Concept explainers

Videos

Cost Allocation with Cost Flow Diagram

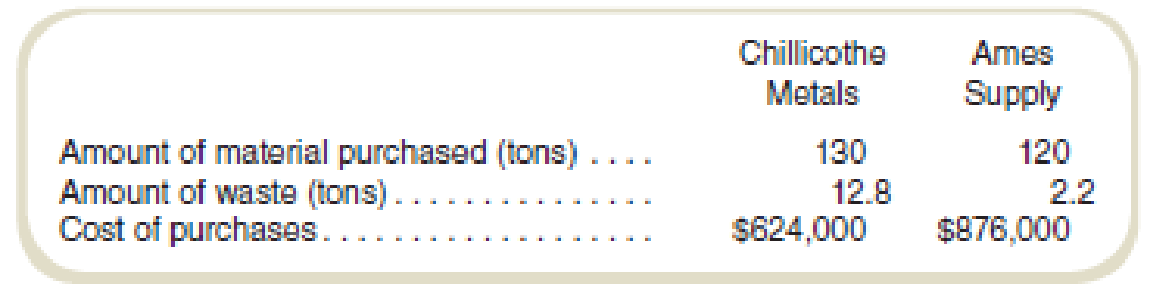

Wayne Casting, Inc., produces a product made from a metal alloy. Wayne buys the alloy from two different suppliers, Chillicothe Metals and Ames Supply, in approximately equal amounts because of supply constraints at both vendors. The material from Chillicothe is less expensive to buy, but more difficult to use, resulting in greater waste. The metal alloy is highly toxic and any waste requires costly handling to avoid environmental accidents. Last year the cost of handling the waste totaled $300,000. Additional data from last year’s operations are shown below.

Required

- a. Allocate the cost of the waste handling to the two suppliers based on:

- 1. Amount of material purchased.

- 2. Amount of waste.

- 3. Cost of material purchased.

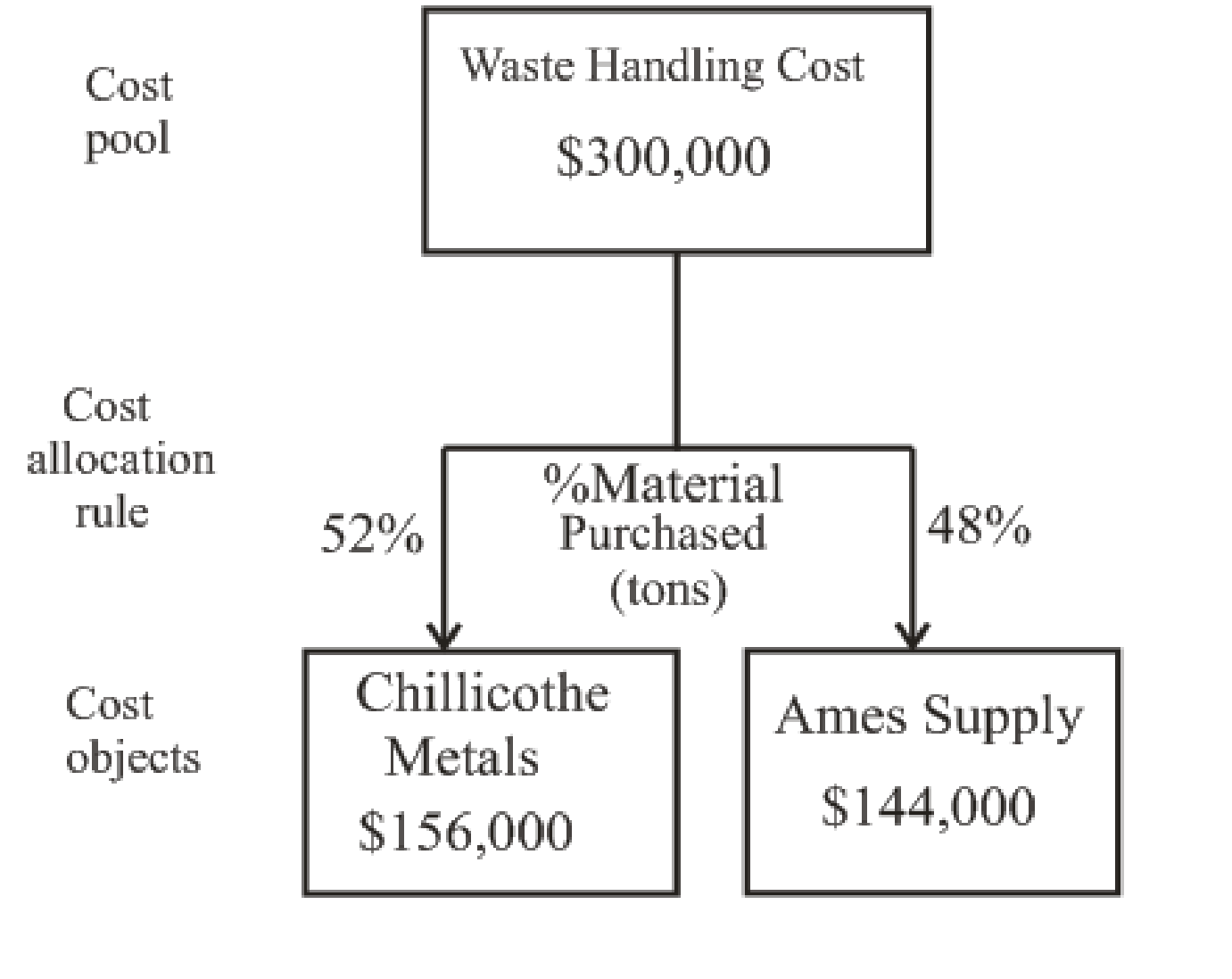

- b. Draw a cost flow diagram to illustrate your answer to requirement (a), part (1).

a.

Allocate the cost of the waste handling to the two suppliers based on:

1. Amount of material purchased.

2. Amount of waste.

3. Cost of material purchased.

Explanation of Solution

Calculate the allocation of the cost of handling the waste on the basis of given variables:

| Chillicothe Ames | Ames Supply |

Total Cost | |||

| Particulars | % | Amount | % | Amount | |

| 1. Based on amount of material purchased: | |||||

| Cost of handling the waste |

52% (1) | $156,000 (3) |

48% (2) | $144,000 (4) | $300,000 |

| 2. Based on amount waste: | |||||

| Cost of handling the waste |

85.33% (5) | $256,000 (7) |

14.67% (6) | $44,000 (8) | $300,000 |

| 3. Based on the cost of material purchased | |||||

| Cost of handling the waste |

41.6% (9) | $124,000 (11) |

58.4% (10) |

$175,200 (12) | $300,000 |

Table: (1)

Calculate the allocation of cost of handling the waste on the basis of the amount of material purchased:

Working note 1:

Allocation for Chillicothe Ames:

Working note 2:

Allocation for Ames Supply:

Working note 3:

Calculate the cost of Chillicothe Ames:

Working note 4:

Calculate the cost of Ames Supply:

Calculate the allocation of cost of handling the waste on the basis of the amount of waste:

Working note 5:

Allocation for Chillicothe Ames:

Working note 6:

Allocation for Ames Supply:

Working note 7:

Calculate the cost of Chillicothe Ames:

Working note 8:

Calculate the cost of Ames Supply:

Calculate the allocation of cost of handling the waste on the basis of cost purchases:

Working note 9:

Allocation for Chillicothe Ames:

Working note 10:

Allocation for Ames Supply:

Working note 11:

Calculate the cost of Chillicothe Ames:

Working note 12:

Calculate the cost of Ames Supply:

b.

Draw a cost flow diagram to illustrate your answer to requirement (a), part (1).

Explanation of Solution

The cost flow diagram to illustrate your answer to requirement (a), part (1):

Figure (1)

Want to see more full solutions like this?

Chapter 2 Solutions

FUNDAMENTALS OF COST ACCOUNTING BUNDLE

- Determining cost relationships Midst ate Containers Inc. manufactures cans for the canned food industry. The operations manager of a can manufacturing operation wants to conduct a cost study investigating the relationship of tin content in the material (can stock) to the energy cost for enameling the cans. The enameling was necessary to prepare the cans for labeling. A higher percentage of tin content in the can stock increases the cost of material. The operations manager believed that a higher tin content in the can stock would reduce the amount of energy used in enameling. During the analysis period, the amount of tin content in the steel can stock was increased for every month, from April to September. The following operating reports were available from the controller: Differences in materials unit costs were entirely related to the amount of tin content. In addition, inventory changes are negligible and are ignored in the analysis. Interpret this information and report to the operations manager your recommendations with respect to tin content.arrow_forwardFunctional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the companys market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way the backpacks were produced. After some discussion, the two managers decided that the problem had to be connected to the addition of the duffel-bag line. Upon investigation, they were informed that the only real change in product-costing procedures was in the way overhead costs are assigned. A two-stage procedure was now in use. First, overhead costs are assigned to the two producing departments, Patterns and Finishing. Second, the costs accumulated in the producing departments are assigned to the two products by using direct labor hours as a driver (the rate in each department is based on direct labor hours). The managers were assured that great care was taken to associate overhead costs with individual products. So that they could construct their own example of overhead cost assignment, the controller provided them with the information necessary to show how accounting costs are assigned to products: The controller remarked that the cost of operating the accounting department had doubled with the addition of the new product line. The increase came because of the need to process additional transactions, which had also doubled in number. During the first year of producing duffel bags, the company produced and sold 100,000 backpacks and 25,000 duffel bags. The 100,000 backpacks matched the prior years output for that product. Required: (Note: Round rates and unit cost to the nearest cent.) 1. CONCEPTUAL CONNECTION Compute the amount of accounting cost assigned to a backpack before the duffel-bag line was added by using a plantwide rate approach based on units produced. Is this assignment accurate? Explain. 2. Suppose that the company decided to assign the accounting costs directly to the product lines by using the number of transactions as the activity driver. What is the accounting cost per unit of backpacks? Per unit of duffel bags? 3. Compute the amount of accounting cost assigned to each backpack and duffel bag by using departmental rates based on direct labor hours. 4. CONCEPTUAL CONNECTION Which way of assigning overhead does the best jobthe functional-based approach by using departmental rates or the activity-based approach by using transactions processed for each product? Explain. Discuss the value of ABC before the duffel-bag line was added.arrow_forwardVariable and Fixed Costs, Cost Formula, High-Low Method Li Ming Yuan and Tiffany Shaden are the department heads for the accounting department and human resources department, respectively, at a large textile firm in the southern United States. They have just returned from an executive meeting at which the necessity of cutting costs and gaining efficiency has been stressed. After talking with Tiffany and some of her staff members, as well as his own staff members, Li Ming discovered that there were a number of costs associated with the claims processing activity. These costs included the salaries of the two paralegals who worked full time on claims processing, the salary of the accountant who cut the checks, the cost of claims forms, checks, envelopes, and postage, and depreciation on the office equipment dedicated to the processing. Some of the paralegals time appears to vary with the routine processing of uncontested claims, but considerable time also appears to be spent on the claims that have incomplete documentation or are contested. The accountants time appears to vary with the number of claims processed. Li Ming was able to separate the costs of processing claims from the costs of running the departments of accounting and human resources. He gathered the data on claims processing cost and the number of claims processed per month for the past 6 months. These data are as follows: Required: 1. Classify the claims processing costs that Li Ming identified as variable and fixed. 2. What is the independent variable? The dependent variable? 3. Use the high-low method to find the fixed cost per month and the variable rate. What is the cost formula? 4. CONCEPTUAL CONNECTION Suppose that an outside company bids on the claims processing business. The bid price is 4.60 per claim. If Tiffany expects 75,600 claims next year, should she outsource the claims processing or continue to do it in-house?arrow_forward

- Activity-based costing and product cost distortion The management of Four Finger Appliance Company in Exercise 14 has asked you to use activity-based costing instead of direct labor hours to allocate factory overhead costs to the two products. You have determined that 81,000 of factory overhead from each of the production departments can be associated with setup activity (162,000 in total). Company records indicate that blenders required 135 setups, while the toaster ovens required only 45 setups. Each product has a production volume of 7,500 units. Determine the three activity rates (assembly, test and pack, and setup). Determine the total factory overhead and factory overhead per unit allocated to each product using the activity rates in (A).arrow_forwardEvaluating selling and administrative cost allocations Gordon Gecco Furniture Company has two major product lines with the following characteristics: Commercial office furniture: Few large orders, little advertising support, shipments in full truckloads, and low handling complexity Home office furniture: Many small orders, large advertising support, shipments in partial truckloads, and high handling complexity The company produced the following profitability report for management: The selling and administrative expenses are allocated to the products on the basis of relative sales dollars. Evaluate the accuracy of this report and recommend an alternative approach.arrow_forwardSouthward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows: The predetermined conversion cost rate is based on available production hours in each cell. The radiator cell has 45,000 hours available for production, and the water pump cell has 27,000 hours. Conversion costs are applied to the units produced by multiplying the conversion rate by the actual time required to produce the units. The radiator cell produced 81,000 units, taking 0.5 hour to produce one unit of product (on average). The water pump cell produced 90,000 units, taking 0.25 hour to produce one unit of product (on average). Other actual results for the year are as follows: All units produced were sold. Any conversion cost variance is closed to Cost of Goods Sold. Required: 1. Calculate the predetermined conversion cost rates for each cell. 2. Prepare journal entries using backflush accounting. Assume two trigger points, with completion of goods as the second trigger point. 3. Repeat Requirement 2, assuming that the second trigger point is the sale of the goods. 4. Explain why there is no need to have a work-in-process inventory account. 5. Two variants of backflush costing were presented in which each used two trigger points, with the second trigger point differing. Suppose that the only trigger point for recognizing manufacturing costs occurs when the goods are sold. How would the entries be listed here? When would this backflush variant be considered appropriate?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning