Managerial Accounting

16th Edition

ISBN: 9781259995484

Author: Ray Garrison

Publisher: MCGRAW-HILL HIGHER EDUCATION

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 4, Problem 16P

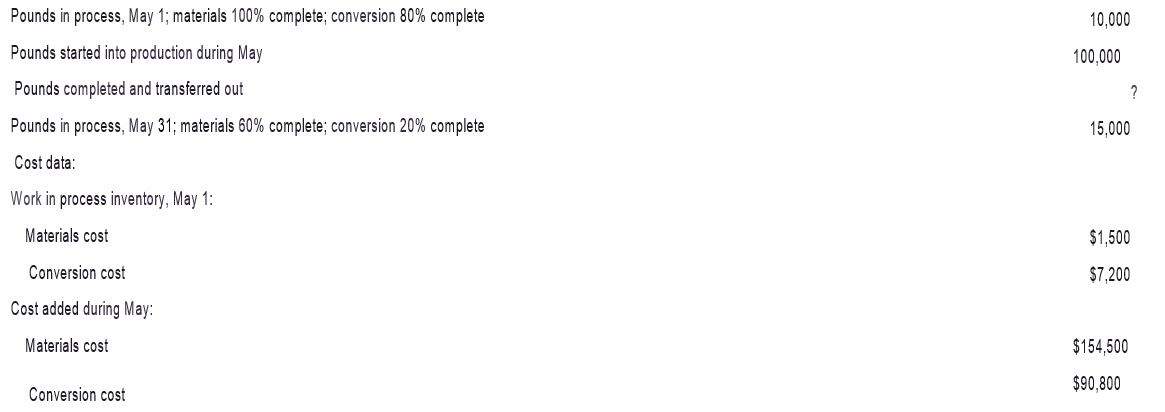

PROBLEM 4-16 Comprehensive Problem-Weighted-Average Method LO4-2, LO4-3, LO4-4, LO4-5

Builder Products, Inc., uses the weighted-average method in its

Production data:

Required:

- Compute the equivalent units of production for materials and conversion for May.

- Compute the cost per equivalent unit for materials and conversion for May.

- Compute the cost of ending work in process inventory’ for materials, conversion, and in total for May.

- Compute the cost of units transferred out to the nest department for materials, conversion, and in total for May.

- Prepare a cost reconciliation report for May

Expert Solution & Answer

Trending nowThis is a popular solution!

Students have asked these similar questions

Problem 8-53 (Static) Prepare a Production Cost Report: Weighted-Average Method (LO 8-3, 4)

Kansas Supplies is a manufacturer of plastic parts that uses the weighted-average process costing method to account for costs of production. It produces parts in three separate departments: Molding, Assembling, and Packaging. The following information was obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding Department

$

192,000

100

%

Costs added by the Assembling Department

Direct materials

$

120,000

100

%

Direct labor

43,200

60

%

Manufacturing overhead

27,600

50

%

$

190,800

Work in process, April 1

$

382,800

During April, 375,000 units were transferred in from the Molding Department at a cost of $960,000. The Assembling Department added the following…

Problem 8-53 (Static) Prepare a Production Cost Report: Weighted-Average Method (LO 8-3, 4)

Kansas Supplies is a manufacturer of plastic parts that uses the weighted-average process costing method to account for costs of production. It produces parts in three separate departments: Molding, Assembling, and Packaging. The following information was obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding Department

$

192,000

100

%

Costs added by the Assembling Department

Direct materials

$

120,000

100

%

Direct labor

43,200

60

%

Manufacturing overhead

27,600

50

%

$

190,800

Work in process, April 1

$

382,800

During April, 375,000 units were transferred in from the Molding Department at a cost of $960,000. The Assembling Department added the following…

Problem 8-54 (Static) Prepare a Production Cost Report: FIFO Method (LO 8-4, 5)

Kansas Supplies is a manufacturer of plastic parts that uses the weighted-average process costing method to account for costs of production. It produces parts in three separate departments: Molding, Assembling, and Packaging. The following information was obtained for the Assembling Department for the month of April.

Work in process on April 1 had 75,000 units made up of the following.

Amount

Degree of Completion

Prior department costs transferred in from the Molding Department

$

192,000

100

%

Costs added by the Assembling Department

Direct materials

$

120,000

100

%

Direct labor

43,200

60

%

Manufacturing overhead

27,600

50

%

$

190,800

Work in process, April 1

$

382,800

During April, 375,000 units were transferred in from the Molding Department at a cost of $960,000. The Assembling Department added the following costs.…

Chapter 4 Solutions

Managerial Accounting

Ch. 4.A - EXERCISE 4A-1 Computation of Equivalent Units of...Ch. 4.A - EXERCISE 4A-2 Cost per Equivalent Unit-FIFO Method...Ch. 4.A - EXERCISE 4A-3 Assigning Costs to Units-FIFO Method...Ch. 4.A - EXERCISE 4A-4 Cost Reconciliation Report-EIFO...Ch. 4.A - EXERCISE 4A-5 Computation of Equivalent Units of...Ch. 4.A - EXERCISE 4A-6 Equivalent Units of Production-FIFO...Ch. 4.A - EXERCISE 4A-7 Equivalent Units of Production and...Ch. 4.A -

EXERCISE 4A-8 Equivalent Units of Production—FIFO...Ch. 4.A - EXERCISE 4A-9 Equivalent Units; Equivalent Units...Ch. 4.A - PROBLEM 4A-10 Equivalent Units of Production;...

Ch. 4.A - Prob. 11PCh. 4.A - Prob. 12CCh. 4.B - Prob. 1ECh. 4.B - EXERCISE 4B-2 Step-Down Method LO4-11 Madison Park...Ch. 4.B - Prob. 3ECh. 4.B - EXERCISE 4B-4 Direct Method LO4-10 Refer to the...Ch. 4.B - PROBLEM 4B-5 Step-Down Method L04-11 Woodbury...Ch. 4.B - PROBLEM 4B-6 Step-Down Method versus Direct...Ch. 4.B - CASE 4B-7 Step-Down Method versus Direct Method...Ch. 4 - Prob. 1QCh. 4 - In what ways are job-order and process costing...Ch. 4 - Why is cost accumulation simpler in a process...Ch. 4 - How many Work in Process accounts are maintained...Ch. 4 - Prob. 5QCh. 4 - Prob. 6QCh. 4 - Prob. 7QCh. 4 - Prob. 8QCh. 4 - Prob. 1AECh. 4 - This exercise relates to the Double Diamond Skis’...Ch. 4 - This exercise relates to the Double Diamond Skis’...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 -

Clopack Company manufactures one product that...Ch. 4 -

Clopack Company manufactures one product that...Ch. 4 -

Clopack Company manufactures one product that...Ch. 4 - Clopack Company manufactures one product that goes...Ch. 4 - Prob. 10F15Ch. 4 - Prob. 11F15Ch. 4 - Prob. 12F15Ch. 4 -

Clopack Company manufactures one product that...Ch. 4 - Prob. 14F15Ch. 4 - Prob. 15F15Ch. 4 - Prob. 1ECh. 4 - Prob. 2ECh. 4 - Prob. 3ECh. 4 - EXERCISE 4-4 Assigning Costs to...Ch. 4 - EXERCISE 4-5 Cost Reconciliation...Ch. 4 - Prob. 6ECh. 4 - Prob. 7ECh. 4 - Prob. 8ECh. 4 -

EXERCISE 4-9 Equivalent Units and Cost per...Ch. 4 - Prob. 10ECh. 4 - Prob. 11ECh. 4 - Prob. 12ECh. 4 - Prob. 13PCh. 4 - Prob. 14PCh. 4 - Prob. 15PCh. 4 - PROBLEM 4-16 Comprehensive...Ch. 4 - Prob. 17PCh. 4 - Prob. 18PCh. 4 - Prob. 19CCh. 4 - (

CASE 4-20 Ethics and the Manager, Understanding...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Single plantwide rate and activity-based costing Whirlpool Corporation conducted an activity-based costing study of its Evansville, Indiana, plant in order to identify its most profitable products. Assume that we select three representative refrigerators (out of 333): one low-, one medium-, and one high-volume refrigerator. Additionally, we assume the following activity-base information for each of the three refrigerators: Prior to conducting the study, the factory overhead allocation was based on a single machine hour rate. The machine hour rate was 200 per hour. After conducting the activity-based costing study, assume that three activities were used to allocate the factory overhead. The new activity rate information is assumed to be as follows: Machining Activity Setup Activity Sales order Processing Activity Activity rate 160 240 55 A. Complete the following table, using the single machine hour rate to determine the per-unit factory overhead for each refrigerator (Column A) and the three activity-based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity-based rate methods (Column C). (Round per-unit overhead to two decimal places and percents to one decimal place.) Product Volume Class Column A Single Rate Overhead Allocation per Unit Column B ABC Overhead Allocation per Unit Column C Percent Change in Allocation (Col. B - Col. A)/Col. A Low Medium High B. Why is the traditional overhead rate per machine hour greater under the single rate method than under the activity-based method? C. Interpret Column C in your table from part (A).arrow_forwardFIFO Method, Single Department Analysis, One Cost Category Refer to the data in Problem 6.33. Required: Prepare a cost of production report for the Fabrication Department for December using the FIFO method of costing.arrow_forwardSingle plantwide rate and activity-based costing Whirlpool Corporation conducted an activity-based costing study of its Evansville, Indiana, plant in order to identify its most profitable products. Assume that we select three representative refrigerators (out of 333): one low-, one medium-, and one high-volume refrigerator. Additionally, we assume the following activity-base information for each of the three refrigerators: Prior to conducting the study, the factory overhead allocation was based on a single machine hour rate. The machine hour rate was 200 per hour. After conducting the activity-based costing study, assume that three activities were used to allocate the factory overhead. The new activity rate information is assumed to be as follows: Machining Activity Setup Activity Sales order Processing Activity Activity rate 160 240 55 A. Complete the following table, using the single machine hour rate to determine the per-unit factory overhead for each refrigerator (Column A) and the three activity-based rates to determine the activity-based factory overhead per unit (Column B). Finally, compute the percent change in per-unit allocation from the single to activity-based rate methods (Column C). (Round per-unit overhead to two decimal places and percents to one decimal place.) Product Volume Class Column A Single Rate Overhead Allocation per Unit Column B ABC Overhead Allocation per Unit Column C Percent Change in Allocation (Col. B - Col. A)/Col. A Low Medium High B. Why is the traditional overhead rate per machine hour greater under the single rate method than under the activity-based method? C. Interpret Column C in your table from part (A).arrow_forward

- Activity-based costing and product cost distortion The management of Four Finger Appliance Company in Exercise 14 has asked you to u.sc activity-based costing instead of direct labor hours to allocate factory overhead costs to the two products. You have determined that 81,000 of factory overhead from each of the production departments can be associated with setup activity (162,000 in total). Company records indicate that blenders required 135 setups, while the toaster ovens required only 45 setups. Each product has a production volume of 7,500 units. A. Determine the three activity rates (assembly, test and pack, and setup). B. Determine the total factory overhead and factory overhead per unit allocated to each product using the activity rates in (A).arrow_forward(Appendix 4B) Assigning Support Department Costs by Using the Direct Method Sanjay Company manufactures a product in a factory that has two producing departments, Assembly and Painting, and two support departments, S1 and S2. The activity driver for S1 is square footage, and the activity driver for S2 is number of machine hours. The following data pertain to Sanjay: Support Departments Producing Departments S1 S2 Assembly Painting Direct costs $200,000 $140,000 $115,000 $96,000 Normal activity: Square footage — 500 1,875 625 Machine hours 337 — 3,200 12,800 Required: 1. Calculate the cost assignment ratios to be used under the direct method for Departments S1 and S2. (Note: Each support department will have two ratios—one for Assembly and the other for Painting.) Round your answers to two decimal places. Assembly Painting S1 fill in the blank 1 fill in the blank 2 S2 fill in the blank 3 fill in the blank 4 2. Allocate the support department…arrow_forwardExercise 4-12 (Algo) Equivalent Units; Assigning Costs; Cost Reconciliation—Weighted-Average Method [LO4-2, LO4-4, LO4-5] Superior Micro Products uses the weighted-average method in its process costing system. During January, the Delta Assembly Department completed its processing of 26,500 units and transferred them to the next department. The cost of beginning work in process inventory and the costs added during January amounted to $733,290 in total. The ending work in process inventory in January consisted of 4,000 units, which were 50% complete with respect to materials and 30% complete with respect to labor and overhead. The costs per equivalent unit for the month were as follows: Materials Labor Overhead Cost per equivalent unit $ 12.90 $ 5.00 $ 8.20 Required: 1. Compute the equivalent units of materials, labor, and overhead in the ending work in process inventory for the month. 2. Compute the cost of ending work in…arrow_forward

- 30. Process costing techniques should be used in assigning costs to products a. when production is customized to individual customer's requests b. if the products are manufactured on the basis of each order received. c. when production is only partially completed during the accounting period. d. if the products are composed of mass-produced, homogeneous units. 31. D Company uses the FIFO method of process costing. The beginning work-in-process inventory consisted of $6,400 of materials cost and $9,600 of conversion cost. Current month costs were $31,740 for materials and $51,100 for conversion. Equivalent Units have already been calculated for you under the FIFO method and were 69,000 equivalent units for materials and 70,000 equivalent units for conversion. Ending inventory of 5,000 units were 100% completed as to materials and 40% completed as to conversion. The cost assigned to ending work-in-process inventory would be _____. a. $3,760 b. $3,200 c. none of the other answers…arrow_forwardQUESTION 1Eman Sdn Bhd (ESB) is a manufacturer of superior rubbish bin, uses the weightedaverage method in its process costing system. ESB has produced the rubbish bin thatpasses through two processing departments: Moulding Department and FinishingDepartment. In the Moulding Department, all direct materials are added at the beginningof the process. Direct labor and manufacturing overhead are added uniformly. Percentageof completion in the Moulding Department for conversion costs is 30 percent for beginningwork in process and 60 percent for ending work in process. Information related to theMoulding Department during March 2021 was summarized as follows: REQUIRED:(a) Prepare the physical units from units to account for, units accounted for andequivalent units.(b) Calculate cost per equivalent units.(c) Calculate total cost for completed and transferred out and ending work in process.arrow_forwardQUESTION 1Eman Sdn Bhd (ESB) is a manufacturer of superior rubbish bin, uses the weightedaverage method in its process costing system. ESB has produced the rubbish bin thatpasses through two processing departments: Moulding Department and FinishingDepartment. In the Moulding Department, all direct materials are added at the beginningof the process. Direct labor and manufacturing overhead are added uniformly. Percentageof completion in the Moulding Department for conversion costs is 30 percent for beginningwork in process and 60 percent for ending work in process. Information related to theMoulding Department during March 2021 was summarized as follows:REQUIRED:(a) Prepare the physical units from units to account for, units accounted for andequivalent units.(b) Calculate cost per equivalent units.(c) Calculate total cost for completed and transferred out and ending work in process.(d) Explain how equivalent units for transferred-in is calculated under the First In, FirstOut (FIFO)…arrow_forward

- Problem 8-63 (Algo) Solving for Unknowns: FIFO Method (LO 8-4, 5) For each of the following independent cases, use FIFO costing to determine the information requested. Required: a) At the start of the period, 3,700 units were in the work-in-process inventory; 3,100 units were in the ending inventory. During the period, 9,600 units were transferred out to the next department. Materials and conversion costs are added evenly throughout the production process. FIFO costing is used. How many units were started during this period?b. Beginning inventory amounted to 1,100 units. This period, 4,600 units were started and completed. At the end of the period, the 3,200 units in inventory were 40 percent complete. Using FIFO costing, the equivalent production for the period was 6,100 units. What was the percentage of completion of the beginning inventory?c. The ending inventory included $81,900 for conversion costs. During the period, 41,300 equivalent units were required to complete the…arrow_forwardExercise 4-5 (Algo) Cost Reconciliation Report—Weighted-Average Method [LO4-5] Maria Am Corporation uses the weighted-average method in its process costing system. The Baking Department is one of the processing departments in its strudel manufacturing facility. In June in the Baking Department, the cost of beginning work in process inventory was $4,880, the cost of ending work in process inventory was $1,120, and the cost added to production was $25,300. Required: Prepare a cost reconciliation report for the Baking Department for June.arrow_forwardProblem 4-30 Albany Company accumulates costs for its product using process costing. Direct material is added at the beginning of the production process, and conversion activity occurs uniformly throughout the process. Production Report on image below Required: Use weighted-average process costing in completing the following requirements.1. Prepare a schedule of equivalent units.2. Compute the costs per equivalent unit.3. Compute the cost of goods completed and transferred out during August.4. Compute the cost remaining in the work-in-process inventory on August 31.5. Prepare a journal entry to record the transfer of the cost of goods completed and transferred out during August.arrow_forward

arrow_back_ios

arrow_forward_ios

Recommended textbooks for you

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781337119207Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781337119207

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Cost Accounting - Definition, Purpose, Types, How it Works?; Author: WallStreetMojo;https://www.youtube.com/watch?v=AwrwUf8vYEY;License: Standard YouTube License, CC-BY