1.

To prepare: The

1.

Explanation of Solution

Journal:

Journal is the method of recording monetary business transactions in chronological order. It records the debit and credit aspects of each transaction to abide by the double-entry system.

Prepare the journal entries for the transactions that occurred from January 1 to January 31:

|

Date |

Account Title and Explanation | Debit ($) | Credit ($) | |

| January 1 |

Prepaid insurance (A+) |

5,700 |

||

| Cash (A-) | 5,700 | |||

| (To record the cash paid for the insurance expense) | ||||

| January 2 |

Prepaid rent |

4,200 |

||

| Cash (A-) | 4,200 | |||

| (To record the payment of prepaid rent) | ||||

| January 3 |

Cash (A+) |

30,000 |

||

| Notes payable (L+) | 30,000 | |||

| (To record the note payable) | ||||

| January 4 |

Equipment (A+) |

24,000 |

||

| Cash (A–) | 24,000 | |||

| (To record the purchase of an equipment) | ||||

| January 5 |

Cash (A+) |

6,000 |

||

| Common stock (SE+) | 6,000 | |||

| (To record the cash invested in common stock) | ||||

| January 6 |

Supplies (A+) |

1,000 |

||

| Accounts payable (L+) | 1,000 | |||

| (To record the additional purchase of supplies) | ||||

| January 7 |

Cash (A+) |

600 |

||

| 600 | ||||

| (To record the accounts receivable) | ||||

|

January 8 |

Accounts payable (L-) |

400 |

||

| Cash (A-) | 40 | |||

| (To record the accounts payable) | ||||

| January 9 |

Accounts receivable (A+) |

10,400 |

||

| Service revenue (R+) (SE+) | 10,400 | |||

| (To record the service provided to the customer on account) | ||||

| January 10 |

Cash (A+) |

7,600 |

||

| Service revenue (R+) (SE+) | 7,600 | |||

| (To record the cash received for the service performed) | ||||

| January 16 |

Salaries and wages expense (E+) (SE-) |

2,200 |

||

| Cash (A-) | 2,200 | |||

| (To record the payment of salaries and wages) | ||||

| January 20 |

Cash (A+) |

3,500 |

||

| Unearned revenue (L+) | 3,500 | |||

| (To record the unearned revenue) | ||||

| January 25 |

Cash (A+) |

4,500 |

||

| Accounts receivable (A-) | 4,500 | |||

| (To record the collection of cash from customer for service provided before) | ||||

Table (1)

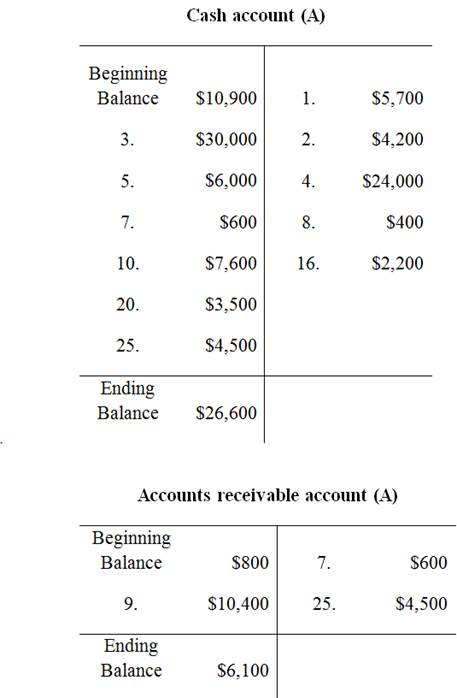

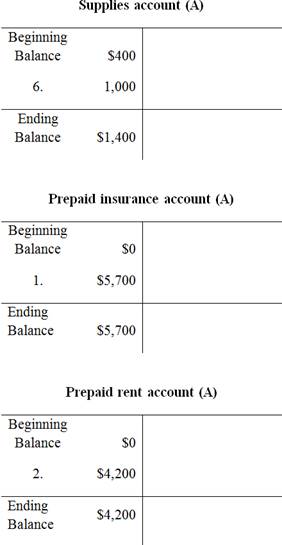

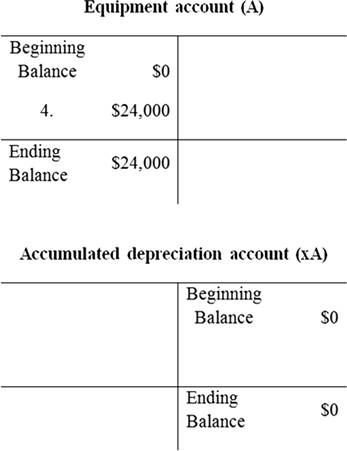

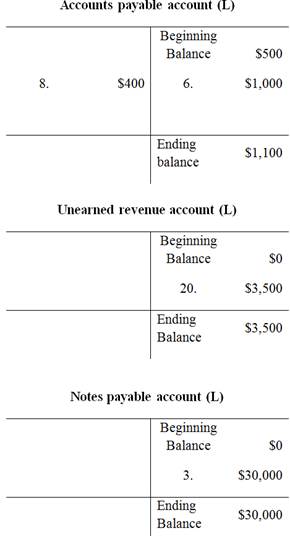

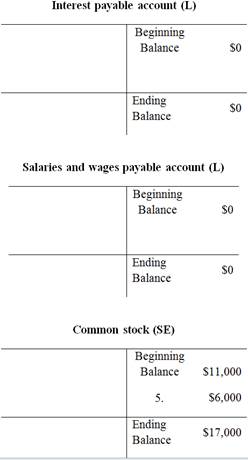

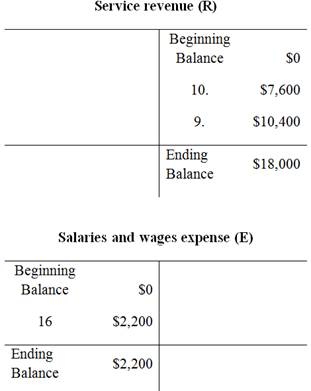

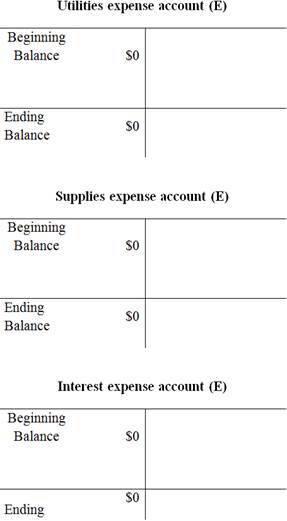

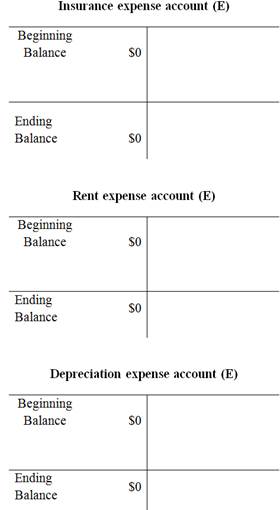

2.

To prepare: the T-Accounts using the beginning balances that are given in the January 1 balance sheet.

2.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability,

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

Prepare the T-Accounts:

Unadjusted

Unadjusted trial balance is that statement which contains complete list of accounts with their unadjusted balances. This statement is prepared at the end of every financial period.

Prepare the unadjusted trial balance:

| Incorporation FD | ||

| Unadjusted trial balance | ||

| As on 31st January | ||

| Account titles | Debit ($) | Credit ($) |

| Cash | 26,600 | |

| Accounts receivable | 6,100 | |

| Supplies | 1,400 | |

| Prepaid insurance | 5,700 | |

| Prepaid rent | 4,200 | |

| Equipment | 24,000 | |

| Accumulated |

0 | |

| Accounts payable | 1,100 | |

| Unearned revenue | 3,500 | |

| Notes payable | 30,000 | |

| Salaries and wages payable | 0 | |

| Interest payable | 0 | |

| Commonstock | 17,000 | |

| 600 | ||

| Service revenue | 18,000 | |

| Salaries and wages expense | 2,200 | |

| Supplies expense | 0 | |

| Depreciation expense | 0 | |

| Interest expense | 0 | |

| Total | 70,200 | 70,200 |

Table (2)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $70,200.

3.

To record: The adjusting journal entries that are needed at 31st January.

3.

Explanation of Solution

Adjusting entries are those entries which are made at the end of the accounting period, to record the revenues in the period of which they have been earned and to record the expenses in the period of which have been incurred, as well as to update all the balances of assets and liabilities accounts on the balance sheet, and to ascertain accurate amount of net income (loss) on the income statement to maintain the records according to the accrual basis principle.

Record the adjusting journal entries:

|

Date |

Account Title and Explanation | Debit ($) | Credit ($) | |

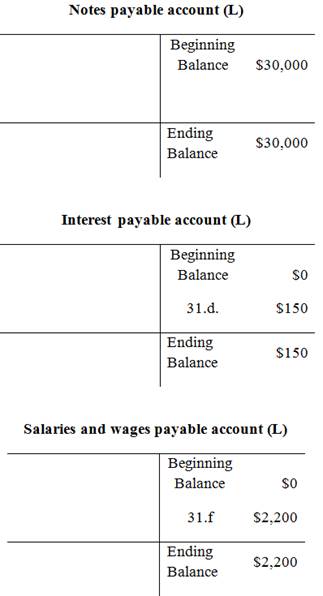

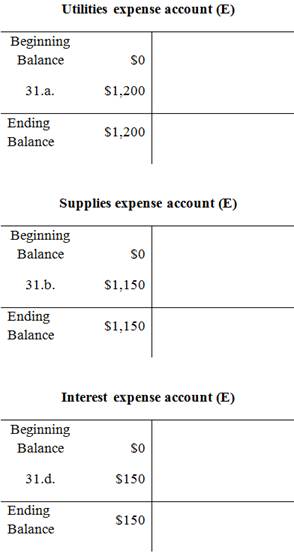

| January 31 |

a. |

Utilities Expense (E+, SE-) |

1,200 |

|

| Accounts payable (L+) | 1,200 | |||

| (To record the adjusting entry for utilities expense)) | ||||

| January 31 |

b. |

Supplies expense (E+) (SE-) |

1,150 |

|

| Supplies (A-) | 1,150 | |||

| (To record the adjusting entry for supplies expense) | ||||

| January 31 |

c. |

Unearned revenue (L-) |

2,100 |

|

| Service revenue (R+) (SE+) | 2,100 | |||

| (To record the adjusting entry for unearned revenue) | ||||

| January 31 |

d. |

Interest expense (E+) (SE-) |

150 |

|

| Interest payable (L+) | 150 | |||

| (To record the adjusting entry for interest expense) | ||||

| January 31 |

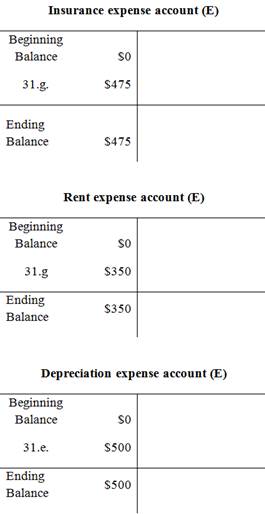

e. |

Depreciation Expense (E+) (SE-) |

500 |

|

| Accumulated depreciation- Equipment (xA+) (A-) |

500 |

|||

| (To record the adjusting entry for accumulated depreciation) | ||||

| January 31 |

f. |

Salaries and wages expense (E+) (SE-) |

2,200 |

|

| Salaries and wages payable (L+) | 2,200 | |||

| (To record the adjusting entry for salaries and wages expense) | ||||

| January 31 |

g. |

Insurance expense (E+) (SE-) |

475 |

|

| Prepaid insurance (A-) | 475 | |||

| (To record the adjusting entry for insurance expense) | ||||

| January 31 |

g. |

Rent expense (E+) (SE-) |

350 |

|

| Prepaid rent (A-) | 350 | |||

| (To record the adjusting entry for insurance expense) | ||||

Table (3)

Working note:

Calculate the amount of supplies expense:

Calculate the amount of unearned revenue:

Calculate the amount of interest expense:

Calculate the amount of depreciation expense:

Calculate the amount of Insurance expense:

Calculate the amount of rent expense:

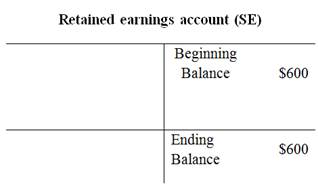

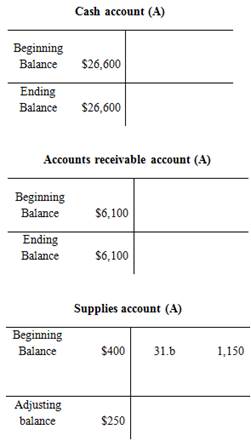

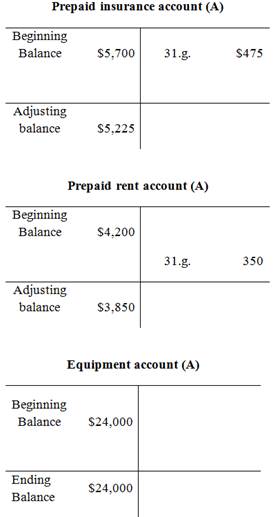

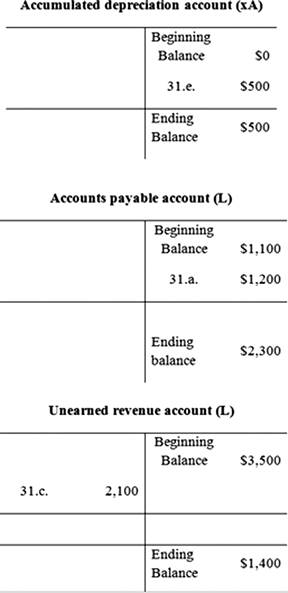

4.

To prepare: The T-Account from the requirement 3 for the adjusting journal entries.

4.

Explanation of Solution

T-account:

T-account refers to an individual account, where the increases or decreases in the value of specific asset, liability, stockholders’ equity, revenue, and expenditure items are recorded.

This account is referred to as the T-account, because the alignment of the components of the account resembles the capital letter ‘T’.’ An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

Prepare the T-Accounts:

Adjusted trial balance:

Adjusted trial balance is that statement which contains complete list of accounts with their adjusted balances, after all relevant adjustments have been made. This statement is prepared at the end of every financial period.

Prepare the adjusted trial balance:

| Incorporation FD | ||

| Adjusted trial balance | ||

| As on 31st January | ||

| Account titles | Debit ($) | Credit ($) |

| Cash | 26,600 | |

| Accounts receivable | 6,100 | |

| Supplies | 250 | |

| Prepaid insurance | 3,850 | |

| Prepaid rent | 5,225 | |

| Equipment | 24,000 | |

| Accumulated depreciation | 500 | |

| Accounts payable | 2,300 | |

| Unearned revenue | 1,400 | |

| Notes payable | 2,200 | |

| Salaries and wages payable | 150 | |

| Interest payable | 30,000 | |

| Commonstock | 17,000 | |

| Retained earnings | 600 | |

| Service revenue | 20,100 | |

| Salaries and wages expense | 4,400 | |

| Utilities expense | 1,200 | |

| Supplies expense | 1,150 | |

| Depreciation expense | 500 | |

| Insurance expense | 475 | |

| Rent expense | 350 | |

| Interest expense | 150 | |

| Total | 74,250 | 74,250 |

Table (4)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $74,250.

5.

To prepare: The income statement for the month ended 31st January.

5.

Explanation of Solution

Income statement:

The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare the income statement:

| Incorporation FD | ||

| Income statement | ||

| For the month end 31st January | ||

| Particulars | Amount( $) | Amount ($) |

| Revenue | ||

| Service revenue | 20,100 | |

| Total revenue(A) | 20,100 | |

| Expense | ||

| Salaries and wages | 4,400 | |

| Utilities | 1,200 | |

| Supplies | 1,150 | |

| Depreciation | 500 | |

| Insurance | 475 | |

| Rent | 350 | |

| Interest expense | 150 | |

| Total expense (B) | 8,225 | |

| Net income

|

11,875 | |

Table (5)

Thus the income statement of Incorporation FD is prepared and it shows the net income of $11,875.

Statement of retained earnings:

This is an equity statement which shows the changes in the stockholders’ equity over a period of time.

Prepare the statement of retained earnings:

| Incorporation FD | ||

| Statement of Retained earnings | ||

| For the month end 31st January | ||

| Particulars | Amount( $) | Amount ($) |

| Retained earnings, beginning | 600 | |

| Add: Net income | 11,875 | |

| Less:Dividends | 0 | |

| Retained earnings, end | 12,475 | |

Table (6)

Hence, the statement of retained earnings is prepared and the ending retained earnings are $12,475.

Classified balance sheet:

This is the financial statement of a company which shows the grouping of similar assets and liabilities under subheadings.

Prepare the classified balance sheet:

| Incorporation FD | ||

| Classified balance sheet | ||

| As on 31st January | ||

| Particulars | Amount($) | Amount($) |

| current asset: | ||

| Cash | 26,600 | |

| Accounts receivable | 6,100 | |

| Supplies | 250 | |

| Prepaid rent | 3,850 | |

| Prepaid insurance | 5,225 | |

| Total current assets | 42,025 | |

| Non-current assets | ||

| Equipment | 24,000 | |

| Accumulated depreciation-equipment net | 500 | |

| Total non-current asset | 24,500 | |

| Total assets | 65,525 | |

| Liabilities and stock holders' equity: | ||

| Current liabilities: | ||

| Accounts payable | 2,300 | |

| Unearned revenue | 1,400 | |

| Salaries and wages payable | 2,200 | |

| Interest payable | 150 | |

| Total current liabilities | 6,050 | |

| Non-current liabilities: | ||

| Notes payable | 30,000 | |

| Total non-current liabilities | 30,000 | |

| Total liabilities | 36,050 | |

| Stock holders' equity | 17,000 | |

| Retained earnings | 12,475 | |

| Total stockholders' equity | 29,475 | |

| Total liabilities and stock holders' equity | 65,525 | |

Table (7)

Hence, the classified balance sheet is prepared and the total assets and total liabilities and stockholders’ equity is $65,525.

Want to see more full solutions like this?

Chapter 4 Solutions

Connect Access Card for Fundamentals of Financial Accounting

- At the end of August, the first month of operations, the following selected data were taken from the financial statements of Tucker Jacobs, an attorney: In preparing the financial statements, adjustments for the following data were overlooked: Unbilled fees earned at August 31, 31,900. Depreciation of equipment for August, 7,500. Accrued wages at August 31, 5,200. Supplies used during August, 3,000. Instructions 1. Journalize the entries to record the omitted adjustments. 2. Determine the correct amount of net income for August and the total assets, liabilities, and owners equity at August 31. In addition to indicating the corrected amounts, indicate the effect of each omitted adjustment by setting up and completing a columnar table similar to the following. The first adjustment is presented as an example.arrow_forwardEddie Edwards and Phil Bell own and operate The Second Hand Equipment Shop. The following transactions involving notes and interest were completed during the last three months or 20--: REQUIRED 1. Prepare general journal entries for the transactions. 2. Prepare necessary adjusting entries for the notes outstanding on December 31.arrow_forwardCrazy Mountain Outfitters Co., an outfitter store for fishing treks, prepared the following unadjusted trial balance at the end of its first year of operations: For preparing the adjusting entries, the following data were assembled: Supplies on hand on April 30 were 1,380. Fees earned but unbilled on April 30 were 3,900. Depreciation of equipment was estimated to be 3,000 for the year. Unpaid wages accrued on April 30 were 2,475. The balance in unearned fees represented the April 1 receipt in advance for services to be provided. Only 14,140 of the services was provided between April 1 and April 30. Instructions 1. Journalize the adjusting entries necessary on April 30, 2019. 2. Determine the revenues, expenses, and net income of Crazy Mountain Outfitters Co. before the adjusting entries. 3. Determine the revenues, expenses, and net income of Crazy Mountain Outfitters Co. after the adjusting entries. 4. Determine the effect of the adjusting entries on John Bridger, Capital.arrow_forward

- Reece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services accounting clerk prepared the following unadjusted trial balance at July 31, 2019: The data needed to determine year-end adjustments are as follows: Depreciation of building for the year, 6,400. Depreciation of equipment for the year, 2,800. Accrued salaries and wages at July 31, 900. Unexpired insurance at July 31, 1,500. Fees earned but unbilled on July 31, 10,200. Supplies on hand at July 31, 615. Rent unearned at July 31, 300. Instructions 1. Journalize the adjusting entries using the following additional accounts: Salaries and Wages Payable, Rent Revenue, Insurance Expense, Depreciation ExpenseBuilding, Depreciation ExpenseEquipment, and Supplies Expense. 2. Determine the balances of the accounts affected by the adjusting entries and prepare an adjusted trial balance.arrow_forwardThe account balances of Bryan Company as of June 30, the end of the current fiscal year, are as follows: Required 1. Data for the adjustments are as follows: a. Expired or used up insurance, 495 b. Depreciation expense on equipment, 670. c. Depreciation expense on the van, 1,190. d. Salary accrued (earned) since the last payday, 540 (owed and to be paid on the next payday). e. Supplies used during the period, 97. Your instructor may want you to use a work sheet for these adjustments. 2. Journalize the adjusting entries. 3. Prepare an income statement. 4. Prepare a statement of owners equity. Assume that there was an additional investment of 2,000 on June 10. 5. Prepare a balance sheet. 6. Journalize the closing entries using the four steps in the correct sequence. Check Figure Net Income, 13,627arrow_forwardPrepare journal entries to record the following transactions that occurred in March: A. on first day of the month, purchased building for cash, $75,000 B. on fourth day of month, purchased inventory, on account, $6,875 C. on eleventh day of month, billed customer for services provided, $8,390 D. on nineteenth day of month, paid current month utility bill, $2,000 E. on last day of month, paid suppliers for previous purchases, $2,850arrow_forward

- Reece Financial Services Co., which specializes in appliance repair services, is owned and operated by Joni Reece. Reece Financial Services Co.s accounting clerk prepared the following unadjusted trial balance at July 31, 2016: The data needed to determine year-end adjustments are as follows: a. Depreciation of building for the year, 6,400. b. Depreciation of equipment for the year, 2,800. c. Accrued salaries and wages at July 31, 900. d. Unexpired insurance at July 31, 1,500. e. Fees earned but unbilled on July 31, 10,200. f. Supplies on hand at July 31, 615. g. Rent unearned at July 31, 300. Instructions 1. Journalize the adjusting entries using the following additional accounts: Salaries and Wages Payable; Rent Revenue; Insurance Expense; Depreciation ExpenseBuilding; Depreciation ExpenseEquipment; and Supplies Expense. 2. Determine the balances of the accounts affected by the adjusting entries and preparean adjusted trial balance.arrow_forwardPrepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. depreciation on buildings and equipment, $17,500 B. advertising still prepaid at year end, $2,200 C. interest due on notes payable, $4,300 D. unearned rental revenue, $6,900 E. interest receivable on notes receivable, $1,200arrow_forwardPrepare adjusting journal entries, as needed, considering the account balances excerpted from the unadjusted trial balance and the adjustment data. A. supplies actual count at year end, $6,500 B. remaining unexpired insurance, $6,000 C. remaining unearned service revenue, $1,200 D. salaries owed to employees, $2,400 E. depreciation on property plant and equipment, $18,000arrow_forward

- The Detection of Errors in a Trial Balance and Preparation of a Corrected Trial Balance Malcolm Inc. was incorporated on January 1 with the issuance of capital stock in return for $90,000 of cash contributed by the owners. The only other transaction entered into prior to beginning operations was the issuance of a $75,300 note payable in exchange for building and equipment. The following trial balance was prepared at the end of the first month by the bookkeeper for Malcolm Inc.: Required Identify the two errors in the trial balance. Ignore depreciation expense and interest expense. Prepare a corrected trial balance.arrow_forwardAdjusting entries Trident Repairs Service, an electronics repair store, prepared the following unadjusted trial balance at the end of its first year of operations: For preparing the adjusting entries, the following data were assembled: Fees earned but unbilled on November 30 were 7,000. Supplies on hand on November 30 were 1,300. Depreciation of equipment was estimated to be 7,200 for the year. The balance in unearned fees represented the November 1 receipt in advance for services to be provided. During November, 13,500 of the services were provided. Unpaid wages accrued on November 30 were 4,800. Instructions 1. Journalize the adjusting entries necessary on November 30, 20Y3. 2. Determine the revenues, expenses, and net income of Trident Repairs Service before the adjusting entries. 3. Determine the revenues, expense, and net income of Trident Repairs Service after the adjusting entries. 4. Determine the effect of the adjusting entries on Retained Earnings.arrow_forwardWorksheet for Service Company Whitaker Consulting Company has prepared a trial balance on the following partially completed worksheet for the year ended December 31, 2019: Additional information: (a) On January 1, 2019, the company had paid 2 years rent in advance at 100 a month for office space, (b) the office equipment is being depreciated on a straight-line basis over a 10-year life, and no residua! value is expected, (c) interest of 150 has accrued on the note payable but has not been paid, and (d) the income tax rate is 30% on current income and will be paid in the first quarter of 2020. Required: 1. Complete the worksheet. 2. Prepare financial statements for 2019.arrow_forward

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning