Concept explainers

Videos

Analyze Horsepower Hookup, Inc.

Horsepower Hookup, Inc., is a large automobile company that specializes in the production of high-powered trucks. The company is determining cost allocations for purposes of performance evaluation. A portion of company bonuses depends on divisions achieving cost management goals. This necessitates highly accurate support department cost allocation. Management has also stated that it has the means to implement as complex a method as necessary.

The general manager over the Mid-Size D wants to get a good idea of what factors are driving the costs of the support departments in order to make accurate cost allocations, so finding accurate support department cost drivers is important. Support department costs include Janitorial ($163,100) and Security ($285,400). The Janitorial costs vary depending on the number of vehicles produced, increasing with larger production volumes. Security costs are fixed based on the size of the lot, and do not change with respect to how many vehicles are in the lot or warehouse. Joint costs involved in producing the trucks before the split-off point where the various makes, models, and colors are produced are $946,000 for the period. All makes, models, and colors sell at relatively similar margins, but the sports models and metallic colors are normally more difficult to produce during the joint production process.

- a. Which support department cost allocation method (direct, sequential, or reciprocal services) should be used to allocate support department cost?

- b. What driver would be best for allocating Janitorial costs?

- c. What driver would be best for allocating Security costs?

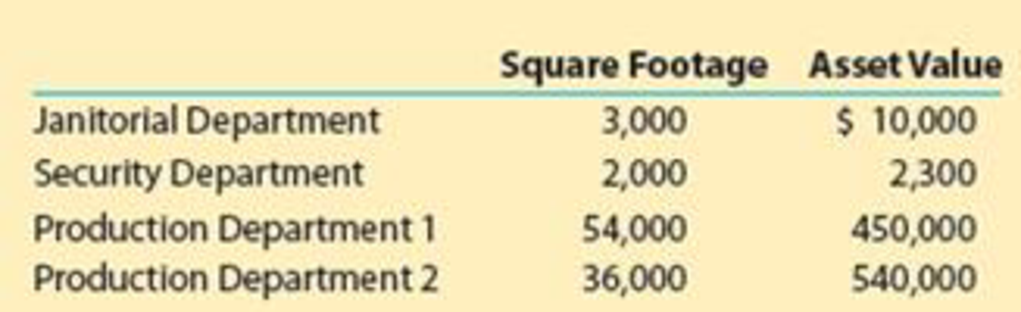

- d. If Janitorial costs were to be allocated based on square footage, and Security costs based on asset value, what percentage of each support department’s costs would be allocated to each production department using the sequential method (allocating Security costs first) given the following:

- e. Should Janitorial and Security costs be considered when evaluating the performance of cost management employees?

- f. What joint cost allocation method should be used for performance evaluation purposes?

Trending nowThis is a popular solution!

Chapter 19 Solutions

Financial and Managerial Accounting - CengageNow

- Two departments within Cougar Gear Inc. are Production and Sales. Each department has a unique scorecard, as follows: The Production Department scorecard focuses on the learning and growth and internal processes perspectives. The Sales Department scorecard focuses on the learning and growth and customer perspectives. Both scorecards have the learning and growth performance metrics of median training hours per employee and average employee tenure. The Production scorecard has the unique metrics of production time per unit and number of production shutdowns. The Sales scorecard has the unique metrics of percentage of customers who shop again and online customer satisfaction rating. The performance targets for each metric are shown in the tan boxes just under the performance metrics. The actual achieved metrics are shown in the red boxes just below the tan boxes. When evaluating both departments, Cougar Gears management looks at the median training hours per employee and average employee tenure metrics and subsequently decides to give the Sales Department a large bonus while giving the Production Department a minimal bonus. a. Determine and define the type of cognitive bias Cougar Gears management has exhibited in this instance. b. Determine which department would have received the larger bonus had the companys management not been biased in the evaluation. c. Discuss one advantage and one disadvantage of using unique balanced scorecards for different departments or divisions of a company.arrow_forwardJolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?arrow_forwardRacxel PLC is a multi-divisional organisation manufacturing four different product lines. The directors of Racxel are worried about its costing and performance management systems which are based around absorption costing and financial ratio analysis. Required:Draft a briefing note to the Directors of Racxel that discusses: a.The benefits of replacing absorption costing with activity-based costing b.The weaknesses associated with traditional, financially focused performance measurement systems like ratio analysis c.The benefits of using the economic value added (EVA) systemarrow_forward

- Profit Corp. has a subunit classified as a cost center that supports other parts of the firm but has reported costs higher than what the corporate office would like to see. Thus, the manager of this subunit is under pressure to cut operating costs without hurting the perceived quality of services provided. What general recommendations could you give to the manager of this cost center to achieve that goal?arrow_forwardWaterfield Company is looking for a way to help its executive managers assess how its three divisions are meeting the company’s goals and objectives for the performance of its purchasing department. Which of the following metrics might be used for this purpose? a. customer satisfaction rating b. the material price variance c. the amount of time employees spend in training d. operating incomearrow_forwardRequired information [The following information applies to the questions displayed below.] Data Performance, a computer software consulting company, has three major functional areas: computer programming, information systems consulting, and software training. Carol Bingham, a pricing analyst, has been asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing these costs, Carol is considering three different methods of the departmental allocation approach to allocate overhead costs: the direct method, the step method, and the reciprocal method. She assembled the following data from the two service departments, information systems and facilities: a. b. Budgeted overhead (base) Information Systems (computer hours) Facilities (square feet) C. Service Departments Information Systems $ 368,000 240 Direct Method Step Method (Information Systems Goes First) Step Method (Facilities Goes First) Reciprocal method Computer…arrow_forward

- Data Performance, a computer software consulting company, has three major functional areas: computer programming, information systems consulting, and software training. Carol Bingham, a pricing analyst, has been asked to develop total costs for the functional areas. These costs will be used as a guide in pricing a new contract. In computing these costs, Carol is considering three different methods of the departmental allocation approach to allocate overhead costs: the direct method, the step method, and the reciprocal method. She assembled the following data from the two service departments, information systems and facilities: Service Departments Production Departments Information Systems Facilities Computer Programming Information Systems Consulting Software Training Total Budgeted overhead (base) $ 368,000 $ 184,000 $ 736,000 $ 874,000 $ 575,000 $ 2,737,000 Information Systems (computer hours) 600 1,200 300 900 3,000 Facilities (square feet) 240 960 600 600…arrow_forwardYou are the new cost accountant for ABX Corporation. After careful review of the company’s operations you have been tasked to determine the company’s break-even point in units and dollars, the numbers sold to meet the company’s target profit and contribution income statement for both outcomes.Management has also asked that you discuss the risk, uncertainty, changing variables and margin of safety regarding Cost Volume Profit Analysis. Based on your discussion and calculations what would be your recommendation if the company wanted to increase variable cost by 20% and sales price by 5%? Support your recommendation. ABX Corporation sold it's product for $600/unit. Fixed cost are $725,000 per year. Variable costs are $455 per unit. ABX Corporation desires a target profit of $1,250,000 per year.arrow_forwardJanex PLC is a multi-divisional organisation manufacturing four different product lines. The directors of Janex are worried about its costing and performance management systems which are based around absorption costing and financial ratio analysis. Required: Draft a briefing note to the Directors of Janex that discusses: The benefits of replacing absorption costing with activity-based costing The weaknesses associated with traditional, financially focused performance measurement systems like ratio analysis The benefits of using the economic value added (EVA) systemarrow_forward

- Determine the total costs that each operating segment would be accountable for if the step method is used to allocate support costs; assume support departments are ranked according to their original cost. (Round intermediate calculations to 4 decimal places, e.g. 15.2516 and final answers to 2 decimal places, e.g. 15.25.) Total costs $ Operating Segments Institutional Taythank and Media. 776887.5 Retail 468712.5arrow_forwardYou are the new cost accountant for ABX Corporation. After careful review of the company's operation you have been tasked to determine the company's break-even point in units and dollars, the numbers sold to meet the company's target profit and contribution income statement for both outcomes. Management has also asked that you discuss the risk, uncertainty, changing variables and margin of safety regarding Cost Volume Profit Analysis. Based on your discussion and calculations what would be your recommendation if the company wanted to increase variable cost by 20% and sales price by 5%? Support your recommendation. Company's Data: ABX Corporation sold it's production for %600/unit. Fixed cost are $725,000 per year. Variable costs are $455 per unit. ABX Corporation desires a target profit of $1,250,000 per year.arrow_forwardPlain Limited produces two standard products, White and Grey. You have recently been appointed as a management accountant along with a new marketing manager, who has several ideas about how to grow the company, including introducing new products with different designs. The company currently absorbs overheads on the basis of units produced, but they have read about a method based on activities undertaken, Activity Based Costing. They have asked you to help them to investigate this method and it’s implication for their business should they decide to implement it in the next accounting year. The current expected output for the existing products during the next year is White 15,000 and Grey 12,000 The company has also provided the following information about the current overhead costs of the business; Overhead activity. Annual costs Cost driver. Amount of activity White…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning