Concept explainers

Videos

Plantwide versus Multiple Predetermined

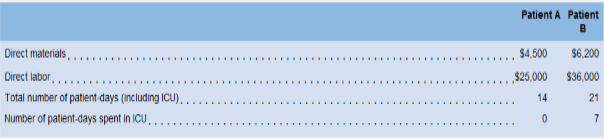

Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spendsin the hospital counts as one patient-day) to allocate overhead costs to patients, Recently a member of the hospital’s accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy of the costsallocated to patients. The first overhead rate would include all overhead costs within the Intensive Care Unit (ICU) and the second overheadrate would include all other overhead costs. Information pertaining to the hospital’s estimated number of patient-days, its estimated overheadcosts, and two of its patients—Patient A and Patient B—is provided below:

Required:

Assuming McCullough uses only one predetermined overhead rate, calculate:

a. The predetermined overhead rate.

b. The total cost, including direct materials, direct labor and applied overhead, assigned to Patient A and Patient B.

2. Assuming McCullough calculates two overhead rates as recommended by the staff accountant calculate:

a. The ICU and Other overhead rates.

b. The total cost, including direct materials, direct labor and applied overhead, assigned to Patient A and Patient B.

3. What insights are revealed by the staff accountant’s approach?

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

Loose Leaf For Introduction To Managerial Accounting

- Product costing and decision analysis for a service company Pleasant Stay Medical Inc. wishes to determine its product costs. Pleasant Stay offers a variety of medical procedures (operations) that are considered its products. The overhead has been separated into three major activities. The annual estimated activity costs and activity bases follow: Total patient days are determined by multiplying the number of patients by the average length of stay in the hospital. A weighted care unit (wcu) is a measure of nursing effort used to care for patients. There were 192,000 weighted care units estimated for the year. In addition, Pleasant Stay estimated 6,000 patients and 27,000 patient days for the year. (The average patient is expected to have a a little more than a four-day stay in the hospital.) During a portion of the year, Pleasant Stay collected patient information for three selected procedures, as follows: Private insurance reimburses the hospital for these activities at a fixed daily rate of 406 per patient day for all three procedures. Instructions Determine the activity rates. Determine the activity cost for each procedure. Determine the excess or deficiency of reimbursements to activity cost. Interpret your results.arrow_forwardMcCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the- clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. Recently a member of the hospital's accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy…arrow_forwardMcCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the- clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. Recently a member of the hospital's accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy…arrow_forward

- McCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the-clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. Recently a member of the hospital’s accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the…arrow_forwardMcCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the-clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. For the most recent period, this predetermined rate was based on three estimates-fixed overhead costs of $17,960,000, variable overhead costs of $110 per patient-day, and a…arrow_forwardMcCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the- clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. Recently a member of the hospital's accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the accuracy…arrow_forward

- McCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. Recently a member of the hospital’s accounting staff has suggested using two predetermined overhead rates (allocated based on the number of patient-days) to improve the…arrow_forwardbk ht McCullough Hospital uses a job-order costing system to assign costs to its patients. Its direct materials include a variety of items such as pharmaceutical drugs, heart valves, artificial hips, and pacemakers. Its direct labor costs (e.g., surgeons, anesthesiologists, radiologists, and nurses) associated with specific surgical procedures and tests are traced to individual patients. All other costs, such as depreciation of medical equipment, insurance, utilities, incidental medical supplies, and the labor costs associated with around-the- clock monitoring of patients are treated as overhead costs. Historically, McCullough has used one predetermined overhead rate based on the number of patient-days (each night that a patient spends in the hospital counts as one patient-day) to allocate overhead costs to patients. For the most recent period, this predetermined rate was based on three estimates-fixed overhead costs of $17,960,000, variable overhead costs of $110 per patient- day, and…arrow_forwardA-7arrow_forward

- All applicable Problems are available with McGraw-Hill’s Connect™Accounting. Activity-based costing MedTech, Inc., manufactures and sells diagnostic equipment used in the medical profession. Its job costing system was designed using an activity-based costing approach. Direct materials and direct labor costs are accumulated separately, along with information concerning four manufacturing overhead cost drivers (activities). Assume that the direct labor rate is $25 per hour and thatthere were no beginning inventories. The following information was available for 2013, based on an expected production level of 100,000 units for the year:Activity Budgeted Cost Driver Used Cost(Cost Driver) Costs for 2013 as Allocation Base Allocation RateMaterials handling $1,200,000 Number of parts used $ 2.00 per partMilling and grinding 2,200,000 Number of machine hours 11.00 per hourAssembly and inspection 1,500,000 Direct labor hours worked 5.00 per hour Testing 300,000 Number of units tested 3.00 per…arrow_forwardActivity Costing, Assigning Resource Costs, Primary andSecondary ActivitiesElmo Clinic has identified three activities for daily maternity care: occupancy and feeding,nursing, and nursing supervision. The nursing supervisor oversees 150 nurses, 25 of whomare maternity nurses (the other nurses are located in other care areas such as the emergencyroom and intensive care). The nursing supervisor has three assistants, a secretary, severaloffices, computers, phones, and furniture. The three assistants spend 75% of their timeon the supervising activity and 25% of their time as surgical nurses. They each receive asalary of $60,000. The nursing supervisor has a salary of $80,000. She spends 100% of hertime supervising. The secretary receives a salary of $35,000 per year. Other costs directlytraceable to the supervisory activity (depreciation, utilities, phone, etc.) average $170,000per year.Daily care output is measured as “patient days.” The clinic has traditionally assigned the costof daily…arrow_forwardWhat types of overhead costs are considered in job costing for hospitals, and how are they allocated to patients or procedures?A. Facility Costs - Rent, property taxes, utilities B. Administrative Costs - Salaries of administrative staff, office supplies, software systems, and legal fees C. Medical supplies and Equipment - Overhead costs also cover the expenses incurred in maintaining and replenishing medical supplies, equipment, and instruments used throughout the hospital. Can you think of any other overhead costs that may be considered when a hospital is determining the cost of a procedure?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College