Concept explainers

Videos

1,3, 5 and 8

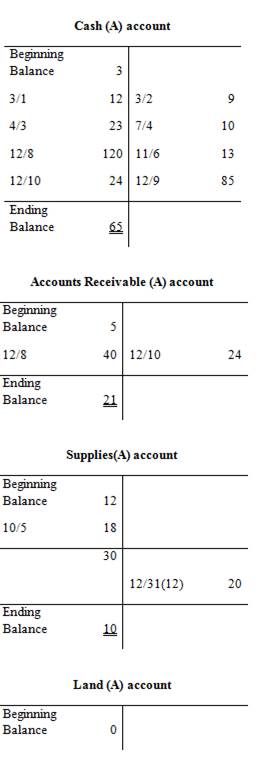

To Prepare: T-accounts for the accounts on the

1,3, 5 and 8

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability,

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

(a)The title of the account

(b)The left or debit side

(c)The right or credit side

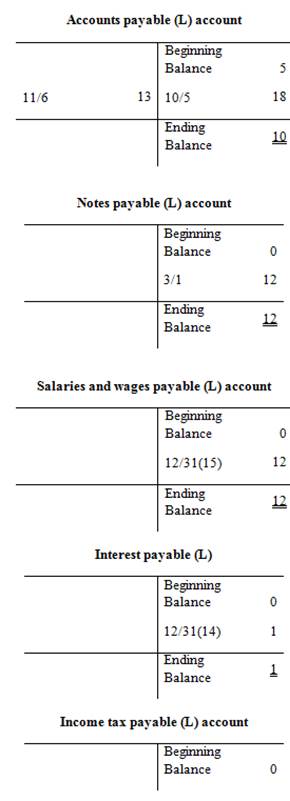

Prepare the T-account:

2.

To record:

2.

Explanation of Solution

Journal entries for the transactions (1) to (10) as follows:

| Date | Account Title and Explanation | Debit ($) | Credit ($) | ||

| 1) | Cash (+A) | 12 | |||

| Notes payable (Short-term) (+L) | 12 | ||||

| (To record borrowed cash on note) | |||||

| 2) | Land (+A) | 9 | |||

| Cash (-A) | 9 | ||||

| (To record purchase of land for building site) | |||||

| 3) | Cash (+A) | 23 | |||

| Common Stock (+SE) | 23 | ||||

| (To record issued common stock for cash) | |||||

| 4) | Software (+A) | 10 | |||

| Cash (-A) | 10 | ||||

| (To record Purchase of additional software) | |||||

| 5) | Supplies (+A) | 18 | |||

| Accounts payable (+L) | 18 | ||||

| (To record supplies purchased for future use) | |||||

| 6) | Accounts payable (-L) | 13 | |||

| Cash (-A) | 13 | ||||

| (To record cash paid to creditors) | |||||

| 7) | No entry required, Because no revenue has been earned in 2015 | ||||

| 8) | Cash (+A) | 120 | |||

| 40 | |||||

| Service Revenue (+R, +SE) | 160 | ||||

| (To record service revenue earned during the year 2015) | |||||

| 9) | Salaries and Wages Expense (+E, -SE) | 85 | |||

| Cash (-A) | 85 | ||||

| (To record salaries and wages expense incurred during 2015) | |||||

| 10) | Cash (+A) | 24 | |||

| Accounts Receivable (-A) | 24 | ||||

| (To record cash collected on customer’s account) | |||||

Table (1)

3.

To Prepare: An unadjusted trial balance from requirement 2.

3.

Explanation of Solution

| Incorporation H&H | ||

| Unadjusted Trial Balance | ||

| At December 31, 2015 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 65 | |

| Accounts Receivable | 21 | |

| Supplies | 30 | |

| Land | 9 | |

| Equipment | 60 | |

| 6 | ||

| Software | 25 | |

| Accumulated Amortization | 5 | |

| Accounts Payable | 10 | |

| Notes Payable (short–term) | 12 | |

| Salaries and Wages Payable | ||

| Interest Payable | ||

| Income Taxes Payable | ||

| Common Stock | 94 | |

| 8 | ||

| Service Revenue | 160 | |

| Salaries and Wages Expense | 85 | |

| Supplies Expense | ||

| Depreciation Expense | ||

| Interest Expense | ||

| Income Tax Expense | ||

| Total | 295 | 295 |

Table (2)

4.

To record: Adjusting journal entries (11) to (16)

4.

Explanation of Solution

Prepare adjusting journal entries (11) to (16):

| Date | Account Title and Explanation | Debit ($) | Credit ($) | ||

| 11. | Amortization Expense (+E, -SE) | 5 | |||

| Accumulated Amortization (+xA, -A) | 5 | ||||

| (To record |

|||||

| 12. | Supplies expense (+E, -SE) (1) | 20 | |||

| Supplies(-A) | 20 | ||||

| (To record the use of supplies) | |||||

| 13. | 6 | ||||

| Accumulated depreciation –Equipment (+xA, -A) | 6 | ||||

| (To record adjusting entry for depreciation expense) | |||||

| 14. | Interest expense (+E, -SE) | 1 | |||

| Interest payable(+L) | 1 | ||||

| (To record the adjusting entry for interest expense) | |||||

| 15. | Salaries and wages expense (+E, -SE) | 12 | |||

| Salaries and wages payable (+L) | 12 | ||||

| (To record the adjusting entry for salaries and wages expenses) | |||||

| 16. | Income tax expense(+E, -SE) | 8 | |||

| Income tax payable(+L) | 8 | ||||

| (To record the adjusting entry for income tax expense) | |||||

Table (3)

Working notes:

12. Calculation of supplies expenses:

5.

To Prepare: An adjusted trial balance from requirement 4.

5.

Explanation of Solution

Prepare an adjusted trial balance for Incorporation H&H for December 31, 2015:

| Incorporation H&H | ||

| Adjusted Trial Balance | ||

| At December 31, 2015 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 65 | |

| Accounts Receivable | 21 | |

| Supplies | 10 | |

| Land | 9 | |

| Equipment | 60 | |

| Accumulated Depreciation–Equipment | 12 | |

| Software | 25 | |

| Accumulated Amortization | 10 | |

| Accounts Payable | 10 | |

| Notes Payable (short–term) | 12 | |

| Salaries and Wages Payable | 12 | |

| Interest Payable | 1 | |

| Income Taxes Payable | 8 | |

| Common Stock | 94 | |

| Retained Earnings | 8 | |

| Service Revenue | 160 | |

| Salaries and Wages Expense | 97 | |

| Supplies Expense | 20 | |

| Depreciation Expense | 6 | |

| Amortization expense | 5 | |

| Interest Expense | 1 | |

| Income Tax Expense | 8 | |

| Total | 327 | 327 |

Table (4)

6.

To prepare: An income statement, Statement of retained earnings and balance sheet.

6.

Explanation of Solution

Prepare an income statement for the year ended December 31, 2015:

| Incorporation H&H | ||

| Income Statement | ||

| For the year ended December 31, 2015 | ||

| (in thousands) | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Service revenue | 160 | |

| Total revenues | 160 | |

| Less: Expenses | ||

| Salaries and wage expense | 97 | |

| Supplies expense | 20 | |

| Depreciation expense | 6 | |

| Amortization expense | 5 | |

| Interest expense | 1 | |

| Income tax expense | 8 | |

| Total expenses | 137 | |

| Net income | 23 | |

(2)

Table (5)

Prepare a statement of retained earnings:

| Incorporation H&H | ||

| Statement of Retained Earnings | ||

| For the year ended December 31, 2015 | ||

| (in thousands) | ||

| Particulars | Amount ($) | Amount ($) |

| Balance, January 1, 2015 | 8 | |

| Add: Net income | 23 | |

| 31 | ||

| Less: Dividends | (0) | |

| Balance, December 31, 2015 | 31 | |

Table (6)

Prepare a balance sheet for the year December 31, 2015:

| Incorporation H&H | ||

| Balance Sheet | ||

| At December 31, 2015 | ||

| (in thousands) | ||

| Particulars | Amount($) | Amount($) |

| Assets | ||

| Current Assets: | ||

| Cash | 65 | |

| Accounts Receivable | 21 | |

| Supplies | 10 | |

| Total current assets | 96 | |

| Land | 9 | |

| Equipment | 60 | |

| Accumulated Depreciation | (12) | |

| Equipment, net | 48 | |

| Software | 25 | |

| Accumulated amortization | (10) | 15 |

| Total Assets | 168 | |

| Liabilities : | ||

| Current liabilities : | ||

| Accounts Payable | 10 | |

| Notes payable (short-term) | 12 | |

| salaries and wages payable | 12 | |

| Interest payable | 1 | |

| Income Taxes Payable | 8 | |

| Total Current Liabilities | 43 | |

| Stockholders’ Equity | ||

| Common Stock | 94 | |

| Retained Earnings | 31 | |

| Total Stockholders’ Equity | 125 | |

| Total liabilities and stockholders’ equity | 168 |

Table (7)

7.

To prepare: The closing entry for Incorporation H&H on December 31, 2015.

7.

Explanation of Solution

Prepare closing entries for Incorporation H&H on December 31, 2015:

| Date | Account Title and Explanation | Debit ($) | Credit ($) |

| December 31, 2015 | Sales revenue(-R) | 160 | |

| Salaries and wages expense(-E) | 97 | ||

| Depreciation expense(-E) | 6 | ||

| Supplies expense(-E) | 20 | ||

| Amortization expense (-E) | 5 | ||

| Income tax expense(-E) | 8 | ||

| Interest expense (-E) | 1 | ||

| Retained earnings(+SE) (2) | 23 | ||

| (To record the closing entries for Incorporation H&H) |

Table (8)

For closing of temporary accounts, the balances of revenues, expenses, and dividend accounts will be transferred to retained earnings in order to bring zero balance for expenses and revenues accounts.

8.

To prepare: Post closing trial balance from the requirement 7.

8.

Explanation of Solution

Prepare a Post-closing trial balance for Incorporation H&H for December 31, 2015:

| Incorporation H&H | ||

| Post-closing Trial Balance | ||

| At December 31, 2015 | ||

| (in thousands) | ||

| Account Titles | Debit ($) | Credit ($) |

| Cash | 65 | |

| Accounts Receivable | 21 | |

| Supplies | 10 | |

| Land | 9 | |

| Equipment | 60 | |

| Accumulated Depreciation–Equipment | 12 | |

| Software | 25 | |

| Accumulated Amortization | 10 | |

| Accounts Payable | 10 | |

| Notes Payable (short–term) | 12 | |

| Salaries and Wages Payable | 12 | |

| Interest Payable | 1 | |

| Income Taxes Payable | 8 | |

| Common Stock | 94 | |

| Retained Earnings | 31 | |

| Dividends | 0 | |

| Service Revenue | 0 | |

| Salaries and Wages Expense | 0 | |

| Supplies Expense | 0 | |

| Depreciation Expense | 0 | |

| Amortization expense | 0 | |

| Interest Expense | 0 | |

| Income Tax Expense | 0 | |

| Total | 190 | 190 |

Table (9)

9.

To know: The net income of Incorporation H&H has been generated during 2015 and to determine the net profit margin and to explain the company has been financed primarily by liabilities or stockholders’ equity and to find the current ratio.

9.

Explanation of Solution

The net income of Incorporation H&H for 2015:

Incorporation H&H generated net income in the year 2015 is $23(thousand).

Calculation of net profit margin:

The net profit margin of Incorporation H&H is 14.4%.

To see whether the Incorporation H&H is financed primarily by liabilities or stockholders’ equity:

The Incorporation H&H is financed primarily by stockholders’ equity, where by providing stockholders’ equity for $125(thousand) with the total assets and liabilities providing for $43(thousand).

Calculation of current ratio:

The current ratio is 2.23:1.

Want to see more full solutions like this?

Chapter 4 Solutions

Access Card To Accompany Financial Accounting Niagara County Community College Acc 116 2-semester Access Phillips

- Journal entries and trial balance On August 1, 20Y7, Rafael Masey established Planet Realty, which completed the following transactions during the month: a. Rafael Masey transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 17,500. b. Purchased supplies on account, 2,300. c. Earned sales commissions, receiving cash, 13,300. d. Paid rent on office and equipment for the month, 3,000. e. Paid creditor on account, 1,150. f. Paid dividends, 1,800. g. Paid automobile expenses (including rental charge) for month, 1,500, and miscellaneous expenses, 400. h. Paid office salaries, 2,800. i. Determined that the cost of supplies used was 1,050. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Journal entry explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances, after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of August 31, 20Y7. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for August. 5. Determine the increase or decrease in retained earnings for August.arrow_forwardElite Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on March 31, 2016, follows: The following business transactions were completed by Elite Realty during April 2016: Instructions 1. Record the April 1, 2016, balance of each account in the appropriate balance column of a four-column account, write Balance in the item section, and place a check mark () in the Posting Reference column. 2. Journalize the transactions for April in a two-column journal beginning on Page 18. Journal entry explanations may be omitted. 3. Post to the ledger, extending the account balance to the appropriate balance column after each posting. 4. Prepare an unadjusted trial balance of the ledger as of April 30, 2016. 5. Assume that the April 30 transaction for salaries and commissions should have been 19,100. (a) Why did the unadjusted trial balance in (4) balance? (b) Journalize the correcting entry. (c) Is this error a transposition or slide?arrow_forwardSage Learning Centers was established on July 20, 2016, to provide educational services. The services provided during the remainder of the month are as follows: Instructions 1. Journalize the transactions for July, using a single-column revenue journal and a two-column general journal. Post to the following customer accounts in the accounts receivable ledger, and insert the balance immediately after recording each entry: D. Chase; J. Dunlop; F. Mintz; T. Quinn; K. Tisdale. 2. Post the revenue journal and the general journal to the following accounts in the general ledger, inserting the account balances only after the last postings: 3. a. What is the sum of the balances of the customer accounts in the subsidiary ledger at July 31? b. What is the balance of the accounts receivable controlling account at July 31? 4. Assume Sage Learning Centers began using a computerized accounting system to record the sales transactions on August 1. What are some of the benefits of the computerized system over the manual system?arrow_forward

- For the past several years, Steffy Lopez has operated a part-time consulting business from his home. As of July 1, 2016, Steffy decided to move to rented quarters and to operate the business, which was to be known as Diamond Consulting, on a full-time basis. Diamond Consulting entered into the following transactions during July: Instructions 1.Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) 2.Post the journal to a ledger of four-column accounts. 3.Prepare an unadjusted trial balance. 4.At the end of July, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during July is 375. b. Supplies on hand on July 31 are 1,525. c. Depreciation of office equipment for July is 750. d. Accrued receptionist salary on July 31 is 175. e. Rent expired during July is 2,400. f. Unearned fees on July 31 are 2,750. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 3 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owners equity, and a balance sheet. 9.Prepare and post the closing entries. (Income Summary is account #33 in the chart of accounts.) Record the closing entries on Page 4 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardKelly Pitney began her consulting business, Kelly Consulting, on April 1, 2018. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned fees, 4,500. 5. Received cash from clients on account, 2,450. 9. Paid cash for a newspaper advertisement, 225. 13. Paid Office Station Co. for part of the debt incurred on April 5, 640. 15. Recorded services provided on account for the period May 115, 9,180. 16. Paid part-time receptionist for two weeks salary including the amount owed on April 30, 750. 17. Recorded cash from cash clients for fees earned during the period May 1-16, 8,360. Record the following transactions on Page 6 of the journal: 20. Purchased supplies on account, 735. 21. Recorded services provided on account for the period May 16-20,4,820. 25. Recorded cash from cash clients for fees earned for the period May 17- 23, 7,900. 27. Received cash from clients on account, 9,520. 28. Paid part-time receptionist for two weeks salary, 750. 30. Paid telephone bill for May, 260. 31. Paid electricity bill for May, 810. 31. Recorded cash from cash clients for fees earned for the period May 26-31, 3,300. 31. Recorded services provided on account for the remainder of May, 2,650. 31. Paid dividends, 10,500. Instructions 1. The cl1art of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2018, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2018, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). (A) Insurance expired during May is 275. (B) Supplies on hand on May 31 are 715. (C) Depreciation of office equipment for May is 330. (D) Accrued receptionist salary on May 31 is 325. (E) Rent expired during May is 1,600. (F) Unearned fees on May 31 are 3,210. 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a retained earnings statement, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 8 of d1e journal. (Income Summary is account #34 in d1e chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10. Prepare a post-closing trial balance.arrow_forwardIn March, T. Carter established Carter Delivery Service. The account headings are presented below. Transactions completed during the month of March follow. a. Carter deposited 25,000 in a bank account in the name of the business. b. Bought a used truck from Degroot Motors for 15,140, paying 5,140 in cash and placing the remainder on account. c. Bought equipment on account from Flemming Company, 3,450. d. Paid the rent for the month, 1,000, Ck. No. 3001 (Rent Expense). e. Sold services for cash for the first half of the month, 6,927 (Service Income). f. Bought supplies for cash, 301, Ck. No. 3002. g. Bought insurance for the truck for the year, 1,200, Ck. No. 3003. h. Received and paid the bill for utilities, 349, Ck. No. 3004 (Utilities Expense). i. Received a bill for gas and oil for the truck, 218 (Gas and Oil Expense). j. Sold services on account, 3,603 (Service Income). k. Sold services for cash for the remainder of the month, 4,612 (Service Income). l. Paid wages to the employees, 3,958, Ck. Nos. 30053007 (Wages Expense). m. Carter withdrew cash for personal use, 1,250, Ck. No. 3008. Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forward

- On March 1 of this year, B. Gervais established Gervais Catering Service. The account headings are presented below. Transactions completed during the month follow. a. Gervais deposited 25,000 in a bank account in the name of the business. b. Bought a truck from Kelly Motors for 26,329, paying 8,000 in cash and placing the balance on account, Ck. No. 500. c. Bought catering equipment on account from Luigis Equipment, 3,795. d. Paid the rent for the month, 1,255, Ck. No. 501 (Rent Expense). e. Bought insurance for the truck for one year, 400, Ck. No. 502. f. Sold catering services for cash for the first half of the month, 3,012 (Catering Income). g. Bought supplies for cash, 185, Ck. No. 503. h. Sold catering services on account, 4,307 (Catering Income). i. Received and paid the heating bill, 248, Ck. No. 504 (Utilities Expense). j. Received a bill from GC Gas and Lube for gas and oil for the truck, 128 (Gas and Oil Expense). k. Sold catering services for cash for the remainder of the month, 2,649 (Catering Income). l. Gervais withdrew cash for personal use, 1,550, Ck. No. 505. m. Paid the salary of the assistant, 1,150, Ck. No. 506 (Salary Expense). Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forwardKelly Pitney began her consulting business, Kelly Consulting, on April 1, 2016. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter. During May, Kelly Consulting entered into the following transactions: Instructions 1. The chart of accounts for Kelly Consulting is shown in Exhibit 9, and the post-closing trial balance as of April 30, 2016, is shown in Exhibit 17. For each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1, 2016, and place a check mark () in the Posting Reference column. Journalize each of the May transactions in a two column journal starting on Page 5 of the journal and using Kelly Consultings chart of accounts. (Do not insert the account numbers in the journal at this time.) 2. Post the journal to a ledger of four-column accounts. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6) a. Insurance expired during May is 275. b. Supplies on hand on May 31 are 715. c. Depreciation of office equipment for May is 330. d. Accrued receptionist salary on May 31 is 325. e. Rent expired during May is 1,600. f. Unearned fees on May 31 are 3,210. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 7 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owners equity, and a balance sheet. 9.Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardOn July 1, K. Resser opened Ressers Business Services. Ressers accountant listed the following chart of accounts: The following transactions were completed during July: a. Resser deposited 25,000 in a bank account in the name of the business. b. Bought tables and chairs for cash, 725, Ck. No. 1200. c. Paid the rent for the current month, 1,750, Ck. No. 1201. d. Bought computers and copy machines from Ferber Equipment, 15,700, paying 4,000 in cash and placing the balance on account, Ck. No. 1202. e. Bought supplies on account from Wigginss Distributors, 535. f. Sold services for cash, 1,742. g. Bought insurance for one year, 1,375, Ck. No. 1203. h. Paid on account to Ferber Equipment, 700, Ck. No. 1204. i. Received and paid the electric bill, 438, Ck. No. 1205. j. Paid on account to Wigginss Distributors, 315, Ck. No. 1206. k. Sold services to customers for cash for the second half of the month, 820. l. Received and paid the bill for the business license, 75, Ck. No. 1207. m. Paid wages to an employee, 1,200, Ck. No. 1208. n. Resser withdrew cash for personal use, 700, Ck. No. 1209. Required 1. Record the owners name in the Capital and Drawing T accounts. 2. Correctly place the plus and minus signs for each T account and label the debit and credit sides of the accounts. 3. Record the transactions in the T accounts. Write the letter of each entry to identify the transaction. 4. Foot the T accounts and show the balances. 5. Prepare a trial balance as of July 31, 20--. 6. Prepare an income statement for July 31, 20--. 7. Prepare a statement of owners equity for July 31, 20--. 8. Prepare a balance sheet as of July 31, 20--. LO 1, 2, 3, 4, 5, 6arrow_forward

- For the past several years, Jeff Horton has operated a part-time consulting business from his home. As of April 1, 2016, Jeff decided to move to rented quarters and to operate the business, which was to be known as Rosebud Consulting, on a full-time basis. Rosebud Consulting entered into the following transactions during April: Instructions 1.Journalize each transaction in a two-column journal starting on Page 1, referring to the following chart of accounts in selecting the accounts to be debited and credited. (Do not insert the account numbers in the journal at this time.) 2.Post the journal to a ledger of four-column accounts. 3.Prepare an unadjusted trial balance. 4.At the end of April, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6). a. Insurance expired during April is 350. b. Supplies on hand on April 30 are 1,225. c. Depreciation of office equipment for April is 400. d. Accrued receptionist salary on April 30 is 275. e. Rent expired during April is 2,000. f. Unearned fees on April 30 are 2,350. 5.(Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. 6.Journalize and post the adjusting entries. Record the adjusting entries on Page 3 of the journal. 7.Prepare an adjusted trial balance. 8.Prepare an income statement, a statement of owners equity, and a balance sheet. 9.Prepare and post the closing entries. Record the closing entries on Page 4 of the journal. (Income Summary is account #33 in the chart of accounts.) Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry. 10.Prepare a post-closing trial balance.arrow_forwardOn March 1 of this year, B. Gervais established Gervais Catering Service. The account headings are presented below. Transactions completed during the month follow. a. Gervais deposited 25,000 in a bank account in the name of the business. b. Bought a truck from Kelly Motors for 26,329, paying 8,000 in cash and placing the balance on account, Ck. No. 500. c. Bought catering equipment on account from Luigis Equipment, 3,795. d. Paid the rent for the month, 1,255, Ck. No. 501. e. Bought insurance for the truck for one year, 400, Ck. No. 502. f. Sold catering services for cash for the first half of the month, 3,012. g. Bought supplies for cash, 185, Ck. No. 503. h. Sold catering services on account, 4,307. i. Received and paid the heating bill, 248, Ck. No. 504. j. Received a bill from GC Gas and Lube for gas and oil for the truck, 128. k. Sold catering services for cash for the remainder of the month, 2,649. l. Gervais withdrew cash for personal use, 1,550, Ck. No. 505. m. Paid the salary of the assistant, 1,150, Ck. No. 506. Required 1. Record the transactions and the balance after each transaction. 2. Total the left side of the accounting equation (left side of the equal sign), then total the right side of the accounting equation (right side of the equal sign). If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forwardEFFECTS OF TRANSACTIONS (BALANCE SHEET ACCOUNTS) Jon Wallace started a business. During the first month (March 20--), the following transactions occurred. Show the effect of each transaction on the accounting equation: Assets= Liabilities + Owners Equity. After each transaction, show the new account totals. (a) Invested cash in the business, 30,000. (b) Bought office equipment on account, 4,500. (c) Bought office equipment for cash, 1,600. (d) Paid cash on account to supplier in transaction (b), 2,000. EFFECTS OF TRANSACTIONS (REVENUE, EXPENSE, WITHDRAWALS) This exercise is an extension of Exercise 2-3B. Lets assume Jon Wallace completed the following additional transactions during March. Show the effect of each transaction on the basic elements of the expanded accounting equation: Assets = Liabilities + Owners Equity (Capital Drawing + Revenues Expenses). After transaction (k), report the totals for each element. Demonstrate that the accounting equation has remained in balance. (e) Performed services and received cash, 3,000. (f) Paid rent for March, 1,000. (g) Paid March phone bill, 68. (h) Jon Wallace withdrew cash for personal use, 800. (i) Performed services for clients on account, 900. (j) Paid wages to part-time employee, 500. (k) Received cash for services performed on account in transaction (i), 500.arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning