Concept explainers

Videos

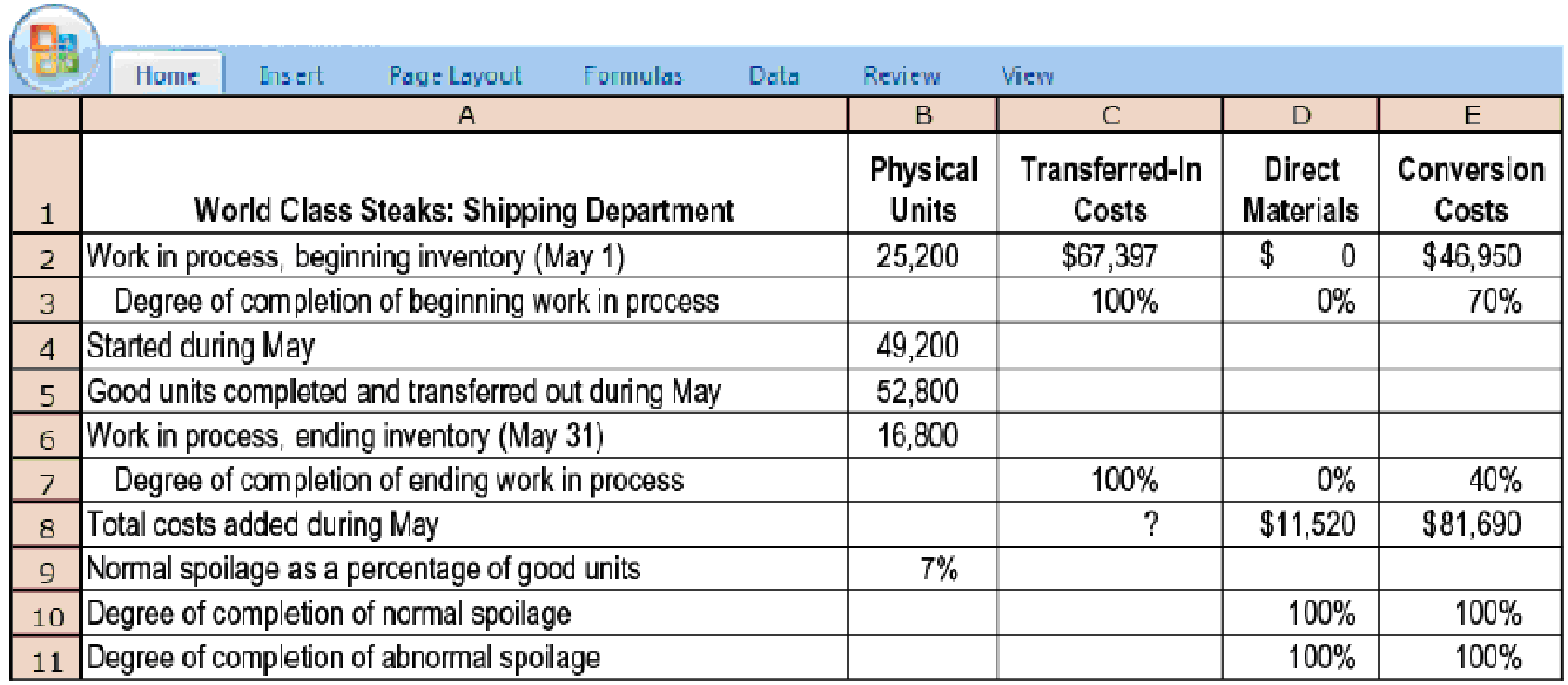

Weighted-average method, shipping department (continuation of 18-35). In the shipping department of World Class Steaks, conversion costs are added evenly during the process, and direct materials are added at the end of the process. Spoiled units are detected upon inspection at the end of the process and are disposed of at zero net disposal value. All completed work is transferred to the next department. The transferred-in costs for May equal the total cost of good units completed and transferred out in May from the prep department, which were calculated in Problem 18-35 using the weighted-average method of

Required

For the shipping department, use the weighted-average method to summarize the total costs to account for and assign those costs to units completed and transferred out (including normal spoilage), to abnormal spoilage, and to units in ending work in process.

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

EBK HORNGREN'S COST ACCOUNTING

- The Converting Department of Worley Company had 2,400 units in work in process at the beginning of the period, which were 35% complete. During the period, 10,800 units were completed and transferred to the Packing Department. There were 1,900 units in process at the end of the period, which were 60% complete. Direct materials are placed into the process at the beginning of production. Determine the number of equivalent units of production with respect to direct materials and conversion costs.arrow_forwardProduction information shows these costs and units for the smoothing department in August. All materials are added at the beginning of the period. The ending work in process is 30% complete as to conversion. What is the value of the inventory transferred to finished goods and the value of the WIP inventory at the end of the month?arrow_forwardK-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.arrow_forward

- The standard cost summary for the most popular product of Phenom Products Co. is shown as follows, together with production and cost data for the period. One gallon each of liquid lead and varnish are added at the start of processing. The balance of the materials is added when the process is two-thirds complete. Labor and overhead are added evenly throughout the process. There were no units in process at the beginning of the month. Required: Calculate equivalent production for materials, labor, and overhead. (Be sure to refer to the standard cost summary to help determine the percentage of materials in ending work in process.) Calculate materials and labor variances and indicate whether they are favorable or unfavorable, using the diagram format shown in Figure 8-4. Determine the cost of materials and labor in the work in process account at the end of the month.arrow_forwardThe Converting Department of Osaka Napkin Company uses the average cost method and had 2,200 units in work in process that were 60% complete at the beginning of the period. During the period, 27,700 units were completed and transferred to the Packing Department. There were 1,200 units in process that were 10% complete at the end of the period. a. Determine the number of whole units to be accounted for and to be assigned costs for the period. 0 units b. Determine the number of equivalent units of production for the period. unitsarrow_forwardTerminal Industries (TI) produces a product using three departments: Mixing, Processing, and Filtering. New material is added only in the Mixing Department. The following information is given for the Processing Department for August. Tl uses process costing. WIP Inventory Processing Department: August 1 Quantity (60% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 1 Current production and costs (August) Units started Current costs Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total current cost: August WIP Inventory Processing Department (August 31) Quantity (20% complete) Transferred-in costs (from Mixing Department). Conversion costs (Processing Department) Total WIP cost: August 31 Required: 30,250 units $ 39,470 13,702 $ 53,172 77,250 units $ 89,700 57,600 $ 147,300 15,250 units a. Complete the production cost report for August using the weighted average method. Note:…arrow_forward

- help mearrow_forwardTerminal Industries (TI) produces a product using three departments: Mixing, Processing, and Filtering. New material is added only in the Mixing Department. The following information is given for the Processing Department for August. Tl uses process costing. WIP Inventory Processing Department: August 1 Quantity (60% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 1 Current production and costs (August) Units started Current costs Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total current cost: August WIP Inventory Processing Department (August 31) Quantity (20% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 31 28,000 units $ 33,890 13,612 $ 47,502 75,000 $ 82,500 53,060 $ 135,560 units 13,000 units ?? ?? ?? Required: a. Complete the production cost report for August using the weighted-average method.…arrow_forwardTerminal Industries (TI) produces a product using three departments: Mixing, Processing, and Filtering. New material is added only in the Mixing Department. The following information is given for the Processing Department for August. Tl uses process costing. WIP Inventory Processing Department: August 1 Quantity (60% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 1 Current production and costs (August) Units started Current costs Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total current cost: August WIP Inventory Processing Department (August 31). Quantity (20% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 31 Required: 30,000 units $ 38,850 13,692 $ 52,542 77,000 units $ 88,900 57,100 $ 146,000 15,000 units ?? ?? ?? a. Complete the production cost report for August using the weighted-average method.…arrow_forward

- Terminal Industries (TI) produces a product using three departments: Mixing, Processing, and Filtering. New material is added only in the Mixing Department. The following information is given for the Processing Department for August. TI uses process costing. WIP Inventory Processing Department: August 1 Quantity (60% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 1 Current production and costs (August) Units started Current costs Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total current cost: August WIP Inventory Processing Department (August 31) Quantity (20 % complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 31 Flow of units: Units to be accounted for: Beginning WIP inventory Units started this period Total units to account for Units accounted for: Completed and transferred out Units in ending…arrow_forwardTerminal Industries (Tl) produces a product using three departments: Mixing. Processing, and Filtering. New material is added only the Mixing Department. The following information is given for the Processing Department for August. Tl uses process costing. WIP Inventory Processing Department: August 1 Quantity (60% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 1 Current production and costs (August) Units started Current costs Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total current cost: August WIP Inventory Processing Department (August 31) Quantity (20% complete) Transferred-in costs (from Mixing Department) Conversion costs (Processing Department) Total WIP cost: August 31 Flow of units: Units to be accounted for: Beginning WIP inventory Units started this period Total units to account for Units accounted for: Completed and transferred out Units in ending inventory…arrow_forwardVictory Company uses weighted average process costing. The company has two production processes. Conversion cost is added evenly throughout each process. Direct materials are added at the beginning of the first process. Additional information for the first process follows. Beginning work in process inventory Units started this period Total units Units completed and transferred out Ending work in process inventory Beginning work in process inventory Direct materials Conversion Costs added this period Direct materials Conversion Total costs to account for Units Units 79,000 894,000 795,000 178,000 $ 632,450 180, 360 Percent Complete 4,232,550 3,426,840 Direct Materials Percent Complete 100% 100% Required: 1. Compute equivalent units of production for both direct materials and conversion. Conversion Percent Complete 80% $ 812,810 Equivalent Units of Production (EUP) - Weighted Average Method Direct Materials EUP 7,659,390 $ 8,472,200 60% Percent Complete Conversion EUParrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College