INTERMEDIATE ACCT VOL.2>CUSTOM<

9th Edition

ISBN: 9781307165067

Author: SPICELAND

Publisher: MCG/CREATE

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 20, Problem 20.2P

P 20-2

Change in principle; change in method of accounting for long-term construction

• LO20–2

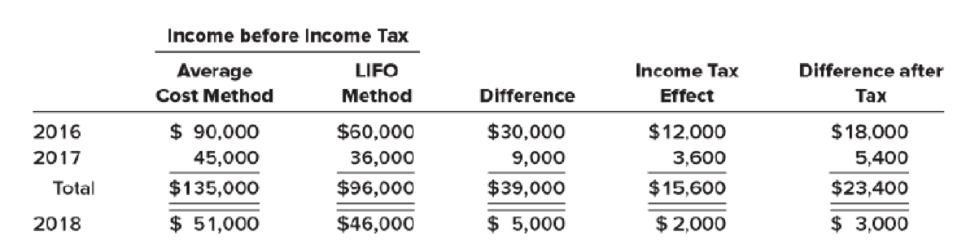

The Pyramid Company has used the LIFO method of accounting for inventory during its first two years of operation, 2016 and 2017. At the beginning of 2018, Pyramid decided to change to the average cost method for both tax and financial reporting purposes. The following table presents information concerning the change for 2016–2018. The income tax rate for all years is 40%.

Pyramid issued 50,000 $1 par, common shares for $230,000 when the business began, and there have been no changes in paid-in capital since then. Dividends were not paid the first year, but $10,000 cash dividends were paid in both 2017 and 2018.

Required:

- 1. Prepare the

journal entry to record the change in accounting principle. - 2. Prepare the 2018–2017 comparative income statements beginning with income before income taxes.

- 3. Prepare the 2018–2017 comparative statements of shareholders’ equity. [Hint: The 2016 statements reported

retained earnings of $36,000. This is $60,000 − ($60,000 × 40%).]

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 20 Solutions

INTERMEDIATE ACCT VOL.2>CUSTOM<

Ch. 20 - Prob. 20.1QCh. 20 - There are three basic accounting approaches to...Ch. 20 - Prob. 20.3QCh. 20 - Lynch Corporation changes from the...Ch. 20 - Sugarbaker Designs Inc. changed from the FIFO...Ch. 20 - Most changes in accounting principles are recorded...Ch. 20 - Southeast Steel, Inc., changed from the FIFO...Ch. 20 - Prob. 20.8QCh. 20 - Its not easy sometimes to distinguish between a...Ch. 20 - For financial reporting, a reporting entity can be...

Ch. 20 - Prob. 20.11QCh. 20 - Describe the process of correcting an error when...Ch. 20 - Prob. 20.13QCh. 20 - If it is discovered that an extraordinary repair...Ch. 20 - Prob. 20.15QCh. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in inventory methods; average cost method...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in depreciation methods LO203 Irwin, Inc.,...Ch. 20 - Prob. 20.5BECh. 20 - Book royalties LO204 Three programmers at Feenix...Ch. 20 - Warranty expense LO204 In 2017, Quapau Products...Ch. 20 - Change in estimate; useful life of patent LO204...Ch. 20 - Prob. 20.9BECh. 20 - Error correction LO206 In 2018, internal auditors...Ch. 20 - Prob. 20.11BECh. 20 - Error correction LO206 In 2018, the internal...Ch. 20 - Change in principle; change in inventory methods ...Ch. 20 - Change in principle; change in inventory methods ...Ch. 20 - Change from the treasury stock method to retired...Ch. 20 - Change in principle; change to the equity method ...Ch. 20 - Prob. 20.5ECh. 20 - FASB codification research LO202 Access the FASB...Ch. 20 - Change in principle; change in inventory cost...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in depreciation methods LO203 For...Ch. 20 - Change in depreciation methods LO203 The Canliss...Ch. 20 - Book royalties LO204 Dreighton Engineering Group...Ch. 20 - Loss contingency LO204 The Commonwealth of...Ch. 20 - Warranty expense LO204 Woodmier Lawn Products...Ch. 20 - Prob. 20.15ECh. 20 - Accounting change LO204 The Peridot Company...Ch. 20 - Change in estimate; useful life and residual value...Ch. 20 - Classifying accounting changes LO201 through...Ch. 20 - Error correction; inventory error LO206 During...Ch. 20 - Error corrections; investment LO206 Required: 1....Ch. 20 - Prob. 20.21ECh. 20 - Prob. 20.22ECh. 20 - Prob. 20.23ECh. 20 - Inventory errors LO206 Indicate with the...Ch. 20 - Classifying accounting changes and errors LO201...Ch. 20 - Change in inventory costing methods; comparative...Ch. 20 - P 20-2 Change in principle; change in method of...Ch. 20 - Change in inventory costing methods; comparative...Ch. 20 - Change in inventory methods LO202 The Rockwell...Ch. 20 - Change in inventory methods LO202 Fantasy...Ch. 20 - Change in principle; change in depreciation...Ch. 20 - Depletion; change in estimate LO204 In 2018, the...Ch. 20 - Accounting changes; six situations LO201, LO203,...Ch. 20 - Prob. 20.9PCh. 20 - Inventory errors LO206 You have been hired as the...Ch. 20 - Error correction; change in depreciation method ...Ch. 20 - Accounting changes and error correction; seven...Ch. 20 - Prob. 20.13PCh. 20 - Prob. 20.14PCh. 20 - Prob. 20.15PCh. 20 - Prob. 20.16PCh. 20 - Prob. 20.17PCh. 20 - Integrating Case 201 Change to dollar-value LIFO ...Ch. 20 - Prob. 20.2BYPCh. 20 - Prob. 20.3BYPCh. 20 - Analysis Case 204 Change in inventory methods;...Ch. 20 - Prob. 20.5BYPCh. 20 - Prob. 20.6BYPCh. 20 - Analysis Case 208 Various changes LO201 through...Ch. 20 - Analysis Case 209 Various changes LO201 through...Ch. 20 - Prob. 20.10BYPCh. 20 - Prob. 20.11BYPCh. 20 - Prob. 20.12BYPCh. 20 - Prob. 1CCTC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Investment reporting O'Brien Industries Inc. is a hook publisher. The comparative unclassified balance sheets for December 31, Year 2 and Year 1 follow. Selected missing balances are shown by letters. Brien Industries Inc. Balance Sheet December 31, Year 2 and Year 1 Dec. 31, Year 2 Dec 31, Year 1 cash 233,000 220,000 Accounts receivable (net) 136,530 138,000 Available for sale investments (at cost)Note 1 a 103,770 Less valuation allowance for available-for-sale investments b. 2,500 Available for-sale investments (fair value) c 101,270 Interest receivable d Investment in Jolly Roger Co. stockNote 2 e. 77,000 Office equipment (net) 115,000 130,000 Total assets f. 666,270 Accounts payable 69.400 65,000 Common stock 70.000 70,000 Excess of issue price over par 225,000 225,000 Retained earnings g 308,770 Unrealized gain (loss) on available for-sale investments h. (2,500) Total liabilities and Stockholders equity i. 666,270 Note 1. Investments are classified as available for sale. The investments at cost and fair value on December 31, Year 1, are as follows: No. of Shares Cost per Share Total Cost Total Fair Value Bernard Co. stock 2,250 17 38,250 37,500 Chadwick Co. stock 1,260 52 65,520 63,770 103,770 101,270 Note 2. The investment in Jolly Roger Co. stock is an equity method investment representing 30% of the outstanding .shares of Jolly Roger Co. The following selected investment transactions occurred during Year 2: May 5. Purchased 3,080 shares of Gozar Inc. at 30 per share including brokerage commission. Gozar Inc. is classified as an available-for-sale security. Oct. 1. Purchased 40,000 of Nightline co. 6%, 10-Year bonds at 100. The bonds are classified as available for sale. The bonds pay interest on October 1 and April 1. 9. Dividends of 12,500 are received on the Jolly Roger co. investment. Dec. 31 Jolly Roger co. reported a total net income of 112,000 for year 2. O'Brien industries Inc. recorded equity earnings for its share of Jolly Roger co. net income. 31. Accrued three months of interest on the Nightline bonds. 31. Adjusted the available-for-sale investment portfolio to fair value, using the following fair value per-share amounts: Available-for-Sale Investments Fair Value Bernard Co. stock 15,40 per share Chadwick Co. stock 46,00 per share Gozar Inc. stock 32,00 per share Nightline Co. bonds 98 per 100 of face amount Dec. 31. Closed the OBrien Industries Inc. net income of 146,230. O'Brien Industries Inc. paid no dividends during the year. Instructions Determine the missing letters in the unclassified balance sheet. Provide appropriate supporting calculations.arrow_forwardInvestment reporting Teasdale Inc. manufactures and sells commercial and residential security equipment. The comparative unclassified balance sheets for December 31, Year 2 and Year 1 are provided below. Selected missing balances are shown by letters. Teasdale Inc. Balance Sheet December 31, Year 2 and Year 1 Dec. 31, Year 2 Dec. 31, Year 1 Cash 160,000 156,000 Accounts receivable (net) 11S.OOO 108,000 Available for-sale investments (at cost)Note 1 a. 91,200 Plus valuation allowance for available-for-sale investments b. 8,776 Available for-sale investments (fair value) c 99,976 Interest receivable d. Investment in Wright Co. stockNote 2 e. 69,200 Office equipment (net) 96,000 105,000 Total assets f. 5538,176 Accounts payable 91,000 72,000 Common stock 80,000 80,000 Excess of issue price over par 250,000 250,000 Retained earnings g 127,400 Unrealized gain (loss) on available for-sale investments h. 8,776 Total liabilities and stockholders' equity S i. 5538,176 Note 1. Investments are classified as available for sale. The investments at cost and fair value on December 31, Year 1, are as follows: No. of Shares Cost per Share Total Cost Total Fair Value Alvarez Inc stock 960 38,00 36,480 39,936 Hirsch Inc. stock 1,900 28,80 4,720 60,040 91,200 99,976 Note 2. The Investment in Wright Co. stack is an equity method investment representing 30% of the outstanding shares of Wright Co. The following selected investment transactions occurred during Year 2: Mar. 18. Purchased 800 shares of Richter Inc. at 40, including brokerage commission. Richter is classified as an available-for-sale security. July 12. Dividends of 12,000 art: received on the Wright Co. investment. Oct 1. Purchased 24,000 of Toon Co. 4%, 10-year bonds at 100. the bonds are classified as available for sale. The bonds pay interest on October 1 and April 1. December 31. Wright Co. reported a total net income of 80,000 for Year 2. Teasdale recorder equity earnings for its share of Wright Co. net income. 31. Accrued interest for three months on the Toon Co. bonds purchased on October 1. 31. Adjusted the available-for-sale investment portfolio to fair value, using the following fair value per-share amounts: Available for Sale Investments Fair Value Alvarez Inc. stock 41,50 per share Hirsch Inc stock 26,00 per share Richter Inc. stock 48,00 per share Toon Co. bonds 101 per 100 of face amount 31. Closed the Teasdale Inc. net income of 51,240. Teasdale Int. paid no dividends during the year. Instructions Determine the missing letters in the unclassified balance sheet. Provide appropriate supporting calculations.arrow_forwardNineteen measures of solvency and profitability The comparative financial statements of Bettancort Inc. are as follows. The market price of Bettancort Inc. common stock was 71.25 on December 31, 2016. Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Retained earnings. January 1......................................... 2,655,000 2,400,000 Add net income for year............................................. 300,000 280,000 Total............................................................... 2,955,000 2,680,000 Deduct dividends: On preferred stock................................................ 15,000 15,000 On common stock................................................. 10,000 10,000 Total........................................................... 25,000 25,000 Retained earnings. December 31..................................... 2,930,000 2,655,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Sales...................... 1,200,000 1,000,000 Cost of goods sold............ 500,000 475,000 Gross profit............... 700,000 525,000 Selling expenses.......... 240,000 200,000 Administrative expenses...... 180,000 150,000 Total operating expenses.. 420,000 350,000 Income from operations.. 280,000 175,000 Other income............. 166,000 225,000 446,000 400,000 Other expense (Interest)... 66,000 60,000 Income before income tax 380,000 340,000 Income tax expense....... 80,000 60,000 Net income............... 300,000 280,000 Bettancort Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 Dec.31, 2016 Dec. 31, 2015 Assets Current Assets: Cash.................................... 450,000 400,000 Marketable securities.................... 300,000 260,000 Accounts receivable (net)................. 130,000 110,000 Inventories.............................. 67,000 58,000 Prepaid expenses........................ 153,000 139,000 Total current assets..................... 1,100,000 967,000 Long-term investments.................... 2,350,000 2,200,000 Property, plant and equipment (net)....... 1,320,000 1,118,000 Total assets............................... 4,770,000 4,355,000 Liabilities Current liabilities.......................... 440,000 400,000 Long-term liabilities: Mortgage note payable, 8.8%, due 2021... 100,000 0 Bonds payable, 9%, due 2017............. 1,000,000 1,000,000 Total long term liabilities............... 1,100,000 1,000,000 Total liabilities............................ 1,540,000 1,400,000 Stockholders' equity Preferred stock 0.90, 10 par.. 200,000 200,000 Common stock. 5 par..................... 100,000 100,000 Retained earnings......................... 2,930,000 2,665,000 Total stockholders equity............... 3,230,000 2,955,000 Total liabilities and stockholders' equity..... 4,770,000 4,355,000 Instructions Determine the following measures for 2016, rounding to one decimal place: 1. Working capital 2. Current ratio 3. Quick ratio 4. Accounts receivable turnover 5. Number of days' sales in receivables 6. Inventory turnover 7. Number of days' sales in inventory 8. Ratio of fixed assets to long-term liabilities 9. Ratio of liabilities to stockholders equity 10. Number of times interest charges are earned 11. Number of times preferred dividends are earned 12. Ratio of sales to assets 13. Rate earned on total assets 14. Rate earned on stockholders' equity 15. Rate earned on common stockholders' equity 16. Earnings per share on common stock 17. Price-earnings ratio 18. Dividends per share of common stock 19. Dividend yieldarrow_forward

- Current liabilities Bon Nebo Co. sold 25,000 annual subscriptions of Bjorn for 85 during December 20Y5. These new subscribers will receive monthly issues, beginning in January 20Y6. In addition, the business had taxable income of 840,000 during the first calendar quarter of 20Y6. The federal tax rate is 40%. A quarterly tax payment will be made on April 12, 20Y6. Prepare the current liabilities section of the balance sheet for Bon Nebo Co. on March 31, 20Y6.arrow_forwardNineteen measures of solvency and profitability The comparative financial statements of Stargel Inc. are as follows. The market price of Stargel Inc. common stock was 119.70 on December 31, 2016. Stargel Inc. Comparative Retained Earnings Statement For the Years Ended December 31, 2016 and 2015 2016 2015 Retained earnings, January 1................ 5,375,000 4,545,000 Add net income for year......................... 900,000 925,000 Total..................................... 6,275,000 5,470,000 Deduct dividends: On preferred stock............................................. 45,000 45,000 On common stock.............................................. 50,000 50,000 Total........................................................ 95,0000 95,000 Retained earnings, December 3................................... 6,180,000 5,375,000 Stargel Inc. Comparative Income Statement For the Year Ended December 31, 2016 and 2015 2016 2015 Sales..................... 10,000,000 9,400,000 Cost of goods sold......... 5,350,000 4,950,000 Gross profit............... 4,650,000 4,450,000 Selling expenses.......... 2,000,000 1,080,000 Administrative expenses... 1,500.000 1,410,000 Total operating expenses 3,500,000 3,290,000 Income from operations ... 1,150,000 1,160,000 Other income............. 150,000 140,000 1,300,000 1,300,000 Other expense (interest). 170,000 150,000 Income before income tax 1,130,000 1,150,000 Income tax expense....... 230,000 225,000 Net income............... 900,000 925,000 Stargel Inc. Comparative Income Statement For the Year Ended December 31, 2016 and 2015 Dec.31, 2016 Dec. 31, 2015 Assets Current Assets: Cash.................................... 500,000 400,000 Marketable securities.................... 1,010,000 1,000,000 Accounts receivable (net)................. 740,000 510,000 Inventories.............................. 1,190000 950,000 Prepaid expenses........................ 250,000 229,000 Total current assets..................... 3,690,000 3,089,000 Long-term investments.................... 2,350,000 2,300,000 Property, plant and equipment (net)....... 3,740,000 3,366,000 Total assets............................... 9,780,000 8,755,000 Liabilities Current liabilities.......................... 900,000 880,000 Long-term liabilities: Mortgage note payable, 8.8%, due 2021... 200,000 0 Bonds payable, 9%, due 2017............. 1,500,000 1,500,000 Total long term liabilities............... 1,700,000 1,500,000 Total liabilities............................ 2,600,000 2,380,000 Stockholders' equity Preferred stock 0.90, 10 par.. 500,000 500,000 Common stock. 5 par..................... 500,000 500,000 Retained earnings......................... 6,180,000 5,375,000 Total stockholders' equity............... 7,180,000 6,375,000 Total liabilities and stockholders' equity..... 9,780,000 8,755,000 Instructions Determine the following measures for 2016, rounding to one decimal place, except per share amounts, which should be rounded to the nearest penny: 1. Working capital 2. Current ratio 3. Quick ratio 4. Accounts receivable turnover 5. Number of days salts in receivables 6. Inventory turnover 7. Number of days sales in inventory 8. Ratio of fixed assets to long-term liabilities 9. Ratio of liabilities to .stockholders' equity 10. Number of times interest charges are earned 11. Number of times preferred dividends are earned 12. Ratio of sales to assets 13. Rate earned on total assets 14. Rate earned on stockholders' equity 15. Rate earned on common stockholders' equity 16. Earnings per share on common stock 17. Price-earnings ratio 18. Dividends per share of common stock 19. Dividend yieldarrow_forwardA main goal of JIT is zero inventories. a. Assume your company does not aspire to JIT and has 3,000,000 in raw materials in stock. Identify costs that may be incurred to maintain the inventory level. b. Now assume that you implement JIT, and your raw materials in stock drop to zero. Explain how you expect this change to impact your income statement and balance sheet.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781337398169Author:Carl Warren, Jeff JonesPublisher:Cengage Learning Accounting Information SystemsFinanceISBN:9781337552127Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan HillPublisher:Cengage Learning

Accounting Information SystemsFinanceISBN:9781337552127Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan HillPublisher:Cengage Learning

Accounting

Accounting

ISBN:9781337272094

Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.

Publisher:Cengage Learning,

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Accounting (Text Only)

Accounting

ISBN:9781285743615

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:9781305653535

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:9781337398169

Author:Carl Warren, Jeff Jones

Publisher:Cengage Learning

Accounting Information Systems

Finance

ISBN:9781337552127

Author:Ulric J. Gelinas, Richard B. Dull, Patrick Wheeler, Mary Callahan Hill

Publisher:Cengage Learning

The ACCOUNTING EQUATION For BEGINNERS; Author: Accounting Stuff;https://www.youtube.com/watch?v=56xscQ4viWE;License: Standard Youtube License