Concept explainers

Videos

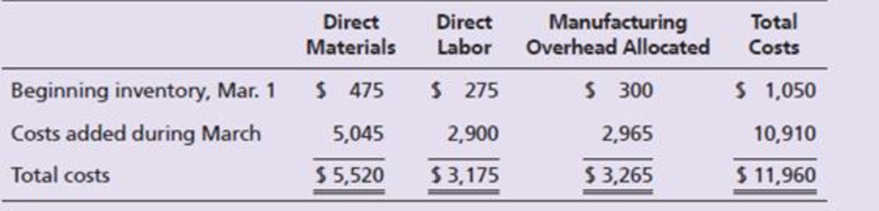

Smith Paper Co. produces the paper used by wallpaper manufacturers. Smith’s four-stage process includes mixing, cooking, rolling, and cutting. On March 1, the Mixing Department had 400 rolls in process. During March, the Mixing Department completed the mixing process for those 400 rolls and also started and completed the mixing process for an additional 4,100 rolls of paper. The department started but did not finish the mixing process for an additional 500 rolls, which were 20% complete with respect to both direct materials and conversion work at the end of March. Direct materials and conversion costs are incurred evenly throughout the mixing process. The Mixing Department compiled the following data for March:

Requirements

- 1. Prepare a production cost report for the Mixing Department for March. The company uses the weighted-average method.

- 2. Journalize all transactions affecting the company’s mixing process during March. Assume labor costs are accrued and not yet paid.

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Additional Business Textbook Solutions

Financial Accounting: Tools for Business Decision Making, 8th Edition

Intermediate Accounting

PRINCIPLES OF TAXATION F/BUS.+INVEST.

Auditing And Assurance Services

Advanced Financial Accounting

Principles of Accounting Volume 1

- Kraus Steel Company has two departments, Casting and Rolling. In the Rolling Department, ingots From the Casting Department are rolled into steel sheet. The Rolling Department received 4,000 tons from the Casting Department in October. During October, the Rolling Department completed 3,900 tons, including 200 tons of work in process on October 1. The ending work in process inventory on October 31 was 300 tons. How many tons were started and completed during October?arrow_forwardPetrini Products Co. has two departments: Mixing and Cooking. At the beginning of the month, Cooking had 4,000 units in process with costs of 8,600 from Mixing, and its own departmental costs of 500 for materials, 1,000 for labor, and 2,500 for factory overhead. During the month, 10,000 units were received from Mixing with a cost of 25,000. Cooking incurred costs of 4,250 for materials, 8,500 for labor, and 21,250 for factory overhead, and finished 12,000 units. At the end of the month, there were 2,000 units in process, one-half completed. Required: 1. Determine the unit cost for the month in Cooking. 2. Determine the adjusted weighted average unit cost for all units received from Mixing. 3. Determine the unit cost of goods finished. 4. Determine the accumulated cost of the goods finished and of the ending work in process. (Round unit costs to three decimal places.)arrow_forwardDuring December, Krause Chemical Company had the following selected data concerning the manufacture of Xyzine, an industrial cleaner: All materials are added at the beginning of processing in this department, and conversion costs are added uniformly during the process. The beginning work in process inventory had 120 of raw materials and 180 of conversion costs incurred. Materials added during December were 540, and conversion costs of 1,484 were incurred. Krause uses the first-in, first-out (FIFO) process cost method. The equivalent units of production used to compute conversion costs for December were: a. 110 units. b. 104 units. c. 100 units. d. 92 units.arrow_forward

- Chavez Concrete Inc. has two production departments. Blending had 1,000 units in process at the beginning of the period, two-fifths complete. During the period 7,800 units were received from Mixing, 8,200 units were transferred to the finished goods storeroom, and 600 units were in process at the end of the period, 1/3 complete. The cost of the beginning work in process was: The costs during the month were: 1. Using the data in E5-15, prepare a cost of production summary for the month ended January 31, 2016. 2. Prepare a journal entry to transfer the cost of the completed units from Blending to the finished goods storeroom.arrow_forwardGolding Manufacturing, a division of Farnsworth Sporting, Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handle. The limbs pass through four sequential processes before reaching final assembly: lay-up, molding, fabricating, and finishing. In the Lay-Up Department, limbs are created by laminating layers of wood. In Molding, the limbs are heat treated, under pressure, to form a strong resilient limb. In the Fabricating Department, any protruding glue or other processing residue is removed. Finally, in Finishing, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the Pattern Department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the Finishing Department where they are sprayed with the final finishes. In Final Assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80 percent of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: KAREN: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in direct material input. AARON: Your predecessor is responsible. He believed that tracking the difference in direct material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. KAREN: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the Pattern Department. The other departments fit what I view as a process-costing pattern. AARON: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the Pattern Department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no beginning work in process; however, there were 300 units in ending work in process: 200 Deluxe and 100 Econo models. Both models were 80 percent complete with respect to conversion costs and 100 percent complete with respect to direct materials. c. The Pattern Department experienced the following costs: d. On an experimental basis, the requisition forms for direct materials were modified to identify the dollar value of the direct materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the Pattern Department, assuming that process costing is totally appropriate. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price less manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?arrow_forwardHeap Company manufactures a product that passes through two processes: Fabrication and Assembly. The following information was obtained for the Fabrication Department for September: a. All materials are added at the beginning of the process. b. Beginning work in process had 80,000 units, 30 percent complete with respect to conversion costs. c. Ending work in process had 17,000 units, 25 percent complete with respect to conversion costs. d. Started in process, 95,000 units. Required: 1. Prepare a physical flow schedule. 2. Compute equivalent units using the weighted average method. 3. Compute equivalent units using the FIFO method.arrow_forward

- Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules. During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments): Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor. Required: 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places. 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.arrow_forwardGolding Manufacturing, a division of Farnsworth Sporting Inc., produces two different models of bows and eight models of knives. The bow-manufacturing process involves the production of two major subassemblies: the limbs and the handles. The limbs pass through four sequential processes before reaching final assembly: layup, molding, fabricating, and finishing. In the layup department, limbs are created by laminating layers of wood. In the molding department, the limbs are heat-treated, under pressure, to form strong resilient limbs. In the fabricating department, any protruding glue or other processing residue is removed. Finally, in the finishing department, the limbs are cleaned with acetone, dried, and sprayed with the final finishes. The handles pass through two processes before reaching final assembly: pattern and finishing. In the pattern department, blocks of wood are fed into a machine that is set to shape the handles. Different patterns are possible, depending on the machines setting. After coming out of the machine, the handles are cleaned and smoothed. They then pass to the finishing department, where they are sprayed with the final finishes. In final assembly, the limbs and handles are assembled into different models using purchased parts such as pulley assemblies, weight-adjustment bolts, side plates, and string. Golding, since its inception, has been using process costing to assign product costs. A predetermined overhead rate is used based on direct labor dollars (80% of direct labor dollars). Recently, Golding has hired a new controller, Karen Jenkins. After reviewing the product-costing procedures, Karen requested a meeting with the divisional manager, Aaron Suhr. The following is a transcript of their conversation: Karen: Aaron, I have some concerns about our cost accounting system. We make two different models of bows and are treating them as if they were the same product. Now I know that the only real difference between the models is the handle. The processing of the handles is the same, but the handles differ significantly in the amount and quality of wood used. Our current costing does not reflect this difference in material input. Aaron: Your predecessor is responsible. He believed that tracking the difference in material cost wasnt worth the effort. He simply didnt believe that it would make much difference in the unit cost of either model. Karen: Well, he may have been right, but I have my doubts. If there is a significant difference, it could affect our views of which model is more important to the company. The additional bookkeeping isnt very stringent. All we have to worry about is the pattern department. The other departments fit what I view as a process-costing pattern. Aaron: Why dont you look into it? If there is a significant difference, go ahead and adjust the costing system. After the meeting, Karen decided to collect cost data on the two models: the Deluxe model and the Econo model. She decided to track the costs for one week. At the end of the week, she had collected the following data from the pattern department: a. There were a total of 2,500 bows completed: 1,000 Deluxe models and 1,500 Econo models. b. There was no BWIP; however, there were 300 units in EWIP: 200 Deluxe and 100 Econo models. Both models were 80% complete with respect to conversion costs and 100% complete with respect to materials. c. The pattern department experienced the following costs: d. On an experimental basis, the requisition forms for materials were modified to identify the dollar value of the materials used by the Econo and Deluxe models: Required: 1. Compute the unit cost for the handles produced by the pattern department, assuming that process costing is totally appropriate. Round unit cost to two decimal places. 2. Compute the unit cost of each handle, using the separate cost information provided on materials. Round unit cost to two decimal places. 3. Compare the unit costs computed in Requirements 1 and 2. Is Karen justified in her belief that a pure process-costing relationship is not appropriate? Describe the costing system that you would recommend. 4. In the past, the marketing manager has requested more money for advertising the Econo line. Aaron has repeatedly refused to grant any increase in this products advertising budget because its per-unit profit (selling price minus manufacturing cost) is so low. Given the results in Requirements 1 through 3, was Aaron justified in his position?arrow_forwardLarkin Company produces leather strips for western belts using three processes: cutting, design and coloring, and punching. The weighted average method is used for all three departments. The following information pertains to the Design and Coloring Department for the month of June: a. There was no beginning work in process. b. There were 400,000 units transferred in from the Cutting Department. c. Ending work in process, June 30: 50,000 strips, 80 percent complete with respect to conversion costs. d. Units completed and transferred out: 330,000 strips. The following costs were added during the month: a. Direct materials are added at the beginning of the process. b. Inspection takes place at the end of the process. All spoilage is considered normal. Required: 1. Calculate equivalent units of production for transferred-in materials, direct materials added, and conversion costs. 2. Calculate unit costs for the three categories of Requirement 1. 3. What is the total cost of units transferred out? What is the cost of ending work-in-process inventory? How is the cost of spoilage treated? 4. Assume that all spoilage is considered abnormal. Now, how is spoilage treated? Give the journal entry to account for the cost of the spoiled units. Some companies view all spoilage as abnormal. Explain why. 5. Assume that 80 percent of the units spoiled are abnormal and 20 percent are normal spoilage. Show the spoilage treatment for this scenario.arrow_forward

- Eyring Manufacturing produces a component used in its production of washing machines. The time to set up and produce a batch of the components is two days. The average daily usage is 800 components, and the maximum daily usage is 875 components. Required: Compute the reorder point assuming that safety stock is carried by Eyring Manufacturing. How much safety stock is carried by Eyring?arrow_forwardMenlo Materials is divided into five departments, Mixing, Blending, Finishing, Factory Office, and Building Maintenance. The first three departments are engaged in production work. Factory Office and Building Maintenance are service departments. During the month of June, the following factory overhead was incurred for the departments: The bases for distributing service department expenses to the other departments follow: Building Maintenance—On the basis of floor space occupied by the other departments as follows: Mixing, 10,000 sq ft; Blending, 4,500 sq ft; Finishing, 10,500 sq ft; and Factory Office, 7,000 sq ft. Factory Office—On the basis of number of employees as follows: Mixing, 30; Blending, 20; and Finishing, 50. Required: Prepare a schedule showing the distribution of the service departments’ expenses using the direct distribution method.arrow_forwardUsing the same data found in Exercise 6.22, assume the company uses the FIFO method. Required: Prepare a schedule of equivalent units, and compute the unit cost for the month of December. Fordman Company has a product that passes through two processes: Grinding and Polishing. During December, the Grinding Department transferred 20,000 units to the Polishing Department. The cost of the units transferred into the second department was 40,000. Direct materials are added uniformly in the second process. Units are measured the same way in both departments. The second department (Polishing) had the following physical flow schedule for December: Costs in beginning work in process for the Polishing Department were direct materials, 5,000; conversion costs, 6,000; and transferred in, 8,000. Costs added during the month: direct materials, 32,000; conversion costs, 50,000; and transferred in, 40,000.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College