Concept explainers

Videos

Recording Transactions and Adjustments, Reconciling Items, and Preparing Financial Statements

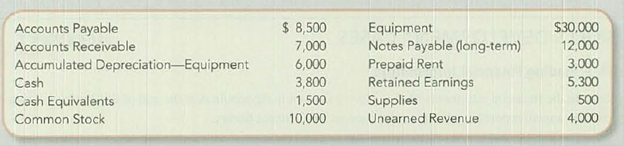

On January 1, Pulse Recording Studio (PRS) had the following account balances.

The following transactions occurred during January.

- 1. Received $2,500 cash on l/l from customers on account for recording services completed in December.

- 2. Wrote checks on 1/2 totaling $4,000 for amounts owed on account at the end of December.

- 3. Purchased and received supplies on account on 1/3, at a total cost of $200.

- 4. Completed $4,000 of recording sessions on 1/4 that customers had paid for in advance in December.

- 5. Received $5,000 cash on 1/5 from customers for recording sessions started and completed in January.

- 6. Wrote a check on 1/6 for $4,000 for an amount owed on account.

- 7. Converted $1,000 of cash equivalents into cash on 1/7.

- 8. On 1/15, completed EFTs for $1,500 for employees’ salaries and wages for the first half of January.

- 9. Received $3,000 cash on 1/31 from customers for recording sessions to start in February.

Required:

- 1. Prepare journal entries for the January transactions.

- 2. Enter the January 1 balances into T-accounts,

post the journal entries from requirement 1, and calculate January 31 balances. (If you are completing this requirement in Connect, this requirement will be completed for you.) - 3. Use the January 31 balance in Cash from requirement 2 and the following information to prepare a bank reconciliation. PRS’s bank reported a January 31 balance of $6,300.

- 10. The bank deducted $500 for an NSF check from a customer deposited on January 5.

- 11. The check written January 6 has not cleared the bank, but the January 2 payment has cleared.

- 12. The cash received and deposited on January 31 was not processed by the bank until February 1.

- 13. The bank added $5 cash to the account for interest earned in January.

- 14. The bank deducted $5 for service charges.

- 4. Prepare journal entries for items (10)–(14) from the bank reconciliation, if applicable, and post them to the T-accounts. If a

journal entry is not required for one or more of the reconciling items, indicate “no journal entry required.” (If you are using Connect, journal entries will be automatically posted after you enter them.) - 5. Prepare

adjusting journal entries on 1/31, using the following information. - 15.

Depreciation for the month is $200. - 16. Salaries and wages totaling $1,500 have not yet been recorded for January 16–31.

- 17. Prepaid Rent will be fully used up by March 31.

- 18. Supplies on hand at January 31 were $500.

- 19. Received $600 invoice for January electricity charged on account to be paid in February but is not yet recorded.

- 20. Interest on the promissory note of $60 for January has not yet been recorded or paid.

- 21. Income tax of $1,000 on January income has not yet been recorded or paid.

- 6. Post the adjusting journal entries from requirement 5 to the T-accounts and prepare an adjusted

trial balance . (If you are completing this requirement in Connect, it will be completed for you using your previous answers.) - 7. Prepare an income statement for January and a classified balance sheet at January 31. Report PRS’s cash and cash equivalents as a single line on the balance sheet.

- 8. Calculate the

current ratio at January 31 and indicate whether PRS has met its loan covenant that requires a minimum current ratio of 1.2. - 9. Calculate the net profit margin and indicate whether PRS has achieved its objective of 10 percent.

(1)

To prepare: Journal entries for the transactions occurred in January in the books of PR Studio

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

Prepare journal entry for the transaction occurred on January 1.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 1 | Cash | 2,500 | |||

| Accounts Receivable | 2,500 | |||||

| (To record cash received for services on account) | ||||||

Table (1)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Accounts Receivable is an asset account. Since amount to be received has decreased, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for the transaction occurred on January 2.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 2 | Accounts Payable | 4,000 | |||

| Cash | 4,000 | |||||

| (To record payment of on account purchases) | ||||||

Table (2)

Description:

- Accounts Payable is a liability account. Since the amount to be paid is paid, liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for the transaction occurred on January 3.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 3 | Supplies | 200 | |||

| Accounts Payable | 200 | |||||

| (To record purchase of supplies on account) | ||||||

Table (3)

Description:

- Supplies is an asset account. Since supplies are bought, asset account increased, and an increase in asset is debited.

- Accounts Payable is a liability account. Since the amount to be paid increased, liability increased, and an increase in liability is credited.

Prepare journal entry for the transaction occurred on January 4.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 4 | Unearned Revenue | 4,000 | |||

| Service Revenue | 4,000 | |||||

| (To record revenue earned, paid for in advance in December) | ||||||

Table (4)

Description:

- Unearned Revenue is a liability account. Since the unearned revenue is earned, liability is reduced, and a decrease in liability is debited.

- Service Revenue is a revenue account. Since the unearned revenue has been earned, revenue value increased, and an increase in revenues increases stockholders’ equity. Hence, the account is credited.

Prepare journal entry for the transaction occurred on January 5.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 5 | Cash | 5,000 | |||

| Service Revenue | 5,000 | |||||

| (To record revenue received for services performed) | ||||||

Table (5)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Service Revenue is a revenue account. Since revenues increase equity, equity value is increased. An increase in equity is credited.

Prepare journal entry for the transaction occurred on January 6.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 6 | Accounts Payable | 4,000 | |||

| Cash | 4,000 | |||||

| (To record payment of on account purchases) | ||||||

Table (6)

Description:

- Accounts Payable is a liability account. Since the amount to be paid is paid, liability decreased, and a decrease in liability is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for the transaction occurred on January 7.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 7 | Cash | 1,000 | |||

| Cash Equivalents | 1,000 | |||||

| (To record conversion of cash equivalents into cash) | ||||||

Table (7)

Description:

- Cash is an asset account. Since cash equivalents are converted to cash, asset account increased, and an increase in asset is debited.

- Cash Equivalents is an asset account. Since cash equivalent re converted into cash, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for the transaction occurred on January 15.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 15 | Salaries and Wages Expense | 1,500 | |||

| Cash | 1,500 | |||||

| (To record payment of wages and salaries expense) | ||||||

Table (8)

Description:

- Salaries and Wages Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Cash is an asset account. Since cash is paid, asset account decreased, and a decrease in asset is credited.

Prepare journal entry for the transaction occurred on January 31.

| Date | Account Titles and Explanations | Post. Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Cash | 3,000 | |||

| Unearned Revenue | 3,000 | |||||

| (To record revenue received for future services to be performed) | ||||||

Table (9)

Description:

- Cash is an asset account. Since cash is received, asset account increased, and an increase in asset is debited.

- Unearned Revenue is a liability account. Since cash received for services to be performed, liability is increased. An increase in liability is credited.

(2)

To open: The T-accounts with balances as on January 1, post the entries recorded in Part (1), and compute the balances as on January 31

Explanation of Solution

T-account: The condensed form of a ledger is referred to as T-account. The left-hand side of this account is known as debit, and the right hand side is known as credit.

Open the T-accounts with balances as on January 1, post the entries recorded in Part (1), and compute the balances as on January 31.

| Cash | |||

| January1 | 3,800 | 4,000 | January 2 |

| January 1 | 2,500 | 4,000 | January 6 |

| January 5 | 5,000 | 1,500 | January 15 |

| January 1 | 1,000 | ||

| January 1 | 3,000 | ||

| Total | 15,300 | 9,500 | Total |

| Balance | $5,800 | ||

Table (10)

| Cash Equivalents | |||

| January 1 | 1,500 | 1,000 | January 7 |

| Total | 1,500 | 1,000 | Total |

| Balance | $500 | ||

Table (11)

| Accounts Receivable | |||

| January 1 | 7,000 | 2,500 | January 1 |

| Total | 7,000 | 2,500 | Total |

| Balance | $4,500 | ||

Table (12)

| Supplies | |||

| January 1 | 500 | ||

| January 3 | 200 | ||

| Balance | $700 | ||

Table (13)

| Prepaid Rent | |||

| January 1 | 3,000 | ||

| Balance | $3,000 | ||

Table (14)

| Equipment | |||

| January 1 | 30,000 | ||

| Balance | $30,000 | ||

Table (15)

| Accumulated Depreciation–Equipment | |||

| 6,000 | January 1 | ||

| $6,000 | Balance | ||

Table (16)

| Accounts Payable | |||

| January 1 | 4,000 | 8,500 | January 1 |

| January 6 | 4,000 | 200 | January 3 |

| Total | 8,000 | 8,700 | Total |

| $700 | Balance | ||

Table (17)

| Unearned Revenue | |||

| January 1 | 4,000 | 4,000 | January 1 |

| 3,000 | January 31 | ||

| Total | 4,000 | 7,000 | Total |

| $3,000 | Balance | ||

Table (18)

| Notes Payable | |||

| 12,000 | January 1 | ||

| $12,000 | Balance | ||

Table (19)

| Common Stock | |||

| 10,000 | January 1 | ||

| $10,000 | Balance | ||

Table (20)

| Retained Earnings | |||

| 10,000 | January 1 | ||

| $10,000 | Balance | ||

Table (21)

| Service Revenue | |||

| 0 | January 1 | ||

| 4,000 | January 4 | ||

| 5,000 | January 5 | ||

| $9,000 | Balance | ||

Table (22)

| Salaries and Wages Expense | |||

| January 1 | 0 | ||

| January 15 | 1,500 | ||

| Balance | $1,500 | ||

Table (23)

(3)

To prepare: Bank reconciliation of PR Studio, as at January 31

Explanation of Solution

Bank reconciliation: Bank statement is prepared by bank. The company maintains its own records from its perspective. This is why the cash balance per bank and cash balance per books seldom agree. Bank reconciliation is the statement prepared by company to remove the differences and disagreement between cash balance per bank and cash balance per books.

Prepare bank reconciliation of PR Studio, as at January 31.

| PR Studio | ||||

| Bank Reconciliation | ||||

| January 31 | ||||

| Updates to Bank Statement | Updates to Company’s Books | |||

| Ending cash balance per bank statement | $6,300 | Ending cash balance per books | $5,800 | |

| Additions: | Additions: | |||

| Deposits in transit | 3,000 | Interest received | 5 | |

| 9,300 | 5,805 | |||

| Deductions: | Deductions: | |||

| Outstanding checks | 4,000 | NSF check | 500 | |

| Up-to-date ending cash balance | $5,300 | Bank service charge | 5 | 505 |

| Up-to-date ending cash balance | $5,300 | |||

Table (24)

Description:

- The deposits which are not recorded by the bank are referred to as deposits in transit. Since the deposits in transit are not reflected on the bank statement, the company should add deposits in transit to cash balance per bank, while preparation of bank reconciliation statement.

- Outstanding checks are the checks that are issued by the company, but not yet paid by the bank. When the check is issued for payment, the company deducts the cash balance immediately. But the bank deducts only when the cash is paid for the issued check. So, company deducts the cash balance per bank to remove the differences.

- Interest received is credited by bank to the bank account of which the company is not aware of. So, while preparing bank reconciliation statement, company should add the amount to the cash balance per books.

- While bank reconciliation, the NSF check should be deducted from the cash balance per book. This is because the bank could not collect funds from the customer’s bank due to lack of funds. But being recorded as Accounts Receivable previously, the balance should be deducted from books, to increase the Accounts Receivable account.

- Banks deduct the service charge for the services rendered like lock box rental, or printed checks. But the company is not aware of such deductions. So, company deducts the cash balance per books while bank reconciliation preparation.

(4)

To prepare: Adjusting journal entries for items (10) to (14) that arise due to bank reconciliation, and post the entries into T-accounts

Explanation of Solution

Journal entry: Journal entry is a set of economic events which can be measured in monetary terms. These are recorded chronologically and systematically.

Debit and credit rules:

- Debit an increase in asset account, increase in expense account, decrease in liability account, and decrease in stockholders’ equity accounts.

- Credit decrease in asset account, increase in revenue account, increase in liability account, and increase in stockholders’ equity accounts.

(10)

Prepare journal entry to record NSF check.

| Date | Account Titles and Explanation | Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Accounts Receivable | 500 | |||

| Cash | 500 | |||||

| (To record NSF check) | ||||||

Table (25)

Description:

- Accounts Receivable is an asset account. The bank has not collected the amount from the customer due to insufficient funds, which was earlier recorded as a receipt. As the collection could not be made, amount to be received increased. Therefore, increase in asset would be debited.

- Cash is an asset account. The amount is decreased because bank could not collect amount due to insufficient funds in customer’s account, and a decrease in asset is credited.

(11)

Prepare journal entry for the checks written but not cleared by bank.

These are the outstanding checks, which are recorded by the company. So, company does not record it again, but this is an adjustment for bank balance. Hence, no journal entry is required.

(12)

Prepare journal entry for the deposits recorded by company.

These are the checks deposited by company but not recorded by bank, which are recorded by the company. So, company does not record it again, but this is an adjustment for bank balance. Hence, no journal entry is required.

(13)

Prepare journal entry to record interest received.

| Date | Account Titles and Explanation | Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Cash | 5 | |||

| Interest Revenue | 5 | |||||

| (To record interest earned) | ||||||

Table (26)

Description:

- Cash is an asset account. The amount is increased because credited the interest earned on checking account, and an increase in asset is debited.

- Interest Revenue is a revenue account. Revenuesincrease Equity account and an increase in Equity is credited.

(14)

Prepare journal entry to record bank service charge.

| Date | Account Titles and Explanation | Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Office Expense | 5 | |||

| Cash | 5 | |||||

| (To record bank service charge) | ||||||

Table (27)

Description:

- Office Expenses is an expense account and the amount is increased because bank has charged service charges. Expenses decrease Equity account and decrease in Equity is debited.

- Cash is an asset account. The amount is decreased because bank service charge is paid, and a decrease in asset is credited.

Prepare T-accounts.

| Cash | |||

| Balance | $5,800 | ||

| January 31 | 5 | 500 | January 31 |

| 5 | January 31 | ||

| Total | 5,805 | 505 | Total |

| Balance | $5,300 | ||

Table (28)

| Accounts Receivable | |||

| Balance | $4,500 | ||

| January 31 | 500 | ||

| Balance | $5,000 | ||

Table (29)

| Interest Revenue | |||

| 0 | January 1 | ||

| 5 | January 31 | ||

| $5 | Balance | ||

Table (30)

| Office Expense | |||

| January 1 | 0 | ||

| January 31 | 5 | ||

| Balance | $5 | ||

Table (31)

(5)

To journalize: The adjusting entries for the items (19) to (21) as on January 31

Explanation of Solution

Adjusting entries: Adjusting entries are those entries which are recorded at the end of the year to update the income statement accounts (revenue and expenses) and balance sheet accounts (assets, liabilities, and stockholders’ equity) to maintain the records according to accrual basis principle.

15.

Prepare adjusting entry for the depreciation expense as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Depreciation Expense | 200 | |||

| Accumulated Depreciation–Equipment | 200 | |||||

| (To record depreciation expense) | ||||||

Table (32)

Description:

- Depreciation Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accumulated Depreciation–Equipment is a contra-asset account, and contra-asset accounts would have a normal credit balance, hence, the account is credited.

16.

Prepare adjusting entry for the wages expense as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Salaries and Wages Expense | 1,500 | |||

| Salaries and Wages Payable | 1,500 | |||||

| (To record accrued expenses) | ||||||

Table (33)

Description:

- Salaries and Wages Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Salaries and Wages Payable is a liability account. Since amount of payables has increased, liability decreased, and an increase in liability is credited.

17.

Prepare adjusting entry for the prepaid rent as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Rent Expense | 1,000 | |||

| Prepaid Rent | 1,000 | |||||

| (To record part of prepaid rent expired) | ||||||

Table (34)

Description:

- Rent Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Prepaid Rent is an asset account. Since amount of rent is expired, asset account decreased, and a decrease in asset is credited.

18.

Prepare adjusting entry for the supplies as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Supplies Expense | 200 | |||

| Supplies | 100 | |||||

| (To record part of supplies consumed) | ||||||

Table (35)

Description:

- Supplies Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Supplies is an asset account. Since amount of supplies is used, asset account decreased, and a decrease in asset is credited.

19.

Prepare adjusting entry for the utilities expense as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Utilities Expense | 600 | |||

| Accounts Payable | 600 | |||||

| (To record accrued expenses) | ||||||

Table (36)

Description:

- Utilities Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Accounts Payable is a liability account. Since amount of payables has increased, liability decreased, and an increase in liability is credited.

20.

Prepare adjusting entry for the interest expense as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Interest Expense | 600 | |||

| Interest Payable | 600 | |||||

| (To record accrued expenses) | ||||||

Table (37)

Description:

- Interest Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Interest Payable is a liability account. Since amount of payables has increased, liability decreased, and an increase in liability is credited.

21.

Prepare adjusting entry for the utilities expense as on January 31.

| Date | Account Titles and Explanation | Post Ref. | Debit ($) | Credit ($) | ||

| January | 31 | Income Tax Expense | 600 | |||

| Income Tax Payable | 600 | |||||

| (To record accrued expenses) | ||||||

Table (38)

Description:

- Income Tax Expense is an expense account. Since expenses decrease equity, equity value is decreased, and a decrease in equity is debited.

- Income Tax Payable is a liability account. Since amount of payables has increased, liability decreased, and an increase in liability is credited.

(6)

To journalize: Post the adjusted entries into T-accounts, and prepare adjusted trial balance for PR Studio as on January 31

Explanation of Solution

Post the adjusting entries into T-accounts.

| Supplies | |||

| Balance | 700 | ||

| 200 | January 31 | ||

| Total | 700 | 200 | Total |

| Balance | $500 | ||

Table (39)

| Prepaid Rent | |||

| Balance | 3,000 | 1,000 | January 31 |

| Balance | $2,000 | ||

Table (40)

| Accumulated Depreciation–Equipment | |||

| 6,000 | Balance | ||

| 200 | January 31 | ||

| $6,200 | Balance | ||

Table (41)

| Interest Payable | |||

| 60 | January 31 | ||

| $60 | Balance | ||

Table (42)

| Income Tax Payable | |||

| 1,000 | January 31 | ||

| $1,000 | Balance | ||

Table (43)

| Salaries and Wages Payable | |||

| 1,500 | January 31 | ||

| $1,500 | Balance | ||

Table (44)

| Accounts Payable | |||

| 700 | Balance | ||

| 600 | January 31 | ||

| $1,300 | Balance | ||

Table (45)

| Depreciation Expense | |||

| January 1 | 0 | ||

| January 31 | 200 | ||

| Balance | $200 | ||

Table (46)

| Rent Expense | |||

| January 1 | 0 | ||

| January 31 | 1,000 | ||

| Balance | $1,000 | ||

Table (47)

| Supplies Expense | |||

| January 1 | 0 | ||

| January 31 | 200 | ||

| Balance | $200 | ||

Table (48)

| Utilities Expense | |||

| January 1 | 0 | ||

| January 31 | 600 | ||

| Balance | $600 | ||

Table (49)

| Interest Expense | |||

| January 1 | 0 | ||

| January 31 | 60 | ||

| Balance | $60 | ||

Table (50)

| Income Tax Expense | |||

| January 1 | 0 | ||

| January 31 | 1,000 | ||

| Balance | $1,000 | ||

Table (51)

| Salaries and Wages Expense | |||

| January 1 | 1,500 | ||

| January 31 | 1,500 | ||

| Balance | $3,000 | ||

Table (52)

Adjusted trial balance: It is that statement which shows all the asset, liability, and equity account balances at the year-end, after recording of adjusting entries.

Prepare adjusted trial balance of PR Studio as on January 31.

| PR Studio | ||

| Adjusted Trial Balance | ||

| January 31 | ||

| Particulars | Debit $ | Credit $ |

| Cash | $5,300 | |

| Cash Equivalents | 500 | |

| Accounts Receivable | 5,000 | |

| Prepaid Rent | 2,000 | |

| Supplies | 500 | |

| Equipment | 30,000 | |

| Accumulated Depreciation - Equipment | 6,200 | |

| Accounts Payable | 1,300 | |

| Interest Payable | 60 | |

| Income Tax Payable | 1,000 | |

| Salaries and Wages Payable | 1,500 | |

| Unearned Revenue | 3,000 | |

| Notes Payable (Long-term) | 12,000 | |

| Common Stock | 10,000 | |

| Retained Earnings | 5,300 | |

| Service Revenue | 9,000 | |

| Interest Revenue | 5 | |

| Salaries and Wages Expense | 3,000 | |

| Rent Expense | 1,000 | |

| Income Tax Expense | 1,000 | |

| Utilities Expense | 600 | |

| Depreciation Expense | 200 | |

| Supplies Expense | 200 | |

| Interest Expense | 60 | |

| Office Expense | 5 | |

| Total | $49,365 | $49,365 |

Table (53)

(7)

To prepare: Income statement of PR Studio for the month ended January 31, and classified balance sheet of PR Studio as on January 31

Explanation of Solution

Income statement: The financial statement which reports revenues and expenses from business operations and the result of those operations as net income or net loss for a particular time period is referred to as income statement.

Prepare income statement for PR Studio for the month ended January 31.

| PR Studio | ||

| Income Statement | ||

| For the Month Ended January 31 | ||

| Revenue | ||

| Service revenue | $9,000 | |

| Interest revenue | 5 | |

| Total revenue | $9,005 | |

| Expenses | ||

| Salaries and wages expense | $3,000 | |

| Rent expense | 1,000 | |

| Income tax expense | 1,000 | |

| Utilities expense | 600 | |

| Depreciation expense | 200 | |

| Supplies expense | 200 | |

| Interest expense | 60 | |

| Office expense | 5 | |

| Total expenses | 6,065 | |

| Net income | $2,940 | |

Table (54)

Classified balance sheet: The main elements of balance sheet assets, liabilities, and stockholders’ equity are categorized or classified further into sections in a classified balance sheet. Assets are further classified as current assets, long-term investments, property, plant, and equipment (PPE), and intangible assets. Liabilities are classified into two sections current and long-term. Stockholders’ equity comprises of common stock and retained earnings. Thus, the classified balance sheet includes all the elements under different sections.

Prepare classified balance sheet for PR Studio, as at January 31.

| PR Studio | ||

| Balance Sheet | ||

| January 31 | ||

| Assets | ||

| Current assets | ||

| Cash and cash equivalents | $5,800 | |

| Accounts receivable | 5,000 | |

| Supplies | 500 | |

| Prepaid rent | 2,000 | |

| Total current assets | $13,300 | |

| Property, plant, and equipment | ||

| Equipment | 30,000 | |

| Less: Accumulated depreciation | 6,200 | 23,800 |

| Total assets | $37,100 | |

| Liabilities and Stockholders’ Equity | ||

| Current liabilities | ||

| Accounts payable | $1,300 | |

| Interest payable | 60 | |

| Income tax payable | 1,000 | |

| Salaries and wages payable | 1,500 | |

| Unearned revenue | 3,000 | |

| Total current liabilities | $6,860 | |

| Long-term liabilities | ||

| Notes payable | 12,000 | |

| Total liabilities | 18,860 | |

| Stockholders’ equity | ||

| Common stock | 10,000 | |

| Retained earnings | 8,240 | |

| Total stockholders’ equity | 18,240 | |

| Total liabilities and stockholders’ equity | $37,100 | |

Table (55)

Working Notes:

Compute retained earnings for the month ended January 31.

| Particulars | Amount ($) |

| Retained earnings, January 1 | $5,300 |

| Add: Net income | 2,940 |

| 8,240 | |

| Less: Dividends | 0 |

| Retained earnings, January 31 | $8,240 |

Table (56)

Note: Refer to Table (54) for net income value.

(7)

Explanation of Solution

Current ratio: The financial ratio which evaluates the ability of a company to pay off the debt obligations which mature within one year or within completion of operating cycle is referred to as current ratio. This ratio assesses the liquidity of a company.

Formula of current ratio:

Compute current ratio of PR Studio for the month ended January 31, if current assets are $13,300 and current liabilities are $6,860.

(8)

Explanation of Solution

Net profit margin: This ratio gauges the operating profitability by quantifying the amount of income earned from business operations from the sales generated.

Formula of net profit margin:

Determine the net profit margin for PR Studio for the month ended January 31, if net income is $2,940 and total revenue is $9,005.

Note: Refer to Table (54) for both values.

Want to see more full solutions like this?

Chapter 5 Solutions

Loose-leaf for Fundamentals of Financial Accounting with Connect

Additional Business Textbook Solutions

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Accounting For Governmental & Nonprofit Entities

PRINCIPLES OF TAXATION F/BUS.+INVEST.

Financial Accounting, Student Value Edition (4th Edition)

Financial Accounting

Financial Accounting (11th Edition)

- Post the following July transactions to T-accounts for Accounts Receivable, Sales Revenue, and Cash, indicating the ending balance. Assume no beginning balances in these accounts. A. on first day of the month, sold products to customers for cash, $13,660 B. on fifth day of month, sold products to customers on account, $22,100 C. on tenth day of month, collected cash from customer accounts, $18,500arrow_forwardPrepare journal entries to record the following transactions: A. December 1, collected balance due from customer account, $5,500 B. December 12, paid creditors for supplies purchased last month, $4,200 C. December 31, paid cash dividend to stockholders, $1,000arrow_forwardJournal entries and trial balance On August 1, 20Y7, Rafael Masey established Planet Realty, which completed the following transactions during the month: a. Rafael Masey transferred cash from a personal bank account to an account to be used for the business in exchange for common stock, 17,500. b. Purchased supplies on account, 2,300. c. Earned sales commissions, receiving cash, 13,300. d. Paid rent on office and equipment for the month, 3,000. e. Paid creditor on account, 1,150. f. Paid dividends, 1,800. g. Paid automobile expenses (including rental charge) for month, 1,500, and miscellaneous expenses, 400. h. Paid office salaries, 2,800. i. Determined that the cost of supplies used was 1,050. Instructions 1. Journalize entries for transactions (a) through (i), using the following account titles: Cash, Supplies, Accounts Payable, Common Stock, Dividends, Sales Commissions, Rent Expense, Office Salaries Expense, Automobile Expense, Supplies Expense, Miscellaneous Expense. Journal entry explanations may be omitted. 2. Prepare T accounts, using the account titles in (1). Post the journal entries to these accounts, placing the appropriate letter to the left of each amount to identify the transactions. Determine the account balances, after all posting is complete. Accounts containing only a single entry do not need a balance. 3. Prepare an unadjusted trial balance as of August 31, 20Y7. 4. Determine the following: a. Amount of total revenue recorded in the ledger. b. Amount of total expenses recorded in the ledger. c. Amount of net income for August. 5. Determine the increase or decrease in retained earnings for August.arrow_forward

- Reconstructing a Beginning Account Balance During the month, services performed for customers on account amounted to $7,500 and collections from customers in payment of their accounts totaled $6,000. At the end of the month, the Accounts Receivable account had a balance of $2,500. What was the Accounts Receivable balance at the beginning of the month?arrow_forwardOn July 1, K. Resser opened Ressers Business Services. Ressers accountant listed the following chart of accounts: The following transactions were completed during July: a. Resser deposited 25,000 in a bank account in the name of the business. b. Bought tables and chairs for cash, 725, Ck. No. 1200. c. Paid the rent for the current month, 1,750, Ck. No. 1201. d. Bought computers and copy machines from Ferber Equipment, 15,700, paying 4,000 in cash and placing the balance on account, Ck. No. 1202. e. Bought supplies on account from Wigginss Distributors, 535. f. Sold services for cash, 1,742. g. Bought insurance for one year, 1,375, Ck. No. 1203. h. Paid on account to Ferber Equipment, 700, Ck. No. 1204. i. Received and paid the electric bill, 438, Ck. No. 1205. j. Paid on account to Wigginss Distributors, 315, Ck. No. 1206. k. Sold services to customers for cash for the second half of the month, 820. l. Received and paid the bill for the business license, 75, Ck. No. 1207. m. Paid wages to an employee, 1,200, Ck. No. 1208. n. Resser withdrew cash for personal use, 700, Ck. No. 1209. Required 1. Record the owners name in the Capital and Drawing T accounts. 2. Correctly place the plus and minus signs for each T account and label the debit and credit sides of the accounts. 3. Record the transactions in the T accounts. Write the letter of each entry to identify the transaction. 4. Foot the T accounts and show the balances. 5. Prepare a trial balance as of July 31, 20--. 6. Prepare an income statement for July 31, 20--. 7. Prepare a statement of owners equity for July 31, 20--. 8. Prepare a balance sheet as of July 31, 20--. LO 1, 2, 3, 4, 5, 6arrow_forwardIn March, T. Carter established Carter Delivery Service. The account headings are presented below. Transactions completed during the month of March follow. a. Carter deposited 25,000 in a bank account in the name of the business. b. Bought a used truck from Degroot Motors for 15,140, paying 5,140 in cash and placing the remainder on account. c. Bought equipment on account from Flemming Company, 3,450. d. Paid the rent for the month, 1,000, Ck. No. 3001. e. Sold services for cash for the first half of the month, 6,927. f. Bought supplies for cash, 301, Ck. No. 3002. g. Bought insurance for the truck for the year, 1,200, Ck. No. 3003. h. Received and paid the bill for utilities, 349, Ck. No. 3004. i. Received a bill for gas and oil for the truck, 218. j. Sold services on account, 3,603. k. Sold services for cash for the remainder of the month, 4,612. l. Paid wages to the employees, 3,958, Ck. Nos. 30053007. m. Carter withdrew cash for personal use, 1,250, Ck. No. 3008. Required 1. Record the transactions and the balance after each transaction 2. Total the left side of the accounting equation (left side of the equal sign), then total the right side of the accounting equation (right side of the equal sign). If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forward

- Analyzing the Accounts The controller for Summit Sales Inc. provides the following information on transactions that occurred during the year: a. Purchased supplies on credit, $18,600 b. Paid $14,800 cash toward the purchase in Transaction a c. Provided services to customers on credit1 $46,925 d. Collected $39,650 cash from accounts receivable e. Recorded depreciation expense, $8,175 f. Employee salaries accrued, $15,650 g. Paid $15,650 cash to employees for salaries earned h. Accrued interest expense on long-term debt, $1,950 i. Paid a total of $25,000 on long-term debt, which includes $1.950 interest from Transaction h j. Paid $2,220 cash for l years insurance coverage in advance k. Recognized insurance expense, $1,340, that was paid in a previous period l. Sold equipment with a book value of $7,500 for $7,500 cash m. Declared cash dividend, $12,000 n. Paid cash dividend declared in Transaction m o. Purchased new equipment for $28,300 cash. p. Issued common stock for $60,000 cash q. Used $10,700 of supplies to produce revenues Summit Sales uses the indirect method to prepare its statement of cash flows. Required: 1. Construct a table similar to the one shown at the top of the next page. Analyze each transaction and indicate its effect on the fundamental accounting equation. If the transaction increases a financial statement element, write the amount of the increase preceded by a plus sign (+) in the appropriate column. If the transaction decreases a financial statement element, write the amount of the decrease preceded by a minus sign (-) in the appropriate column. 2. Indicate whether each transaction results in a cash inflow or a cash outflow in the Effect on Cash Flows column. If the transaction has no effect on cash flow, then indicate this by placing none in the Effect on Cash Flows column. 3. For each transaction that affected cash flows, indicate whether the cash flow would be classified as a cash flow from operating activities, cash flow from investing activities, or cash flow from financing activities. If there is no effect on cash flows, indicate this as a non-cash activity.arrow_forwardPost the following August transactions to T-accounts for Accounts Payable and Supplies, indicating the ending balance (assume no beginning balances in these accounts): A. purchased supplies on account, $600 B. paid vendors for supplies delivered earlier in month, $500 C. purchased supplies for cash, $450arrow_forwardIn March, T. Carter established Carter Delivery Service. The account headings are presented below. Transactions completed during the month of March follow. a. Carter deposited 25,000 in a bank account in the name of the business. b. Bought a used truck from Degroot Motors for 15,140, paying 5,140 in cash and placing the remainder on account. c. Bought equipment on account from Flemming Company, 3,450. d. Paid the rent for the month, 1,000, Ck. No. 3001 (Rent Expense). e. Sold services for cash for the first half of the month, 6,927 (Service Income). f. Bought supplies for cash, 301, Ck. No. 3002. g. Bought insurance for the truck for the year, 1,200, Ck. No. 3003. h. Received and paid the bill for utilities, 349, Ck. No. 3004 (Utilities Expense). i. Received a bill for gas and oil for the truck, 218 (Gas and Oil Expense). j. Sold services on account, 3,603 (Service Income). k. Sold services for cash for the remainder of the month, 4,612 (Service Income). l. Paid wages to the employees, 3,958, Ck. Nos. 30053007 (Wages Expense). m. Carter withdrew cash for personal use, 1,250, Ck. No. 3008. Required 1. In the equation, write the owners name above the terms Capital and Drawing. 2. Record the transactions and the balance after each transaction. Identify the account affected when the transaction involves revenues or expenses. 3. Write the account totals from the left side of the equals sign and add them. Write the account totals from the right side of the equals sign and add them. If the two totals are not equal, check the addition and subtraction. If you still cannot find the error, re-analyze each transaction.arrow_forward

- TRANSACTION ANALYSIS George Atlas started a business on June 1,20--. Analyze the following transactions for the first month of business using T accounts. Label each T account with the title of the account affected and then place the transaction letter and the dollar amount on the debit or credit side. (a) Invested cash in the business, 7,000. (b) Purchased equipment for cash, 900. (c) Purchased equipment on account, 1,500. (d) Paid cash on account for equipment purchased in transaction (c), 800. (e) Withdrew cash for personal use, 1,100.arrow_forwardPrepare journal entries to record the following transactions. Create a T-account for Cash, post any entries that affect the account, and calculate the ending balance for the account. Assume a Cash beginning balance of $37,400. A. May 12, collected balance due from customers on account, $16,000 B. June 10, purchased supplies for cash, $4,444arrow_forwardThe transactions completed by Revere Courier Company during December, the first month of the fiscal year, were as follows: Instructions 1. Enter the following account balances in the general ledger as of December 1: 2. Journalize the transactions for December, using the following journals similar to those illustrated in this chapter: cash receipts journal (p. 31), purchases journal (p. 37, with columns for Accounts Payable, Maintenance Supplies, Office Supplies, and Other Accounts), single-column revenue journal (p. 35), cash payments journal (p. 34), and two-column general journal (p. 1). Assume that the daily postings to the individual accounts in the accounts payable subsidiary ledger and the accounts receivable subsidiary ledger have been made. 3. Post the appropriate individual entries to the general ledger. 4. Total each of the columns of the special journals and post the appropriate totals to the general ledger; insert the account balances. 5. Prepare a trial balance.arrow_forward

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,