Videos

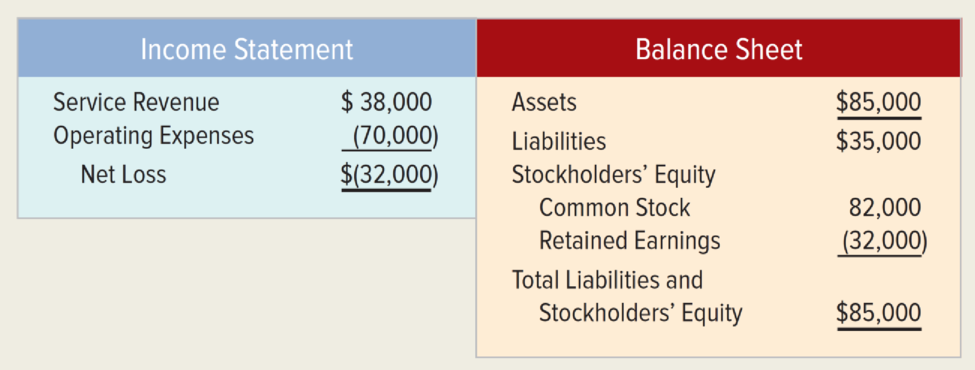

Glenn’s Cleaning Services Company is experiencing

Glenn made the following adjustments to these statements before showing them to his friend. He recorded $82,000 of revenue on account from Barrymore Manufacturing Company for a contract to clean its headquarters office building that was still being negotiated for the next month. Barrymore had scheduled a meeting to sign a contract the following week, so Glenn was sure that he would get the job. Barrymore was a reputable company, and Glenn was confident that he could ultimately collect the $82,000. Also, he subtracted $30,000 of accrued salaries expense and the corresponding liability. He reasoned that since he had not paid the employees, he had not incurred any expense.

Required

a. Reconstruct the income statement and balance sheet as they would appear after Glenn’s adjustments.

b. Write a brief memo explaining how Glenn’s treatment of the expected revenue from Barrymore violated the revenue recognition concept.

c. Write a brief memo explaining how Glenn’s treatment of the accrued salaries expense violates the matching concept.

Want to see the full answer?

Check out a sample textbook solution

Chapter 2 Solutions

Survey Of Accounting

- Comprehensive Problem 1 8 Net income. 31,425 Kelly Pitney began her consulting business. Kelly Consulting, on April 1, 20Y8. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter During May, Kelly Consulting entered into the following transactions: May 3.Received cash from clients as an advance payment for services to be provided and recorded it as unearned tree 4,500 5.Received cash from clients on account 2,450. 9.Paid cash for a newspaper advertisement 225. 13.Raid Office Station Co for part of the debt incurred on April , 640. 15.Recorded services provided on account for the period May 1-15, 9,180. 16 Paid part-time receptionist for two weeks salary including the amount owed on April 30, 750. 17.Recorded cash from cash clients for fees earned during the period May 116, 8,360. Record the following transactions on Page 6 of the Journal 20.Purchased support on account 735. 21.Recorded services provided on account for the period May 1620. 4,820 25.Recorded cash from cash clients for fees earned for the period May 1723, 7,900 27.Received cash from clients on account 9,520. 28.Paid part-time receptionist for two weeks salary. 7S0. 30.Raid telephone bill for May. 260 31.Paid electricity bill for May, 810. 31.Recorded cash from cash clients tor lees earned for the period May 2031. 3,300. 31.Recorded services provided on account for the remainder of May, 2,650. 31.Paid dividends 10,500 Instructions 1.The chart of accounts foe Kelly Consulting is shown us Exhibit 9. and the post-closing trial balance as of April 30, 20Y8, is shown in Exhibit 17. for each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1. 20Y8. and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting cm Page of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2.Post the journal to a ledger of four-column accounts. 5.Prepare an unadjusted trial balance. 4.At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). (a)Insurance expired during May is 275. (b)Supplies on hand on May II are 715. (c)Depreciation of office equipment for May is 330. (d)Accrued receptionist salary on May 31 is 325. (e)Rent expired during May is 1600. (f)Unearned fees on May 31 are 3,210 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of stockholders equity, and a balance sheet. 9.Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardJournal entries and trial balance Valley Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on July 31, 2018, follows: The following business transactions were completed by Valley Realty during August 2018: Aug. 1. Purchased office supplies on account, 3,150. 2. Paid rent on office for month, 7,200. 3. Received cash from clients on account, 83,900. 5. Paid insurance premiums, 12,000. 9. Returned a portion of the office supplies purchased on August 1, receiving full credit for their cost, 400. 17. Paid advertising expense, 8,000. 23. Paid creditors on account, 13,750. Enter the following transactions on Page 19 of the two-column journal: 29. Paid miscellaneous expenses, 1,700. 30. Paid automobile expense (including rental charges for an automobile), 2,500. 31. Discovered an error in computing a commission during July; received cash from the salesperson for the overpayment, 2,000. 31. Paid salaries and commissions for the month, 53,000. 31. Recorded revenue earned and billed to clients during the month, 183,500. 31. Purchased land for a future building site for 75,000, paying 7,500 in cash and giving a note payable for the remainder. 31. Paid dividends, 1,000. 31. Rented land purchased on August 31 to a local university for use as a parking lot during football season (September, October, and November); received advance payment of 5,000. Instructions 1. Record the August 1 balance of each account in the appropriate balance column of a four- column account, write Balance in the item section, and place a check mark (0 in the Posting Reference column. 2. Journalize the transactions for August in a two-column journal beginning on Page 18. Journal entry explanations may be omitted. 3. Post to the ledger, extending the account balance to the appropriate balance column after each posting. 4. Prepare an unadjusted trial balance of the ledger as of August 31, 2018. 5. Assume that the August 31 transaction for dividends should have been 10,000. (A) Why did the unadjusted trial balance in (4) balance? (B) Journalize the correcting entry. (C) Is this error a transposition or slide?arrow_forwardExercise 3-40 Revenue and Expense Recognition Electronic Repair Company repaired a high-definition television for Sarah Merrifield in December 2019. Sarah paid $80 at the time of the repair and agreed to pay Electronic Repair $80 each month for 5 months beginning on January 15, 2020. Electronic Repair used $120 of supplies, which were purchased in November 2020, to repair the television. Assume that Electronic Repair uses accrual-basis accounting. Required: In what month or months should revenue from this service be recorded by Electronic Repaid? In what month or months should the expense related to the repair of the television be recorded by Electronic Repair? CONCEPTUAL CONNECTION Describe the accounting principles used to answer the above questions.arrow_forward

- Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement, 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Recorded services provided on account for the period May 115, 9,180. 16. Paid part-time receptionist for two weeks' salary including the amount owed on April 30, 750. 17. Recorded cash from cash clients for fees earned during the period May 116, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Recorded services provided on account for the period May 1620, 4,820. 25. Recorded cash from cash clients for fees earned for the period May 1723, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks' salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Recorded cash from cash clients for fees earned for the period May 2631, 3,300. 31. Recorded services provided on account for the remainder of May, 2,650. 31. Kelly withdrew 10,500 for personal use. Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardJournal entries and trial balance Elite Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on March 31, 2018, follows: The following business transactions were completed by Elite Realty during April 2018: Apr 1. Paid rent on office for month, 6,500. 2. Purchased office supplies on account, 2,300. 5. Paid insurance premiums, 6,000. 10. Received cash from clients on account, 52,300. 15. Purchased land for a future building site for 200,000, paying 30,000 in cash and giving a note payable for the remainder. 17. Paid creditors on account, 6,450. 20. Returned a portion of the office supplies purchased on April 2, receiving full credit for their cost, 325. 23. Paid advertising expense, 4300. Enter the following transactions on Page 19 of the two-column journal: 27. Discovered an error in computing a commission; received cash from the salesperson for the overpayment, 2,500. 28. Paid automobile expense (including rental charges for an automobile), 1,500. 29. Paid miscellaneous expenses, 1,400. 30 Recorded revenue earned and billed to clients during the month, 57,000. 30. Paid salaries and commissions for the month, 11,900. 30. Paid dividends, 4,000. 30. Rented land purchased on April 15 to local merchants association for use as a parking lot in May and June, during a street rebuilding program; received advance payment of 10,000. Instructions 1. Record the April 1, 2018, balance of each account in the appropriate balance column of a four-column account, write Balance in the item section, and place a check mark () in the Posting Reference column. 2. Journalize the transactions for April in a two-column journal beginning on Page 18. Journal entry explanations may be omitted. 3. Post to the ledger, extending the account balance to the appropriate balance column after each posting. 4. Prepare an unadjusted trial balance of the ledger as of April 30, 2018. 5. Assume that the April 30 transaction for salaries and commissions should have been 19,100. (A) Why did the unadjusted trial balance in (4) balance? (B) Journalize the correcting entry. (C) Is this error a transposition or slide?arrow_forwardProblem 2-56A Analyzing Transactions Luis Madero, after working for several years with a large public accounting firm decided to open his own accounting service. The business is operated as a corporation under the name Madero Accounting Services. The following captions and amounts summarize Maderos balance sheet at July 31, 2019. The following events occurred during August 2019. Issued common stock to Ms. Garriz in exchange for $15,000 cash. Paid $850 for first months rent on office space. Purchased supplies of $2,250 on credit. Borrowed $8,000 from the bank. Paid $1,080 on account for supplies purchased earlier on credit. Paid secretarys salary for August of $2,150. Performed amounting services for clients who paid cash upon completion of the service in the total amount of $4,700. Used $3,180 of the supplies on hand. Perfumed accounting services for clients on credit in the total amount of $1,920. Purchased $500 in supplies for cash. Collected $1,290 cash from clients for whom services were performed on credit. Paid $1,000 dividend to stockholders. Required: Record the effects of the transactions listed above on the accounting equation. Use the format given in the problem, starting with the totals at July 31, 20l9. Prepare the trial balance at August 31, 2019.arrow_forward

- Comprehensive problem 1 Kelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement. 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Recorded services provided on account for the period May 1-15; 9,180. 16. Paid part-time receptionist for two weeks salary including the amount owed on April 30, 750. 17. Recorded cash from cash clients for fees earned during the period May 1-16, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Recorded services provided on account for the period May 16-20, 4,820. 25. Recorded cash from cash clients for fees earned for the period May 17-23, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Recorded cash from cash clients for fees earned for the period May 26-31, 3,300. 31. Recorded services provided on account for the remainder of May, 2,650. 31. Paid dividends, 10,500. Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two- column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a retained earnings statement, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account 34 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardOBJECTIVE 9 Exercise 2-47 Debit and Credit Effects of Transactions Lincoln Corporation was involved in the following transactions during the current year: Lincoln borrowed cash from the local bank on a note payable. Lincoln purchased operating assets on credit. Lincoln paid dividends in cash. Lincoln purchased supplies inventory on credit. Lincoln used a portion of the supplies purchased in Transaction d. Lincoln provided services in exchange for cash from the customer. A customer received services from Lincoln on credit. The owners invested cash in the business in exchange for common stock. The payable from Transaction d was paid in full. The receivable from Transaction g was collected in full. Lincoln paid wages in cash. Required: Prepare a table like the one shown below and indicate the effect on assets, liabilities, and stock-holders, equity. Be sure to enter debits and credits in the appropriate columns for each of the transactions. Transaction a is entered as an example:arrow_forward

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning