Concept explainers

Videos

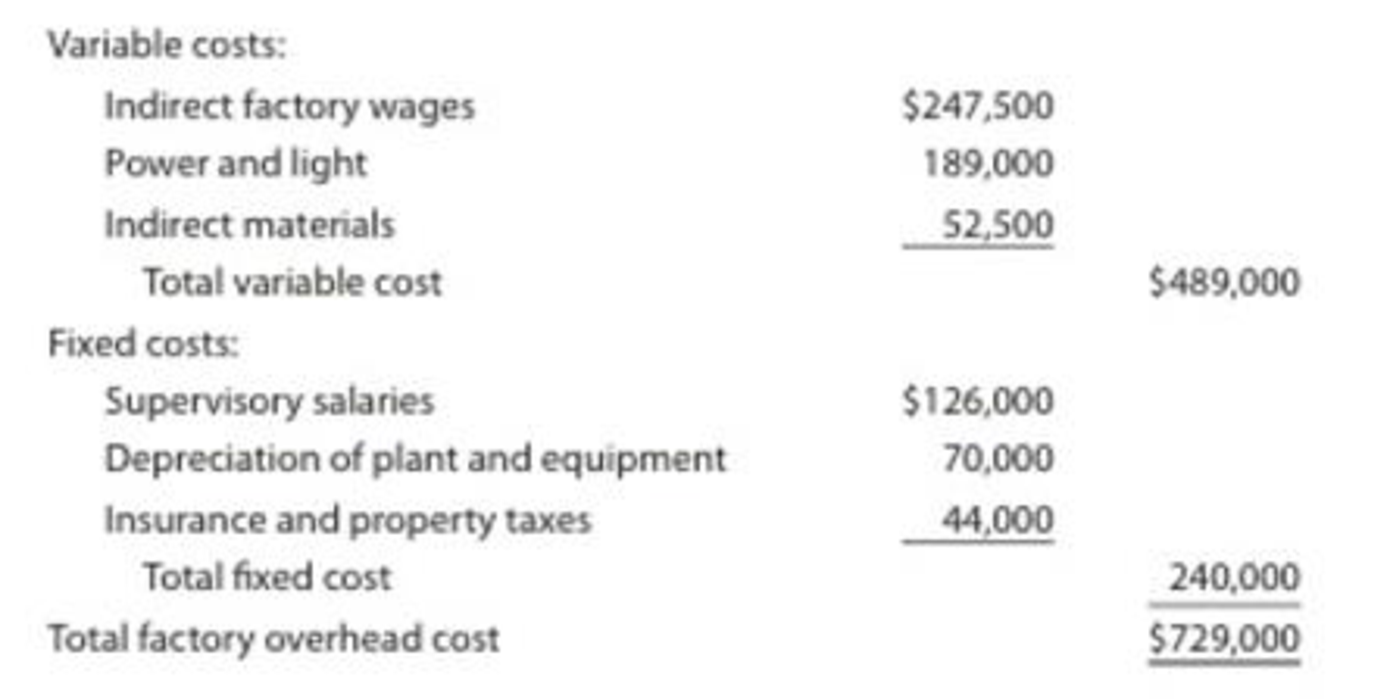

Feeling Better Medical Inc., a manufacturer of disposable medical supplies, prepared the following factory overhead cost budget for the Assembly Department for October of the current year. The company expected to operate the department at 100% of normal capacity of 30,000 hours.

During October, the department operated at 28,500 hours, and the factory overhead costs incurred were indirect factory wages, $234,000; power and light, $178,500; indirect materials, $50,600; supervisory salaries, $126,000;

Instructions

Prepare a factory overhead cost variance report for October. To be useful for cost control, the budgeted amounts should be based on 28,500 hours.

Want to see the full answer?

Check out a sample textbook solution

Chapter 23 Solutions

FINANCIAL & MANAGERIAL ACCW/CENGAGENOWV

- Factory overhead cost variance report Tiger Equipment Inc., a manufacturer of construction equipment, prepared the following factory overhead cost budget for the Welding Department for May of the current year. The company expected to operate the department at 100% of normal capacity of 8,400 hours. During May, the department operated at 8,860 hours, and the factory overhead costs incurred were indirect factory wages, 32,400; power and light, 21,000; indirect materials, 18,250; supervisory salaries, 20,000; depreciation of plant and equipment, 36,200; and insurance and property taxes, 15,200. Instructions Prepare a factory overhead cost variance report for May. To be useful for cost control, the budgeted amounts should be based on 8,860 hours.arrow_forwardFactory overhead cost variance report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 20,000 hours for production: Tannin has available 25,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 22,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Construct a factory overhead cost variance report for the Trim Department for July.arrow_forwardSalisbury Bottle Company manufactures plastic two-liter bottles for the beverage industry. The cost standards per 100 two-liter bottles are as follows: At the beginning of March, Salisburys management planned to produce 500,000 bottles. The actual number of bottles produced for March was 525,000 bottles. The actual costs for March of the current year were as follows: a. Prepare the March manufacturing standard cost budget (direct labor, direct materials, and factory overhead) for Salisbury, assuming planned production. b. Prepare a budget performance report for manufacturing costs, showing the total cost variances for direct materials, direct labor, and factory overhead for March. c. Interpret the budget performance report.arrow_forward

- Calculating factory overhead The standard capacity of a factory is 8,000 units per month. Cost and production data follow: Calculate the amount of factory overhead allowed for the actual volume of production each month and the variance between budgeted and actual overhead for each month.arrow_forwardThomas Textiles Corporation began November with a budget for 60,000 hours of production in the Weaving Department. The department has a full capacity of 75,000 hours under normal business conditions. The budgeted overhead at the planned volumes at the beginning of November was as follows: The actual factory overhead was 725,000 for November. The actual fixed factory overhead was as budgeted. During November, the Weaving Department had standard hours at actual production volume of 64,500 hours. a. Determine the variable factory overhead controllable variance. b. Determine the fixed factory overhead volume variance.arrow_forwardBusiness Specialty, Inc., manufactures two staplers: small and regular. The standard quantities of direct labor and direct materials per unit for the year are as follows: The standard price paid per pound of direct materials is 1.60. The standard rate for labor is 8.00. Overhead is applied on the basis of direct labor hours. A plantwide rate is used. Budgeted overhead for the year is as follows: The company expects to work 12,000 direct labor hours during the year; standard overhead rates are computed using this activity level. For every small stapler produced, the company produces two regular staplers. Actual operating data for the year are as follows: a. Units produced: small staplers, 35,000; regular staplers, 70,000. b. Direct materials purchased and used: 56,000 pounds at 1.5513,000 for the small stapler and 43,000 for the regular stapler. There were no beginning or ending direct materials inventories. c. Direct labor: 14,800 hours3,600 hours for the small stapler and 11,200 hours for the regular stapler. Total cost of direct labor: 114,700. d. Variable overhead: 607,500. e. Fixed overhead: 350,000. Required: 1. Prepare a standard cost sheet showing the unit cost for each product. 2. Compute the direct materials price and usage variances for each product. Prepare journal entries to record direct materials activity. 3. Compute the direct labor rate and efficiency variances for each product. Prepare journal entries to record direct labor activity. 4. Compute the variances for fixed and variable overhead. Prepare journal entries to record overhead activity. All variances are closed to Cost of Goods Sold. 5. Assume that you know only the total direct materials used for both products and the total direct labor hours used for both products. Can you compute the total direct materials and direct labor usage variances? Explain.arrow_forward

- Case made 24,500 units during June, using 32,000 direct labor hours. They expected to use 31,450 hours per the standard cost card. Their employees were paid $15.75 per hour for the month of June. The standard cost card uses $15.50 as the standard hourly rate. A. Compute the direct labor rate and time variances for the month of June, and also calculate the total direct labor variance. B. If the standard rate per hour was $16.00, what would change?arrow_forwardA company estimates its manufacturing overhead will be $840,000 for the next year. What is the predetermined overhead rate given each of the following Independent allocation bases? Budgeted direct labor hours: 90,615 Budgeted direct labor expense: $750000 Estimated machine hours: 150,000arrow_forwardThe cost accountant for River Rock Beverage Co. estimated that total factory overhead cost for the Blending Department for the coming fiscal year beginning February 1 would be 3,150,000, and total direct labor costs would be 1,800,000. During February, the actual direct labor cost totalled 160,000, and factory overhead cost incurred totaled 283,900. a. What is the predetermined factory overhead rate based on direct labor cost? b. Journalize the entry to apply factory overhead to production for February. c. What is the February 28 balance of the account Factory OverheadBlending Department? d. Does the balance in part (c) represent over- or underapplied factory overhead?arrow_forward

- Flaherty, Inc., has just completed its first year of operations. The unit costs on a normal costing basis are as follows: During the year, the company had the following activity: Actual fixed overhead was 12,000 less than budgeted fixed overhead. Budgeted variable overhead was 5,000 less than the actual variable overhead. The company used an expected actual activity level of 12,000 direct labor hours to compute the predetermined overhead rates. Any overhead variances are closed to Cost of Goods Sold. Required: 1. Compute the unit cost using (a) absorption costing and (b) variable costing. 2. Prepare an absorption-costing income statement. 3. Prepare a variable-costing income statement. 4. Reconcile the difference between the two income statements.arrow_forwardShinto Corp. uses a standard cost system and manufactures one product. The variable costs per product follow: Budgeted fixed overhead costs for the month are $4,000, and Shinto expected to manufacture 2,000 units. Actual production, however, was only 1,800 units. Materials prices were 10% over standard, and labor rates were 5% over standard. Of the factory overhead expense, only 80% was used, and fixed overhead was $100 over budget. The actual variable overhead cost was $4,800. In materials usage, 8% more parts were used than were allowed for actual production by the standard, and 6% more labor hours were used than were allowed. Required: Calculate the materials and labor variances. Calculate the variances for overhead by the four-variance method. (Hint: First compute the fixed and variable overhead rates per hour.)arrow_forwardFlexible budget for factory overhead Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month. The predetermined overhead rate is based on normal capacity. Required: 1. Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of 80%, 90%, and 110% of normal capacity. Also determine the predetermined factory overhead rate at each level of volume in both units and direct labor hours. 2. Prepare a flexible budget for production levels of 80%, 90%, and 110%, assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions. (Hint: Set up a third category for semi-variable expenses.) a. At 110% of capacity, another supervisor will be needed at a salary of 24,000 annually. b. At 80% of capacity, the repairs expense will drop to one-half of the amount at 100% capacity. c. At 80% of capacity, one part-time maintenance worker, earning 10,000 a year, will be laid off. d. At 110% of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was 12,000, it has a 10-year life, and straight-line depreciation will be taken.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College