Concept explainers

Videos

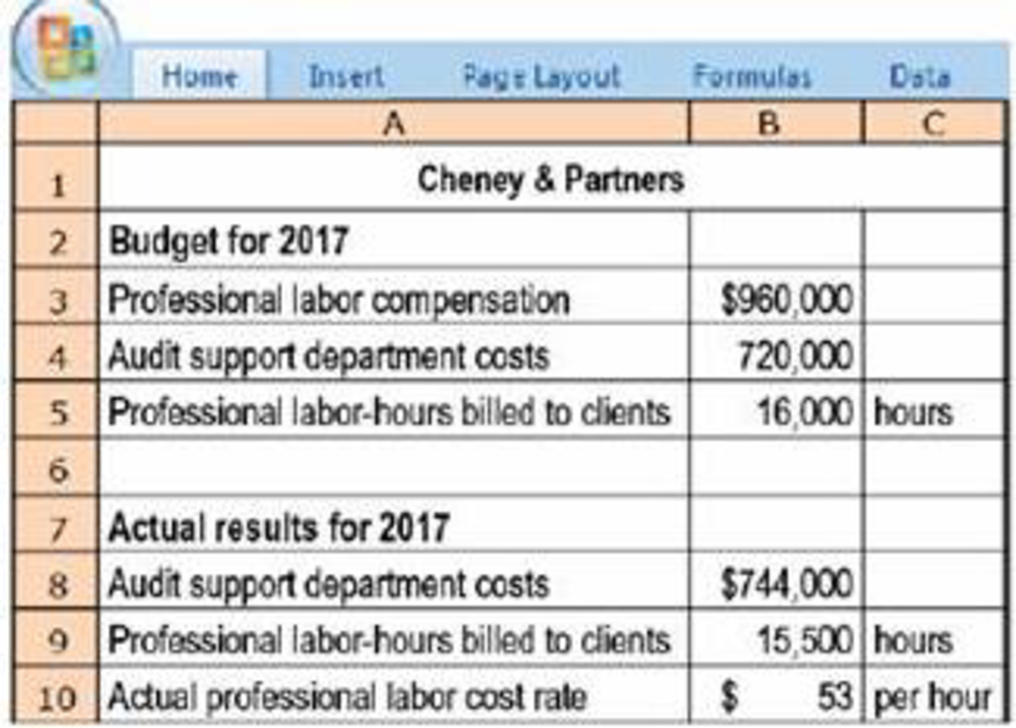

Budgeted and actual amounts for 2017 are as follows:

- 1. Compute the direct-cost rate and the indirect-cost rate per professional labor-hour for 2017 under (a) actual costing, (b) normal costing, and (c) the variation from normal costing that uses budgeted rates for direct costs.

Required

- 2. Which job-costing system would you recommend Cheney & Partners use? Explain.

- 3. Cheney’s 2017 audit of Pierre & Co. was budgeted to take 170 hours of professional labor time. The actual professional labor time spent on the audit was 185 hours. Compute the cost of the Pierre & Co. audit using (a) actual costing, (b) normal costing, and (c) the variation from normal costing that uses budgeted rates for direct costs. Explain any differences in the job cost.

Learn your wayIncludes step-by-step video

Chapter 4 Solutions

HORGREN'S COST ACCOUNTING

Additional Business Textbook Solutions

Horngren's Accounting (12th Edition)

Horngren's Accounting (11th Edition)

Intermediate Accounting (2nd Edition)

Construction Accounting And Financial Management (4th Edition)

Financial Accounting

Principles of Accounting Volume 2

- A manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardCynthia Rogers, the cost accountant for Sanford Manufacturing, is preparing a management report that must include an allocation of overhead. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, and allocating overhead on the basis of direct labor hours, overhead applied to Job 231 in the Tooling Department would be: a. 44.00. b. 197.50. c. 241.50. d. 501.00.arrow_forwardThe following describes the job responsibilities of two employees of Barney Manufacturing. Joan Dennison, Cost Accounting Manager. Joan is responsible for measuring and collecting costs associated with the manufacture of the garden hose product line. She is also responsible for preparing periodic reports that compare the actual costs with planned costs. These reports are provided to the production line managers and the plant manager. Joan helps to explain and interpret the reports. Steven Swasey, Production Manager. Steven is responsible for the manufacture of the high-quality garden hose. He supervises the line workers, helps to develop the production schedule, and is responsible for seeing that production quotas are met. He is also held accountable for controlling manufacturing costs. Required: CONCEPTUAL CONNECTION Identify Joan and Steven as line or staff and explain your reasons.arrow_forward

- San Mateo Optics, Inc., specializes in manufacturing lenses for large telescopes and cameras used in space exploration. As the specifications for the lenses are determined by the customer and vary considerably, the company uses a job-order costing system. Manufacturing overhead is applied to jobs on the basis of direct labor hours, utilizing the absorption- or full-costing method. San Mateos predetermined overhead rates for 20x1 and 20x2 were based on the following estimates. Jim Cimino, San Mateos controller, would like to use variable (direct) costing for internal reporting purposes as he believes statements prepared using variable costing are more appropriate for making product decisions. In order to explain the benefits of variable costing to the other members of San Mateos management team, Cimino plans to convert the companys income statement from absorption costing to variable costing. He has gathered the following information for this purpose, along with a copy of San Mateos 20x1 and 20x2 comparative income statement. San Mateo Optics, Inc. Comparative Income Statement For the Years 20x1 and 20x2 San Mateos actual manufacturing data for the two years are as follows: The companys actual inventory balances were as follows: For both years, all administrative expenses were fixed, while a portion of the selling expenses resulting from an 8 percent commission on net sales was variable. San Mateo reports any over-or underapplied overhead as an adjustment to the cost of goods sold. Required: 1. For the year ended December 31, 20x2, prepare the revised income statement for San Mateo Optics, Inc., utilizing the variable-costing method. Be sure to include the contribution margin on the revised income statement. 2. Describe two advantages of using variable costing rather than absorption costing. (CMA adapted)arrow_forwardThe law firm END, LLP provides legal services to a wide range of clients in the KC area. The firm has two main costs: (1) compensation for professional staff and (2) all other costs, which include support staff, facilities costs, and other costs. The costs of professional staff are considered direct costs for the purposes of billing clients and assessing the profitability of each client job; all other costs are considered overhead. The firm determines an overhead rate for client billing based on the number of professional staff hours used for the job. Professional staff are paid $150 per hour and their time is billed at $250 per hour. The firm estimates the following total costs for the coming year: Estimated cost of professional staff $ 6,000,000 (40,000 hours of staff time = $150/hr) Estimated other costs (overhead) 5,000,000 Total estimated costs $11,000,000 Required: Prepare a case analysis that computes the…arrow_forwardJansen Corp. has decided to implement an activity-based costing system for its in-house legal department. The legal department’s primary expense is professional salaries, which are estimated for associated activities as follows: Reviewing supplier or customer contracts (Contracts) P270,000 Reviewing regulatory compliance issues (Regulation) 375,000 Court actions (Court) 862,500 Management has determined that the appropriate cost allocation base for Contracts is the number of pages in the contract reviewed, for Regulation is the number of reviews, and for Court is number of hours of court time. For 2010, the legal department reviewed 450,000 pages of contracts, responded to 750 regulatory review requests, and logged 3,750 hours in court. How can the developed rates be used for evaluating output relative to cost incurred in the legal department? What alternative does the firm have to maintaining an internal legal department and how might this choice affect costs?arrow_forward

- Jansen Corp. has decided to implement an activity-based costing system for its in-house legal department. The legal department’s primary expense is professional salaries, which are estimated for associated activities as follows: Reviewing supplier or customer contracts (Contracts) P270,000 Reviewing regulatory compliance issues (Regulation) 375,000 Court actions (Court) 862,500 Management has determined that the appropriate cost allocation base for Contracts is the number of pages in the contract reviewed, for Regulation is the number of reviews, and for Court is number of hours of court time. For 2010, the legal department reviewed 450,000 pages of contracts, responded to 750 regulatory review requests, and logged 3,750 hours in court. Determine the allocation rate for each activity in the legal department. What amount would be charged to a producing department that had 21,000 pages of contracts reviewed, made 27 regulatory review requests, and consumed 315 professional hours…arrow_forwardKumar, Inc., evaluates managers of producing departments on their ability to control costs. In addition to the costs directly traceable to their departments, each production manager is held responsible for a share of the costs of a support center, the human resources (HR) department. The total costs of HR are allocated on the basis of actual direct labor hours used. The total costs of HR and the actual direct labor hours worked by each producing department are as follows: Year 1 Year 2 Direct labor hours worked: Department A 24,000 25,000 Department B 36,000 25,000 Total hours 60,000…arrow_forwardKeating& Associates is a law firm specializing in labor relations employee-related work. Keating & Associates received feedback from Punch, Inc., that its bid for the labor contract work was too high. This feedback prompted Keating to review its work activities and how they are reflected in its job-costing system. The review included the detailed analysis of how past jobs used the firm’s resources and interviews with personnel about what factors drive the level of indirect costs. Management concluded that a system with two direct-cost categories (professional partner labor and professional associate labor) and two indirect-cost categories (general support and secretarial support) would yield more accurate job costs. Budgeted information for 2016 related to two direct cost categories is as follows: Professional Professional Partner labor…arrow_forward

- Assigning Overhead to Jobs—Ethical Issues Tonya Martin, CMA and controller of the Parts Division of Gunderson Inc., was meeting with Doug Adams, manager of the division. The topic of discussion was the assignment of overhead costs to jobs and their impact on the division's pricing decisions. Their conversation was as follows: Tonya: Doug, as you know, about 25% of our business is based on government contracts, with the other 75% based on jobs from private sources won through bidding. During the last several years, our private business has declined. We have been losing more bids than usual. After some careful investigation, I have concluded that we are overpricing some jobs because of improper assignment of overhead costs. Some jobs are also being underpriced. Unfortunately, the jobs being overpriced are coming from our higher-volume, labor-intensive products, so we are losing business. Doug: I think I understand. Jobs associated with our high-volume products are being assigned more…arrow_forwardJob costing, journal entries. The University of Chicago Press is wholly owned by the university. It performs the bulk of its work for other university departments, which pay as though the press were an outside business enterprise. The press also publishes and maintains a stock of books for general sale. The press uses normal costing to cost each job. Its job-costing system has two direct-cost categories (direct materials and direct manufacturing labor) and one indirect-cost pool (manufacturing overhead, allocated on the basis of direct manufacturing labor costs).arrow_forwardKLP provides consulting services and uses a job-order system to accumulate the cost of client projects. Traceable costs are charged directly to individual clients; in contrast, other costs incurred by KLP, but not identifiable with specific clients, are charged to jobs by using a predetermined overhead application rate. Clients are billed for directly chargeable costs, overhead, and a markup. KLP anticipates the following costs for the upcoming year: KLP's partners desire to make a $480,000 profit for the firm and plan to add a percentage markup on total cost to achieve that figure.On May 14, KLP completed work on a project for Lawson Manufacturing. The following costs were incurred: professional staff salaries, $68,000; administrative support staff, $8,900; travel, $10,500; and other operating costs, $2,600.REQUIRED:(a) Determine KLP's total traceable costs for the upcoming year and the firm's total anticipated overhead.(b) Calculate the predetermined overhead rate. The…arrow_forward

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,