Concept explainers

Videos

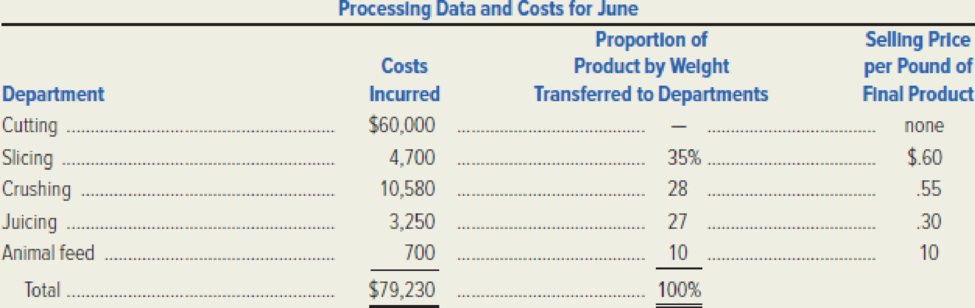

Top Quality Fruit Company, based on Oahu, grows, processes, cans, and sells three main pineapple products: sliced, crushed, and juice. The outside skin is cut off in the Cutting Department and processed as animal feed. The feed is treated as a by-product. The company’s production process is as follows:

- Pineapples first are processed in the Cutting Department. The pineapples are washed and the outside skin is cut away. Then the pineapples are cored and trimmed for slicing. The three main products (sliced, crushed, juice) and the by-product (animal feed) are recognizable after processing in the Cutting Department. Each product then is transferred to a separate department for final processing.

- The trimmed pineapples are sent to the Slicing Department, where the pineapples are sliced and canned. Any juice generated during the slicing operation is packed in the cans with the slices.

- The pieces of pineapple trimmed from the fruit are diced and canned in the Crushing Department. Again, the juice generated during this operation is packed in the can with the crushed pineapple.

- The core and surplus pineapple generated from the Cutting Department are pulverized into a liquid in the Juicing Department. There is an evaporation loss equal to 8 percent of the weight of the good output produced in this department that occurs as the juices are heated.

- The outside skin is chopped into animal feed in the Feed Department.

Top Quality Fruit Company uses the net-realizable-value method to assign the costs of the joint process to its main products. The net realizable value of the by-product is subtracted from the joint cost before the allocation.

A total of 270,000 pounds were entered into the Cutting Department during June. The following schedule shows the costs incurred in each department, the proportion by weight transferred to the four final processing departments, and the selling price of each end product.

Required: Compute each of the following amounts.

- 1. The number of pounds of pineapple that result as output for pineapple slices, crushed pineapple, pineapple juice, and animal feed.

- 2. The net realizable value at the split-off point of the three main products.

- 3. The amount of the cost of the Cutting Department allocated to each of the three main products.

Want to see the full answer?

Check out a sample textbook solution

Chapter 17 Solutions

Managerial Accounting: Creating Value in a Dynamic Business Environment

- Old Country Links, Incorporated, produces sausages in three production departments—Mixing, Casing and Curing, and Packaging. In the Mixing Department, meats are prepared and ground and then mixed with spices. The spiced meat mixture is then transferred to the Casing and Curing Department, where the mixture is force-fed into casings and then hung and cured in climate-controlled smoking chambers. In the Packaging Department, the cured sausages are sorted, packed, and labeled. The company uses the weighted-average method in its process costing system. Data for September for the Casing and Curing Department follow: Units Percent Completed Mixing Materials Conversion Work in process inventory, September 1 1 100% 90% 80% Work in process inventory, September 30 1 100% 80% 70% Mixing Materials Conversion Work in process inventory, September 1 $ 1,670 $ 90 $ 605 Cost added during September $ 81,460 $ 6,006 $ 42,490 Mixing cost represents the costs of the spiced…arrow_forwardAmazon Beverages produces and bottles a line of soft drinks using exotic fruits from Latin America and Asia. The manufacturing process entails mixing and adding juices and coloring ingredients at the bottling plant, which is a part of Mixing Division. The finished product is packaged in a company-produced glass bottle and packed in cases of 24 bottles each. Because the appearance of the bottle heavily influences sales volume, Amazon developed a unique bottle production process at the company’s container plant, which is a part of Container Division. Mixing Division uses all of the container plant’s production. Each division (Mixing and Container) is considered a separate profit center and evaluated as such. As the new corporate controller, you are responsible for determining the proper transfer price to use for the bottles produced for Mixing Division. At your request, Container Division’s general manager asked other bottle manufacturers to quote a price for the number and sizes…arrow_forwardOld Country Links, Incorporated, produces sausages in three production departments—Mixing, Casing and Curing, and Packaging. In the Mixing Department, meats are prepared, ground and mixed with spices. The spiced meat mixture is transferred to the Casing and Curing Department, where the mixture is force-fed into casings and hung and cured in climate-controlled smoking chambers. In the Packaging Department, the cured sausages are sorted, packed, and labeled. The company uses the weighted-average method of process costing. Data for September for the Casing and Curing Department follow: Units Percent Completed Mixing Materials Conversion Work in process inventory, September 1 1 100% 60% 50% Work in process inventory, September 30 1 100% 20% 10% Mixing Materials Conversion Work in process inventory, September 1 $ 1,640 $ 26 $ 105 Cost added during September $ 94,740 $ 8,402 $ 61,197 Mixing cost represents the costs of the spiced meat mixture transferred in from…arrow_forward

- Cooperative San José of southern Sonora state in Mexico makes a unique syrup using cane sugar and local herbs. The syrup is sold in small bottles and is prized as a flavoring for drinks and for use in desserts. The bottles are sold for $12 each. The first stage in the production process is carried out in the Mixing Department, which removes foreign matter from the raw materials and mixes them in the proper proportions in large vats. The company uses the weighted-average method in its process costing system. A hastily prepared report for the Mixing Department for April appears below: Units to be accounted for: Work in process, April 1 (materials 90% complete;conversion 80% complete) 30,000 Started into production 200,000 Total units to be accounted for 230,000 Units accounted for as follows: Transferred to next department 190,000 Work in process, April 30 (materials 75% complete;conversion 60% complete) 40,000 Total units accounted for 230,000…arrow_forwardCooperative San José of southern Sonora state in Mexico makes a unique syrup using cane sugar and local herbs. The syrup is sold in small bottles and is prized as a flavoring for drinks and for use in desserts. The bottles are sold for $12 each. The first stage in the production process is carried out in the Mixing Department, which removes foreign matter from the raw materials and mixes them in the proper proportions in large vats. The company uses the weighted-average method in its process costing system. A hastily prepared report for the Mixing Department for April appears below: Units to be accounted for: Work in process, April 1 (materials 90% complete;conversion 80% complete) 30,000 Started into production 200,000 Total units to be accounted for 230,000 Units accounted for as follows: Transferred to next department 190,000 Work in process, April 30 (materials 75% complete;conversion 60% complete) 40,000 Total units accounted for 230,000…arrow_forwardGroFast Company manufactures a high-quality fertilizer, which is used primarily by commercial veg-etable growers. Two departments are involved in the production process. In the Mixing Department, various chemicals are entered into production. After processing, the Mixing Department transfers a chemical called Chemgro to the Finishing Department. There the product is completed, packaged, and shipped under the brand name Vegegro. Various chemicals --> Mixing Dept (Chemgro)-->Finishing Dept (Vegegro) ---> In the Mixing Department, the raw material is added at the beginning of the process. Labor and overhead are applied continuously throughout the process. All direct departmental overhead is traced to the departments, and plant overhead is allocated to the departments on the basis of direct-labor. The plant overhead rate for 20x2 is $.40 per direct-labor dollar. The following information relates to production during November 20x2 in the Mixing Department. a. Work in process,…arrow_forward

- Mack's Juices produces and bottles a line of fruit juices. The manufacturing process entails mixing and adding juices and other ingredients at the bottling plant, which is a part of Blending Division. The finished product is packaged in a company-produced glass bottle and packed in cases of 24 bottles each. Because the appearance of the bottle heavily influences sales volume, Mack's developed a unique bottle production process at the company’s container plant, which is a part of Packaging Division. Blending Division uses all of the container plant’s production. Each division (Blending and Packaging) is considered a separate profit center and evaluated as such. As the new corporate controller, you are responsible for determining the proper transfer price to use for the bottles produced for Blending Division. At your request, Packaging Division’s general manager asked other bottle manufacturers to quote a price for the number and sizes demanded by Blending Division. These competitive…arrow_forwardTourneSol Canada, Ltd. is a producer of high quality sunflower oil. The company buys raw sunflower seeds directly from large agricultural companies, and refines the seeds into sunflower oil that it sells in the wholesale market. As a by-product, the company also produces sunflower mash (a paste made from the remains of crushed sunflower seeds) that it sells into the market as base product for animal feed. The company has a maximum input capacity of 150 short tons of raw sunflower seeds every day (or 54,750 short tons per year). Of course the company cannot run at full capacity every day as it is required to shut down or reduce capacity for maintenance periods every year, and it experiences the occasional mechanical problem. The facility is expected to run at 90% capacity over the year (or on average 150 x 90% = 135 short tons per day). TourneSol is planning to purchase its supply of raw sunflower seeds from three primary growers, Supplier A, Supplier B, and Supplier C. Purchase prices…arrow_forwardHealthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.arrow_forward

- Carleigh, Inc., is a pork processor. Its plants, located in the Midwest, produce several products from a common process: sirloin roasts, chops, spare ribs, and the residual. The roasts, chops, and spare ribs are packaged, branded, and sold to supermarkets. The residual consists of organ meats and leftover pieces that are sold to sausage and hot dog processors. The joint costs for a typical week are as follows: The revenues from each product are as follows: sirloin roasts, 68,000; chops, 71,000; spare ribs, 33,000; and residual, 9,800. Carleighs management has learned that certain organ meats are a prized delicacy in Asia. They are considering separating those from the residual and selling them abroad for 52,000. This would bring the value of the residual down to 2,650. In addition, the organ meats would need to be packaged and then air freighted to Asia. Further processing cost per week is estimated to be 27,500 (the cost of renting additional packaging equipment, purchasing materials, and hiring additional direct labor). Transportation cost would be 12,100 per week. Finally, resource spending would need to be expanded for other activities as well (purchasing, receiving, and internal shipping). The increase in resource spending for these activities is estimated to be 3,120 per week. Required: 1. What is the gross profit earned by the original mix of products for one week? 2. Should the company separate the organ meats for shipment overseas or continue to sell them at split-off? What is the effect of the decision on weekly gross profit?arrow_forwardGolding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: Karen: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input. Aaron: Your predecessor is responsible. He believed that tracking the difference in material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. Karen: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern. Aaron: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials. c. The pattern department experienced the following costs: d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the pattern department, assuming that process costing is totally appropriate. Round unit cost to two decimal places. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. Round unit cost to two decimal places. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?arrow_forwardA dedicated pharmaceutical plant uses the theory of constraints and has three processes: Mixing, Encapsulating, and Packaging. For Mixing, sufficient materials are released to produce 4,000 packages of product per day. Encapsulating has a buffer inventory of 8,000 units (work in process from Mixing). Packaging produces 4,000 units per day. Which of the three processes sets the production rate of 4,000 units per day? a. The Mixing Department b. The Encapsulating Department c. The Packaging Department d. Cannot be determinedarrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning