Concept explainers

Videos

Identifying terms in ABC and ABM

Use the following terms to complete the sentences that follows; terms may be used once, more than once, or not at all.

Activity proportion

Activity rate

Activity-based management (ABM)

Batch-level

Cost-plus pricing

External failure costs

First

Inspection costs

Internal failure costs

Non-value-added

Non-volume-based

Product level

Second

Target costing

Third

Total costs

Total quality management (TQM)

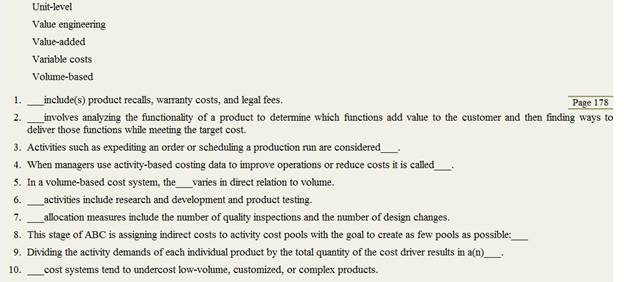

Unit-level

Value engineering

Value-added

Variable costs

Volume-based

1. ___ include(s) product recalls, warranty costs, and legal fees.

2. ___ involves the functionality of a product to determine which functions add value to the customer and then finding ways to deliver those functions while meeting the target cost.

3. Activities such as expediting an order or scheduling a production run are considered ___.

4. ___ When managers use activity-based costing data to improve operations or reduce costs it is called____.

5. ___In a volume-based cost system, the ___varies in direct relation to volume.

6. ___ activities include research and testing development and product testing.

7. ____allocation measures include the number of quality inspections and the number of design changes.

8. ___ This stage of ABC is assigning indirect costs to activity cost pools with the goal to create as few poos as possible.

9. Dividing the activity demands of each product by the total quantity of the cost driver results in a(n)___.

10. ___ cost systems tend to undercost low-volume, customized, or complex products.

Trending nowThis is a popular solution!

Chapter 4 Solutions

Connect 1-Semester Access Card for Managerial Accounting

- Activity-based management includes both process value analysis and activity-based costing. Which of the following features is primarily associated with process value analysis? a. Defining root causes of each activity b. Identifying cost objects and activity drivers c. Calculating activity rate d. Assigning costs to cost objectsarrow_forwardClassify the following cost drivers as structural, executional, or operational. a. Number of plants b. Number of moves c. Degree of employee involvement d. Capacity utilization e. Number of product lines f. Number of distribution channels g. Engineering hours h. Direct labor hours i. Scope j. Product configuration k. Quality management approach l. Number of receiving orders m. Number of defective units n. Employee experience o. Types of process technologies p. Number of purchase orders q. Type and efficiency of layout r. Scale s. Number of functional departments t. Number of planning meetingsarrow_forwardActivity-based costing is preferable in a system: when multiple products have similar product volumes and costs with a large direct labor cost as a percentage of the total product cost with multiple, diverse products where management needs to support an increase in sales pricearrow_forward

- Lean manufacturing uses value streams to produce a family of products that require the same manufacturing sequence. Value-stream costing is an approach often used to determine the unit product costs in a lean manufacturing environment. Which of the following best describes how unit costs are calculated using value-stream costing? a. Value stream costs divided by units shipped b. Value stream costs divided by units produced c. (Total prime costs + overhead costs assigned to the value stream using a plantwide rate) divided by units produced d. Activity-based costing assignments within the value streamarrow_forwardThe following items are associated with a traditional cost accounting information system, an activity-based cost accounting information system, or both (that is, some elements are common to the two systems): a. Usage of direct materials b. Direct materials cost assigned to products using direct tracing c. Direct labor cost incurrence d. Direct labor cost assigned to products using direct tracing e. Setup cost incurrence f. Setup cost assigned using number of setups as the activity driver g. Setup cost assigned using direct labor hours as the activity driver h. Cost accounting personnel i. Submission of a bid, using product cost plus 25 percent j. Purchasing cost incurrence k. Purchasing cost assigned to products using direct labor hours as the activity driver l. Purchasing cost assigned to products using number of orders as the activity driver m. Materials handling cost incurrence n. Materials handling cost assigned using the number of moves as the activity driver o. Materials handling cost assigned using direct labor hours as the activity driver p. Computer q. Costing out of products r. Decision to continue making a part rather than buying it s. Printer t. Customer service cost incurred u. Customer service cost assigned to products using number of complaints as the activity driver v. Report detailing individual product costs w. Commission cost x. Commission cost assigned to products using units sold as the activity driver y. Plant depreciation z. Plant depreciation assigned to products using direct labor hours Required: 1. For each cost system, classify the relevant items into one of the following categories: a. Interrelated parts b. Processes c. Objectives d. Inputs e. Outputs f. User actions 2. Explain the choices that differ between the two systems. Which system will provide the best support for the user actions? Explain. 3. Draw an operational model that illustrates each cost accounting systemwith the items that belong to the system used as examples for each component of the model. 4. Based on the operational models, comment on the relative costs and benefits of the two systems. Which system should be chosen?arrow_forwardContinuous improvement is the governing principle of a lean accounting system. Following are several performance measures. Some of these measures would be associated with a traditional standard-costing accounting system, and some would be associated with a lean accounting system. a. Materials price variances b. Cycle time c. Comparison of actual product costs with target costs d. Materials quantity or efficiency variances e. Comparison of actual product costs over time (trend reports) f. Comparison of actual overhead costs, item by item, with the corresponding budgeted costs g. Comparison of product costs with competitors product costs h. Percentage of on-time deliveries i. First-time through j. Reports of value- and non-value-added costs k. Labor efficiency variances l. Days of inventory m. Downtime n. Manufacturing cycle efficiency (MCE) o. Unused (available) capacity variance p. Labor rate variance q. Using a sister plants best practices as a performance standard Required: 1. Classify each measure as lean or traditional (standard costing). If traditional, discuss the measures limitations for a lean environment. If it is a lean measure, describe how the measure supports the objectives of lean manufacturing. 2. Classify the measures into operational (nonfinancial) and financial categories. Explain why operational measures are better for control at the shop level (production floor) than financial measures. Should any financial measures be used at the operational level? 3. Suggest some additional measures that you would like to see added to the list that would be supportive of lean objectives.arrow_forward

- Which is not a step In activity-based costing? A. identify the activities performed by the organization B. identify the cost driver(s) associated with each activity C. compute a cost rate per production D. assign costs to products by multiplying the cost driver rate by the volume of the cost driver units consumed by the productarrow_forwardThe second stage of customer-based activity-based costing entails the assignment of: a. resource costs to sales departments. b. resources costs to distribution channels. c. customer-related activity costs to products. d. customer-related activity costs to customers.arrow_forwardHappy Trails has this information for its manufacturing: Â Its income statement under absorption costing is: Prepare an income statement with variable costing and a reconciliation statement between both methods.arrow_forward

- Trail Outfitters has this information for its manufacturing: Its income statement under absorption costing is as follows: Prepare an income statement with variable costing and a reconciliation statement between both methods.arrow_forwardIdentify appropriate cost drivers for these cost pools: A. setup cost pools B. assembly cost pool C. supervising cost pool D. testing cost poolarrow_forwardThe actions listed next are associated with either an activity-based operational control system or a traditional operational control system: a. Budgeted costs for the maintenance department are compared with the actual costs of the maintenance department. b. The maintenance department manager receives a bonus for beating budget. c. The costs of resources are traced to activities and then to products. d. The purchasing department is set up as a responsibility center. e. Activities are identified and listed. f. Activities are categorized as adding or not adding value to the organization. g. A standard for a products material usage cost is set and compared against the products actual materials usage cost. h. The cost of performing an activity is tracked over time. i. The distance between moves is identified as the cause of materials handling cost. j. A purchasing agent is rewarded for buying parts below the standard price set by the company. k. The cost of the materials handling activity is reduced dramatically by redesigning the plant layout. l. An investigation is undertaken to find out why the actual labor cost for the production of 1,000 units is greater than the labor standard allowed. m. The percentage of defective units is calculated and tracked over time. n. Engineering has been given the charge to find a way to reduce setup time by 75 percent. o. The manager of the receiving department lays off two receiving clerks so that the fourth-quarter budget can be met. Required: Classify the preceding actions as belonging to either an activity-based operational control system or a traditional control system. Explain why you classified each action as you did.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning