung Company is beginning operations and is considering three alternatives to allocate manufacturing overhead to individual units produced. Young can use a plantwide rate, departmental rates, or activity-based costing. Young will produce many types of products in its single plant, and not all products will be processed through all departments. In which one of the following independent situations would reported net income for the first year be the same regardless of which overhead allocation method had been selected? a. All production costs approach those costs that were budgeted. b. The sales mix does not vary from the mix that was budgeted. c. All manufacturing overhead is a fixed cost. d. All ending inventory balances are zero.arrow_forwardThe management of Wheeler Company has decided to develop cost formulas for its major overhead activities. Wheeler uses a highly automated manufacturing process, and power costs are a significant manufacturing cost. Cost analysts have decided that power costs are mixed; thus, they must be broken into their fixed and variable elements so that the cost behavior of the power usage activity can be properly described. Machine hours have been selected as the activity driver for power costs. The following data for the past eight quarters have been collected: Required: 1. Prepare a scattergraph by plotting power costs against machine hours. Does the scatter-graph show a linear relationship between machine hours and power cost? 2. Using the high and low points, compute a power cost formula. 3. Use the method of least squares to compute a power cost formula. Evaluate the coefficient of determination. 4. Rerun the regression and drop the point (20,000; 26,000) as an outlier. Compare the results from this regression to those for the regression in Requirement 3. Which is better?arrow_forward

- Classify the following cost drivers as structural, executional, or operational. a. Number of plants b. Number of moves c. Degree of employee involvement d. Capacity utilization e. Number of product lines f. Number of distribution channels g. Engineering hours h. Direct labor hours i. Scope j. Product configuration k. Quality management approach l. Number of receiving orders m. Number of defective units n. Employee experience o. Types of process technologies p. Number of purchase orders q. Type and efficiency of layout r. Scale s. Number of functional departments t. Number of planning meetingsarrow_forwardSupport department cost allocation Blue Mountain Masterpieces produces pictures, paintings, and other home decor. The Printing and Framing production departments are supported by the Janitorial and Security departments. Janitorial costs are allocated to the production departments based on square feet, and security costs are allocated based on asset value. Information about these departments is detailed in the following table: Management has experimented with different support department cost allocation methods in the past. The different allocation methods did not yield large differences of cost allocation to the production departments. Instructions 1. Determine which support department cost allocation method Blue Mountain Masterpieces would most likely use to allocate its support department costs to the production departments. 2. Determine the total costs allocated from each support department to each production department using the method you determined in part (1). 3. Without doing calculations, consider and answer the following: If Blue Mountain Masterpieces decided to use square feet instead of asset value as the cost driver for security services, how would this change the allocation of Security Department costs?arrow_forwardThe management of Hartman Company is trying to determine the amount of each of two products to produce over the coming planning period. The following information concerns labor availability, labor utilization, and product profitability: a. Develop a linear programming model of the Hartman Company problem. Solve the model to determine the optimal production quantities of products 1 and 2. b. In computing the profit contribution per unit, management does not deduct labor costs because they are considered fixed for the upcoming planning period. However, suppose that overtime can be scheduled in some of the departments. Which departments would you recommend scheduling for overtime? How much would you be willing to pay per hour of overtime in each department? c. Suppose that 10, 6, and 8 hours of overtime may be scheduled in departments A, B, and C, respectively. The cost per hour of overtime is 18 in department A, 22.50 in department B, and 12 in department C. Formulate a linear programming model that can be used to determine the optimal production quantities if overtime is made available. What are the optimal production quantities, and what is the revised total contribution to profit? How much overtime do you recommend using in each department? What is the increase in the total contribution to profit if overtime is used?arrow_forward

- A manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardRefer to the data in Exercise 7.18. When the capacity of the HR Department was originally established, the normal usage expected for each department was 20,000 direct labor hours. This usage is also the amount of activity planned for the two departments in Year 1 and Year 2. Required: 1. Allocate the costs of the HR Department using the direct method and assuming that the purpose is product costing. 2. Allocate the costs of the HR Department using the direct method and assuming that the purpose is to evaluate performance.arrow_forwardA manufacturing company has two service and two production departments. Building Maintenance and Factory Office are the service departments. The production departments are Assembly and Machining. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The building maintenance department services all departments of the company, and its costs are allocated using floor space occupied, while factory office costs are allocable to Assembly and Machining on the basis of direct labor hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forward

- Explain why either normal or peak capacity of the producing (or user) departments should be used to allocate the fixed costs of support departments.arrow_forwardData Master is a computer software consulting company. Its three major functional areas are computer programming, information systems consulting, and software training. Cynthia Moore, a pricing analyst in the Accounting Department, has been asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing these costs, Moore is considering three different methods of allocating overhead costs-the direct method, the step method, and the reciprocal method. Moore assembled the following data on overhead from its two service departments, the Information Systems Department and the Facilities Department. Service Departments User Departments Info Systems Facilities Computer Program Consult Training Total Budgeted Overhead $ 50,000 $ 25,000 $ 75,000 $ 110,000 $ 85,000 $ 345,000 Info Systems (hrs.) 400 1,100 600 900 3,000 Facilities (Square feet) 200,000…arrow_forwardBoysenberry Corp. has two support departments, Personnel (P) and Maintenance (M), and two producing departments, Blending (B) and Finishing (F). Estimated direct costs and percentages of services used by these departments are as follows: Used by Department Support Dept. P M B F P - 10% 60% 30% M 10% - 40% 50% Direct costs Required: $9,000 $13,500 $40,000 $35,000 Prepare a schedule allocating the support department costs to the producing departments using the direct allocation method. Prepare a schedule allocating the support department costs to the producing departments using the sequential allocation method.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning

Essentials of Business Analytics (MindTap Course ...StatisticsISBN:9781305627734Author:Jeffrey D. Camm, James J. Cochran, Michael J. Fry, Jeffrey W. Ohlmann, David R. AndersonPublisher:Cengage Learning