Videos

Enterprise Fund Entries and Statements

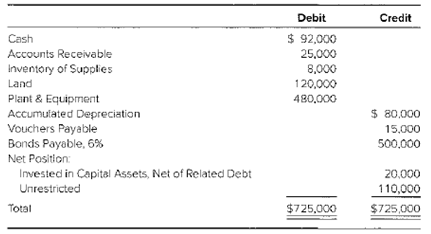

Augusta has a municipal water and gas utility district (MUD). The trail balance on January 1, 20X1, follows:

Additional Information for 20X1

- Charges to customers for water and gas were $420,000; collections were $432,000.

- A loan of $30,000 for two years was received from the general fund.

- The water and gas lines extended to a new development at a cost of $75,000. The contractor was paid.

- Supplies were acquired from central stores (internal service fund) for $12,400. Operating expenses were $328,000, and interest expense was $30,000. Payment was made for the interest and the payable to central stores, and $325,000 of the vouchers were paid.

Adjusting entries were as follows: estimated uncollectible accounts receivable, $6,300;depreciation expense, $32,000; and supplies expense, $15,200.

Required

- Prepare entries for the MUD enterprise fund for 20X1 and closing entries.

- Prepare a statement of net position for the fund for December 31, 20X1.

- Prepare a statement of revenues, expenses, and changes in fund net position for 20X1. Assume that the $500,000 of the 6 percent bonds is related to the net capital assets of land and of plant and equipment.

- Prepare a statement of

cash flows for 20X1.

a

Introduction: An enterprise fund is one of two proprietary funds. It is the amounts charged to the general public, to recover all or most of the cost of goods and services provided by the government to the general public. An enterprise fund is one of two proprietary funds.

The entries for the enterprise fund for 20X1 and closing entries.

Explanation of Solution

| Particulars | Debit $ | Credit $ |

| 1. Accounts receivable | 420,000 | |

| Revenue | 420,000 | |

| (Recognition of receivable from customers) | ||

| 2. Cash | 432,000 | |

| Accounts receivable | 432,000 | |

| (Received cash on account of accounts receivable) | ||

| Cash | 30,000 | |

| Due to general fund | 30,000 | |

| (Received loan from general fund) | ||

| 3. Plant and equipment | 75,000 | |

| Contracts payable | 75,000 | |

| (Extension of water and gas lines recognized) | ||

| Contract payable | 75,000 | |

| Cash | 75,000 | |

| (Record payment of extended lines) | ||

| 4. Inventory of supplies | 12,400 | |

| Operating expenses | 328,000 | |

| Interest expense | 30,000 | |

| Due to central stores fund | 12,400 | |

| Vouchers payable | 328,000 | |

| Interest payable | 30,000 | |

| (Expenses incurred are recognized) | ||

| Due to central stores fund | 12,400 | |

| Vouchers payable | 325,000 | |

| Interest payable | 30,000 | |

| Cash | 367,400 | |

| (Paid cash for dues to central fund vouchers and interest) | ||

| 5. Revenue | 6,300 | |

| Allowance for uncollectible | 6,300 | |

| (Reduction of revenue for uncollectible accounts) | ||

| Depreciation expense | 32,000 | |

| Accumulated depreciation | 32,000 | |

| (Adjustment for depreciation for the period) | ||

| Supplies expense | 15,200 | |

| Inventory of supplies | 15,200 | |

| (Adjustment for supplies on hand) | ||

| Closing entries: | ||

| Revenue | 413,700 | |

| Operating expenses | 328,000 | |

| Interest expense | 30,000 | |

| Depreciation expense | 32,000 | |

| Supplies expense | 15,200 | |

| Profit and loss summary | 8,500 | |

| (Closing of nominal accounts) | ||

| Profit and loss summary | 8,500 | |

| Net assets − unrestricted | 8,500 | |

| (Profit and loss summary account closed and amount transferred to net assets unrestricted) | ||

| Net Assets − unrestricted | 43,000 | |

| Net assets − invested in capital | 43,000 | |

| (Recognition of increase in net asset invested) |

Calculation of increase in net assets invested:

| Ending balance of net capital assets | $563,000 |

| Less: Related debt | (500,000) |

| Beginning balance in net assets − invested in capital assets | (20,000) |

| Increase in net assets invested | $43,000 |

b

Introduction: An enterprise fund is one of two proprietary funds. It is the amounts charged to the general public, to recover all or most of the cost of goods and services provided by the government to the general public. An enterprise fund is one of two proprietary funds.

The statement of net position for the fund for December 31, 20X1.

Answer to Problem 18.8E

Total assets as per statement of net assets $686,500

Explanation of Solution

A MUD Enterprise Fund

Statement of Net Assets

December 31, 20X1

| $ | $ | |

| Assets: | ||

| Cash | 111,600 | |

| Accounts receivable | 13,000 | |

| Less: Allowance for uncollectible | (6,300) | 6,700 |

| Inventory of supplies | 5,200 | |

| Land | 120,000 | |

| Plant and equipment | 555,000 | |

| Less: Accumulated depreciation | (112,000) | 443,000 |

| Total Assets | 686,500 | |

| Liabilities: | ||

| Vouchers payable | 18,000 | |

| Due to general fund | 30,000 | |

| Bonds payable | 500,000 | |

| Total Liabilities | 548,000 | |

| Net Assets: | ||

| Invested in capital assets, net of related debt | 63,000 | |

| Unrestricted | 75,500 | |

| Total Net Assets | 138,500 | |

| 686,500 |

c

Introduction: An enterprise fund is one of two proprietary funds. It is the amounts charged to the general public, to recover all or most of the cost of goods and services provided by the government to the general public. An enterprise fund is one of two proprietary funds.

The statement of revenues, expenses and changes in fund net position for 20X1. Assuming $500,000 of the 6 percent bonds is related to the net capital assets of land and of plant and equipment.

Answer to Problem 18.8E

Change in net assets $8,500

Explanation of Solution

A MUD Enterprise fund

Statement of Revenues, Expenses and

Changes in Fund Net Assets

For the year ended December 31, 20X1

| $ | $ | |

| Revenues: | ||

| Revenue from services | 413,700 | |

| Expenses: | ||

| Operating expense | 328,000 | |

| Depreciation | 32,000 | |

| Supplies | 15,200 | |

| Total expenses | 375,200 | |

| Operating income | 38,500 | |

| Non-operating expenses | ||

| Interest on capital − related debt | 30,000 | |

| Change in net assets | 8,500 | |

| Net assets, January 1 | 130,000 | |

| Net assets, December 31 | 138,500 |

d

Introduction: An enterprise fund is one of two proprietary funds. It is the amounts charged to the general public, to recover all or most of the cost of goods and services provided by the government to the general public. An enterprise fund is one of two proprietary funds.

The statement of cash flows 20X1.

Answer to Problem 18.8E

Net increase in cash $19,600

Explanation of Solution

A MUD Enterprise Fund

Statement of Cash Flows

December 31, 20X1

| $ | $ | |

| Cash flows from operating activities: | ||

| Cash received from customers | 432,000 | |

| Cash payments for goods and services | (325,000) | |

| Cash paid to internal service fund for supplies | (12,400) | |

| Net cash provided by operating activities | 94,600 | |

| Cash flows from non-capital financing activities: | ||

| Cash received from general fund for non-capital loan | 30,000 | |

| Net cash provided by non-capital financing activities | 30,000 | |

| Cash flow from capital and related financing activities | ||

| Interest on capital related debts | (30,000) | |

| Extension of service lines | (75,000) | |

| Net cash used for capital and related financing activities | (105,000) | |

| Cash flow from investing activities | 0 | |

| Net increase in cash | 19,600 | |

| Cash at the beginning of the year | 92,000 | |

| Cash at the end of the year | 111,600 |

Want to see more full solutions like this?

Chapter 18 Solutions

ADVANCED FINANCIAL ACCOUNTING-ACCESS

Additional Business Textbook Solutions

Financial Accounting: Tools for Business Decision Making, 8th Edition

Financial Accounting, Student Value Edition (4th Edition)

Introduction To Managerial Accounting

Intermediate Accounting

Financial Accounting, Student Value Edition (5th Edition)

- This year Riverside began work on an outdoor amphitheater and concession stand at the city's park. It is to be financed by a $3,500,000 bond issue and supplemented by a $500,000 General Fund transfer. The following transactions occurred during the current year: 1.The General Fund transferred $500,000 to the Park Building Capital Projects Fund (hint: credit "Other Financing Sources-Interfund Transfers In" for $500,000). 2.A contract was signed with Restin Construction Company for the major part of the project on a bid of $2,700,000. 3.Preliminary planning and engineering costs of $69,000 were vouchered for e Great Pacific Engineering Company. (This cost had not been encumbered, therefore, we do not need the reverse journal entries for encumbrances, but we need to record expenditures and liability for this cost in the capital projects fund.) 4.An invoice in the amount of $1,000,000 was received from Restin for progress to date on the project. 5.The $3,500,000 bonds were issued at par.…arrow_forwardA city is building a new park. To finance the construction of the park, the city will issue a $1,800,000 bond, and receive a transfer of $200,000 from the general Please record the journal entries for the Capital Project Fund and the Government-Wide financial statements. 1. The city signed a contract with a construction company to construct the park for $2,000.000. 2. The $1.800.000 bonds were issued at par. 3. The construction company billed the city for $2,000,000 upon completion of the project. 4. The park is completed.arrow_forwardThe governing board of wolekete town approved a street improvement program excepted to cost birr 500,000 and authorized a birr 300,000 bond issue to partially finance the improvement the reaming sources needed are to be provided by a federal grant and an internal fund transfer. Capital projects fund accounting records were established and the plane and authorizes recorded in by memorandum entry. The following transactions took place in connection with this project. 1.proceeds of the bond sale bitt 303000 were recoreded in capital project found etcarrow_forward

- Prepare journal entries for a local government to record the following transactions, first for fund financial statements and then for government-wide financial statements. The government sells $900,000 in bonds at face value to finance construction of a warehouse. A $1.1 million contract is signed for construction of the warehouse. The commitment is required, if allowed. A $130,000 transfer of unrestricted funds was made for the eventual payment of the debt in (a). Equipment for the fire department is received with a cost of $12,000. When it was ordered, an anticipated cost of $11,800 had been recorded. Supplies to be used in the schools are bought for $2,000 cash. The consumption method is used. A state grant of $90,000 is awarded to supplement police salaries. The money will be paid to reimburse the government after the supplement payments have been made to the police officers. Property tax assessments are mailed to citizens of the government. The total assessment is $600,000,…arrow_forwardPrepare journal entries for a local government to record the following transactions, first for fund financial statements and then for government-wide financial statements.a. The government sells $900,000 in bonds at face value to finance construction of a warehouse.b. A $1.1 million contract is signed for construction of the warehouse. The commitment is required, if allowed.c. A $130,000 transfer of unrestricted funds was made for the eventual payment of the debt in (a).d. Equipment for the fire department is received with a cost of $12,000. When it was ordered, an anticipated cost of $11,800 had been recorded.e. Supplies to be used in the schools are bought for $2,000 cash. The consumption method is used.f. A state grant of $90,000 is awarded to supplement police salaries. The money will be paid to reimburse the government after the supplement payments have been made to the police officers.g. Property tax assessments are mailed to citizens of the government. The total assessment is…arrow_forwardThe Township of Thomasville's General Fund has the following net resources at year end: • $66,000 of inventory • $375,000 federal grants for disaster relieve related to the flood • $60,000 sinking fund for payments of general obligation bond • $150,000 contractual obligations for the purchase of equipment • $200,000 to be used to fund government operations in the future • Outstanding encumbrance of $80,000 for the purchase of office supplies 1. What would be the total Nonspendable fund balance? 2. What would be the total Restricted fund balance? 3. What would be the total Committed fund balance? 4. What would be the total Assigned fund balance? 5. What would be the total Unassigned fund balance?arrow_forward

- Prepare journal entries for the City of Pudding’s governmental funds to record the following transactions, first for fund financial statements and then for government-wide financial statements.a. A new truck for the sanitation department was ordered at a cost of $94,000.b. The city print shop did $1,200 worth of work for the school system (but has not yet been paid).c. An $11 million bond was issued to build a new road.d. Cash of $140,000 is transferred from the general fund to provide permanent financing for a municipal swimming pool that will be viewed as an enterprise fund.e. The truck ordered in (a) is received at an actual cost of $96,000. Payment is not made at this time.f. Cash of $32,000 is transferred from the general fund to the capital projects fund.g. A state grant of $30,000 is received that must be spent to promote recycling.h. The first $5,000 of the state grant received in (g) is appropriately expended.arrow_forwardThe City of Soheil maintains its books so as to prepare fund accounting statements and prepares worksheet adjustments in order to prepare government-wide financial statements. Required: You are to prepare, in journal form, worksheet adjustments for each of the following situations. General fixed assets, as of the beginning of the year, which had not been recorded, were as follows: Land $ 96,000,000 Buildings 480,000,000 Improvements other than buildings 270,000,000 Equipment 60,000,000 Accumulated depreciation, capital assets 150,000,000 During the year, expenditures for capital outlays amounted to $22,700,000. Of that amount, $10,600,000 was for buildings; $8,300,000 was for improvements other than buildings, $95,000 was capitalized interest and the remainder was for land. The capital outlay expenditures outlined in (B) were completed at the end of the year (no depreciation until next year). For purposes of financial statement…arrow_forwardThe City of Sunnyville’s General Fund has the following net resources at year end: $55,000 for LT Advance to an internal service fund $375,000 approved by the City Council with specific conditions for its use $2,500 of supplies inventory $60,000 state grant for snow removal $150,000 City Council resolution approved for funds to renovate city hall $400,000 to be used to fund government operations in the future Outstanding encumbrances of $80,000 for the purchase of furniture & fixtures What would be the total “Restricted” Fund balance? Select one: a. $275,000 b. $210,000 c. $150,000 d. $60,000arrow_forward

- The City of Sunnyville’s General Fund has the following net resources at year end: $55,000 for LT Advance to an internal service fund $375,000 approved by the City Council with specific conditions for its use $2,500 of supplies inventory $60,000 state grant for snow removal $150,000 City Council resolution approved for funds to renovate city hall $400,000 to be used to fund government operations in the future Outstanding encumbrances of $80,000 for the purchase of furniture & fixtures What would be the total “Committed” fund balance? Select one: a. $375,000 b. $290,000 c. $525,000 d. $455,000arrow_forwardFinancing for the renovation of Fir City's municipal park, begun and completed during Year 1, came from the following sources: Grant from state government $400,000 Proceeds from general obligation bond issue 500,000 Transfer from Fir's general fund 100,000 In its Year 1 capital projects fund operating statement, Fir should report these amounts as:) Revenues Other Financing Sources A) Operating cash flow only. B) Investing cash flow only C) Operating or investing cash flow. D) Operating or financing cash flow.arrow_forwardRecord the appropriate journal entry using encumbrance accounting: 1. Federal grant of $30,000 was received. 2. By the end of the fiscal year, the city earned 80% of the federal grant. The remainder will be earned in the next fiscal yeararrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education