Concept explainers

Videos

T accounts,

The unadjusted

| Epicenter Laundry Unadjusted Trial Balance June 30,2019 |

||

| Debit Balances | Credit Balances | |

| Cash | 11,000 | |

| Laundry Supplies | 21,500 | |

| Prepaid Insurance | 9,600 | |

| Laundry Equipment | 232,600 | |

| 125,400 | ||

| Accounts Payable | 11,800 | |

| Sophie Perez, Capital | 105,600 | |

| Sophie Perez, Drawing | 10,000 | |

| Laundry Revenue | 232,200 | |

| Wages Expense | 125,200 | |

| Rent Expense | 40,000 | |

| Utilities Expense | 19,700 | |

| Miscellaneous Expense | 5,400 | |

| 475,000 | 475,000 | |

The data needed to determine year-end adjustments are as follows:

a. Laundry supplies on hand at June 30 are $3,600.

b. Insurance premiums expired during the year are $5,700.

c. Depreciation of laundry equipment during the year is $6,500.

d. Wages accrued but not paid at June 30 are $1,100.

Instructions

1. For each account listed in the unadjusted trial balance, enter the balance in a T account. Identify the balance as "June 30 Bal." In addition, add T accounts for Wages Payable, Depreciation Expense, Laundry Supplies Expense, and Insurance Expense.

2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (1) as needed.

3. Journalize and post the adjusting entries. Identify the adjustments as "Adj." and the new balances as "Adj. Bal."

4. Prepare an adjusted trial balance.

5. Prepare an income statement, a statement of owner's equity (no additional investments were made during the year), and a balance sheet.

6. Journalize and

7. Prepare a post-closing trial balance.

1, 3, and 6:

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

Ø The title of accounts.

Ø The debit side (Dr) and,

Ø The credit side (Cr).

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Statement of owners’ equity:

This statement reports the beginning owner’s equity and all the changes, which led to ending owners’ equity. Additional capital, net income from income statement is added to and drawing is deducted from beginning owner’s equity to arrive at the end result, ending owner’s equity.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

To prepare: The T-accounts.

Explanation of Solution

Record the transactions directly in their respective T-accounts, and determine their balances.

| Cash | |||||||||||

| June 30 | Balance | 11,000 | |||||||||

| Laundry Supplies | |||||||||||

| June 30 | Balance | 21,500 | June 30 | Adjusted | 17,900 | ||||||

| June 30 | Adjusted balance | 3,600 | |||||||||

| Prepaid Insurance | |||||||||||

| June 30 | Balance | 9,600 | June 30 | Adjusted | 5,700 | ||||||

| Adjusted balance | 3,900 | ||||||||||

| Laundry Equipment | |||||||||||

| June 30 | Balance | 232,600 | |||||||||

| Accumulated Depreciation | |||||||||||

| June 30 | Balance | 125,400 | |||||||||

| June 30 | Adjusted | 6,500 | |||||||||

| June 30 | Adjusted balance | 131,900 | |||||||||

| Accounts Payable | |||||||||||

| June 30 | Balance | 11,800 | |||||||||

| Wages Payable | |||||||||||

| June 30 | Adjusted | 1,100 | |||||||||

| SP, Capital | |||||||||||

| June 30 | Closing | 10,000 | June 30 | Balance | 105,600 | ||||||

| June 30 | Closing | 10,700 | |||||||||

| June 30 | Balance | 106,300 | |||||||||

| SP, Drawing | |||||||||||

| June 30 | Balance | 10,000 | June 30 | Closing | 10,000 | ||||||

| Laundry Revenue | |||||||||||

| June 30 | Closing | 232,200 | June 30 | Balance | 232,200 | ||||||

| Wages Expense | |||||||||||

| June 30 | Balance | 125,200 | June 30 | Closing | 126,300 | ||||||

| June 30 | Adjusted | 1,100 | |||||||||

| June 30 | Adjusted balance | 126,300 | |||||||||

| Rent Expense | |||||||||||

| June 30 | Balance | 40,000 | June 30 | Closing | 40,000 | ||||||

| Utilities Expense | |||||||||||

| June 30 | Balance | 19,700 | June 30 | Closing | 19,700 | ||||||

| Depreciation Expense | |||||||||||

| June 30 | Adjusted | 6,500 | June 30 | Closing | 6,500 | ||||||

| Laundry Supplies Expense | |||||||||||

| June 30 | Adjusted | 17,900 | June 30 | Closing | 17,900 | ||||||

| Insurance Expense | |||||||||||

| June 30 | Adjusted | 5,700 | June 30 | Closing | 5,700 | ||||||

| Miscellaneous Expense | |||||||||||

| June 30 | Balance | 5,400 | June 30 | Closing | 5,400 | ||||||

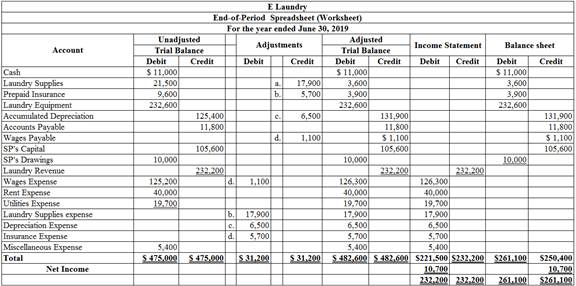

2.

To enter: The unadjusted trial balance on an end-of-period spreadsheet, and complete the spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (1)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

3.

To Journalize and post: The adjusting entries.

Explanation of Solution

The adjusting entries are journalized as follows:

| Date | Description | Debit ($) | Credit ($) | |

| 2019 | Wages expense | 1,100 | ||

| June | 30 | Wages payable | 1,100 | |

| (To record the wages accrued) | ||||

Table (2)

Explanation:

- Wages expense is an expense account, and it is increased. Hence, debit the wages expense account by $1,100.

- Wages payable is a liability account, and it is increased. Hence, credit the wages payable account by $1,100.

| Date | Description | Debit ($) | Credit ($) | |

| 2019 | Depreciation expense | 6,500 | ||

| June | 30 | Accumulated depreciation | 6,500 | |

| (To record the equipment depreciation) | ||||

Table (3)

Explanation:

- Depreciation expense is an expense account, and it is increased. Hence, debit the wages expense account by $6,500.

- Accumulated depreciation is a contra asset account, and it is increased. Hence, credit the accumulated depreciation account by $6,500.

| Date | Description | Debit ($) | Credit ($) | |

| 2019 | Laundry supplies expense | 17,900 | ||

| June | 30 |

Laundry supplies

| 17,900 | |

| (To record the equipment depreciation) | ||||

Table (4)

Explanation:

- Laundry supplies expense is an expense account, and it is increased. Hence, debit the laundry supplies expense account by $17,900.

- Laundry supplies are the asset account, and it is increased. Hence, credit the laundry supplies account by $17,900.

| Date | Description | Debit ($) | Credit ($) | |

| 2019 | Insurance expense | 5,700 | ||

| August | 31 | Prepaid insurance | 5,700 | |

| (To record the equipment depreciation) | ||||

Table (5)

Explanation:

- Insurance expense is an expense account, and it is increased. Hence, debit the insurance expense account by $5,700.

- Prepaid insurance is an asset account, and it is decreased. Hence, credit the prepaid insurance account by $5,700.

4.

To prepare: An unadjusted trial balance for Laundry E, as of June 30, 2019.

Explanation of Solution

Prepare an unadjusted trial balance for Laundry E, as of June 30, 2019.

| Laundry E | ||

| Unadjusted Trial Balance | ||

| June 30, 2019 | ||

| Accounts | Debit Balances | Credit Balances |

| Cash | 11,000 | |

| Laundry Supplies | 3,600 | |

| Prepaid Insurance | 3,900 | |

| Laundry Equipment | 232,600 | |

| Accumulated depreciation | 131,900 | |

| Accounts payable | 11,800 | |

| Wages Payable | 1,100 | |

| SP, Capital | 105,600 | |

| SP, Drawing | 10,000 | |

| Laundry revenue | 232,200 | |

| Wages expense | 126,300 | |

| Rent expense | 40,000 | |

| Utilities Expense | 19,700 | |

| Depreciation Expense | 17,900 | |

| Laundry supplies expense | 6,500 | |

| Insurance Expense | 5,700 | |

| Miscellaneous Expense | 5,400 | |

| 482,600 | 482,600 | |

Table (6)

5.

Explanation of Solution

The net income of Laundry E for the month of June is $10,700.

| E Laundry | ||

| Income Statement | ||

| For the year ended June 30, 2019 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenue: | ||

| Laundry revenue | $248,000 | |

| Expenses: | ||

| Wages Expense | $126,300 | |

| Rent Expense | 40,000 | |

| Utilities Expense | 19,700 | |

| Depreciation Expense | 17,900 | |

| Laundry supplies Expense | 6,500 | |

| Insurance Expense | 5,700 | |

| Miscellaneous Expense | 5,400 | |

| Total Expenses | 221,500 | |

| Net Income | $10,700 | |

Table (7)

Hence, the net income of Laundry E for the year ended June 30, 2019 is $10,700.

6.

To Journalize: The closing entries for E Laundry.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 30, 2019 | Laundry Revenue | 232,200 | ||

| Wages Expense | 126,300 | |||

| Rent Expense | 40,000 | |||

| Utilities Expense | 19,700 | |||

| Depreciation Expense | 17,900 | |||

| Laundry supplies Expense | 6,500 | |||

| Insurance Expense | 5,700 | |||

| Miscellaneous Expense | 5,400 | |||

| SP, Capital | 10,700 | |||

| (To close the revenues and expenses account. Then the balance amount are transferred to owners’ capital account) | ||||

| June 30 | SP’s Capital | 10,000 | ||

| SP’ Drawing | 10,000 | |||

| (To Close the capital and drawings account) | ||||

Table (10)

Explanation:

- Laundry revenue is revenue account. Since the amount of revenue is closed, and transferred to SP’s capital account. Here, E Laundry earned an income of $232,200. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expense, Laundry Supplies Expense, Depreciation Expense, SP Capital, and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

- Owner’s capital is a component of owner’s equity. Thus, owners ‘equity is debited since the capital is decreased on owners’ drawings.

- Owner’s drawings are a component of owner’s equity. It is credited because the balance of owners’ drawing account is transferred to owners ‘capital account

7.

To prepare: The post–closing trial balance of E Laundry for the month ended June 30, 2019.

Explanation of Solution

Prepare a post–closing trial balance of E Laundry for the month ended June 30, 2019 as follows:

|

Laundry E Post-closing Trial Balance June 30, 2019 | ||

| Particulars | Debit $ | Credit $ |

| Cash | 11,000 | |

| Laundry Supplies | 3,600 | |

| Prepaid insurance | 3,900 | |

| Laundry Equipment | 232,600 | |

| Accumulated depreciation | 131,900 | |

| Accounts payable | 11,800 | |

| Wages payable | 1,100 | |

| BD’s Capital | 106,300 | |

| Total | 251,100 | 251,100 |

Table (11)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $251,100.

Want to see more full solutions like this?

Chapter 4 Solutions

Cengagenow?v2, 1 Term Printed Access Card For Warren/reeve/duchac?s Accounting, 27th

- T accounts, adjusting entries, financial statements, and closing entries; optional end-of-period spreadsheet The unadjusted trial balance of Epicenter Laundry at June 30, 20Y6, the end of the fiscal year, follows: The data needed to determine year-end adjustments are as follows: (a) Laundry supplies on hand at June 30 are 8,600. (b) Insurance premiums expired during the year are 5,700. (c) Depreciation of laundry equipment during the year is 6,500. (d) Wages accrued but not paid at June 30 are 1,100. Instructions 1. For each account listed in the unadjusted trial balance, enter the balance in a T account. Identify the balance as June 30 Bal. In addition, add T accounts for Wages Payable, Depreciation Expense, Laundry Supplies Expense, and Insurance Expense. 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (1) as needed. 3. Journalize and post the adjusting entries. Identify the adjustments by Adj. and the new balances as Adj. Bal. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a statement of stockholders equity, and a balance sheet. During the year ended June 30, 20Y6, additional common stock of 7,500 was issued. 6. Journalize and post the closing entries. Identify the closing entries by Clos. 7. Prepare a post-closing trial balance.arrow_forwardT accounts, adjusting entries, financial statements, and closing entries; optional end-of-period spreadsheet The unadjusted trial balance of La Mesa Laundry at August 31, 20Y5, the end of the fiscal year, follows: The data needed to determine year-end adjustments are as follows: (a) Wages accrued but not paid at August 31 are 2,200. (b) Depreciation of equipment during the year is 8,150. (c) Laundry supplies on hand at August 31 are 2,000. (d) Insurance premiums expired during the year are 5,300. Instructions 1. For each account listed in the unadjusted trial balance, enter the balance in a T account. Identify the balance as Aug. 31 Bal. In addition, add T accounts for Wages Payable, Depreciation Expense, Laundry Supplies Expense, and Insurance Expense. 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (1) as needed. 3. Journalize and post the adjusting entries. Identify the adjustments by Adj. and the new balances as Adj. Bal. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a statement of stockholders equity, and a balance sheet. During the year ended August 31, 20Y5, common stock of 3,000 was issued. 6. Journalize and post the closing entries. Identify the closing entries by Clos. 7. Prepare a post-closing trial balance.arrow_forwardThe unadjusted trial balance of PS Music as of July 31, 2018, along with the adjustment data for the two months ended July 31, 2018, are shown in Chapter 3. Based upon the adjustment data, the following adjusted trial balance was prepared: PS Music Adjusted Trial Balance July 31, 2018 Account No. Debit Balances Credit Balances Cash................................................. 11 9,945 Accounts Receivable................................... 12 4,150 Supplies.............................................. 14 275 Prepaid Insurance..................................... 15 2,475 Office Equipment..................................... 17 7,500 Accumulated DepreciationOffice Equipment.......... 18 50 Accounts Payable..................................... 21 8,350 Wages Payable........................................ 22 140 Unearned Revenue.................................... 23 3,600 Common Stock....................................... 31 9,000 Dividends............................................ 33 1,750 Fees Earned........................................... 41 21,200 Music Expense........................................ 54 3,610 Wages Expense....................................... 50 2,940 Office Rent Expense................................... 51 2,550 Advertising Expense................................... 55 1,500 Equipment Rent Expense.............................. 52 1,375 Utilities Expense...................................... 53 1,215 Supplies Expense...................................... 56 925 Insurance Expense.................................... 57 225 Depreciation Expense................................. 58 50 Miscellaneous Expense................................ 59 1,855 42,340 42,340 Instructions 1. (Optional) Using the data from Chapter 3, prepare an end-of-period spreadsheet. 2. Prepare an income statement, a retained earnings statement, and a balance sheet. 3. Journalize and post the closing entries. The retained earnings account is #33 and the income summary account is #34 in the ledger of PS Music. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 4. Prepare a post-dosing trial balance.arrow_forward

- Prepare journal entries to record the business transaction and related adjusting entry for the following: A. March 1, paid cash for one year premium on insurance contract, $18,000 B. December 31, remaining unexpired balance of insurance, $3,000arrow_forwardWorksheet Victoria Company has the following account balances on December 31, 2019, prior to any adjustments: Additional adjustment information: (a) depreciation on buildings, 1,100; on equipment, 600; (b) bad debts expense, 240; (c) interest accumulated but not paid: on note payable, 50; on mortgage payable, 530 (this interest is due during the next accounting period); (d) insurance expired, 175; (e) salaries accrued but not paid 370; (f) rent was collected in advance and the performance obligation is now satisfied, 800; (g) office supplies cm hand at year-end, 230 (expensed when originally purchased earlier in the year); and (h) the income tax rate is 30% on current income and is payable in the first quarter of 2020. Required: 1. Transfer the account balances to a 10-column worksheet and prepare a trial balance. 2. Prepare the adjusting entries in the general journal and complete the worksheet. 3. Prepare the companys income statement, retained earnings statement, and balance sheet. 4. Prepare closing entries in the general journal.arrow_forwardLedger accounts, adjusting entries, financial statements, and closing entries; optional end-of-period spreadsheet The unadjusted trial balance of Recessive Interiors at January 31, 20Y2, the end of the year, follows: The data needed to determine year-end adjustments are as follows: (a) Supplies on hand at January 31 are 2,850. (b) Insurance premiums expired during the year are 3,150. (c) Depreciation of equipment during the year is 5,250. (d) Depreciation of trucks during the year is 4,000. (e) Wages accrued but not paid at January 31 are 900. Instructions 1. For each account listed in the unadjusted trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark () in the Posting Reference column. 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed. 3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Recessive Interiors chart of accounts should be used: Wages Payable, 22; Depreciation Expense Equipment, 54; Supplies Expense, 55; Depreciation ExpenseTrucks, 56; Insurance Expense, 57. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a statement of stockholders equity, and a balance sheet. During the year ended January 31, 20Y2, additional common stock of 7,500 was issued. 6. Journalize and post the closing entries. Record the closing entries on Page 27 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 7. Prepare a post-closing trial balance.arrow_forward

- Prepare journal entries to record the following business transaction and related adjusting entry. A. January 12, purchased supplies for cash, to be used all year, $3,850 B. December 31, physical count of remaining supplies, $800arrow_forwardBalance Sheet without Amounts The following is an alphabetical list of all of While Limnology Companys adjusted trial balance accounts as of December 31, 2019: Required: Prepare White Limnologys balance sheet (without amounts) in proper format.arrow_forwardLedger accounts, adjusting entries, financial statements, and closing entries; optional spreadsheet The unadjusted trial balance of Lakota Freight Co. at March 31, 20Y4, the end of the year, follows: The data needed to determine year-end adjustments are as follows: (a) Supplies on hand at March 31 are 7,500. (b) Insurance premiums expired during year are 1,800. (c) Depreciation of equipment during year is 8,350. (d) Depreciation of trucks during year is 6,200. (e) Wages accrued but not paid at March 31 are 600. Instructions 1. For each account listed in the trial balance, enter the balance in the appropriate Balance column of a four-column account and place a check mark () in the Posting Reference column. 2. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet. Add the accounts listed in part (3) as needed. 3. Journalize and post the adjusting entries, inserting balances in the accounts affected. Record the adjusting entries on Page 26 of the journal. The following additional accounts from Lakota Freight Co.s chart of accounts should be used: Wages Payable, 22; Supplies Expense, 52; Depreciation ExpenseEquipment, 55; Depreciation ExpenseTrucks, 56; Insurance Expense, 57. 4. Prepare an adjusted trial balance. 5. Prepare an income statement, a statement of stockholders equity, and a balance sheet. During the year ended March 31, 20Y4, additional common stock of 6,000 was issued. 6. Journalize and post the closing entries. Record the closing entries on Page 27 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. 7. Prepare a post-closing trial balance.arrow_forward

- WORK SHEET, ADJUSTING, CLOSING, AND REVERSING ENTRIES Vickis Fabric Store shows the trial balance on page 603 as of December 31, 20-1. At the end of the year, the following adjustments need to be made: (a and b)Merchandise inventory as of December 31, 31,600. (c)Unused supplies on hand, 1,150. (d)Insurance expired, 350. (e)Depreciation expense for the year; 700. (f)Wages earned but not paid (Wages Payable), 520. (g)Unearned revenue on December 31, 20-1, 1,200. REQUIRED 1. Prepare a work sheet. 2. Prepare adjusting entries. 3. Prepare closing entries. 4. Prepare a post-closing trial balance. 5. Prepare reversing entry(ies).arrow_forwardOffice Supplies Somerville Corp. purchases office supplies once a month and prepares monthly financial statements. The asset account Office Supplies on Hand has a balance of $1,450 on May 1. Purchases of supplies during May amount to $1,100. Supplies on hand at May 31 amount to $920. Prepare the necessary adjusting entry on Somervilles books on May 31. What will be the effect on net income for May if this entry is not recorded?arrow_forwardThe trial balance for Wilson Financial Services on January 31 is as follows: Data for month-end adjustments are as follows: a. Expired or used-up insurance, 750. b. Depreciation expense on equipment, 300. c. Wages accrued or earned since the last payday, 1,055 (owed and to be paid on the next payday). d. Supplies used, 535. Required 1. Complete a work sheet for the month. (Skip this step if using CLGL.) 2. Journalize the adjusting entries. 3. If using CLGL, prepare an adjusted trial balance. 4. Prepare an income statement, a statement of owners equity, and a balance sheet. Assume that no additional investments were made during January.arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning