Concept explainers

Videos

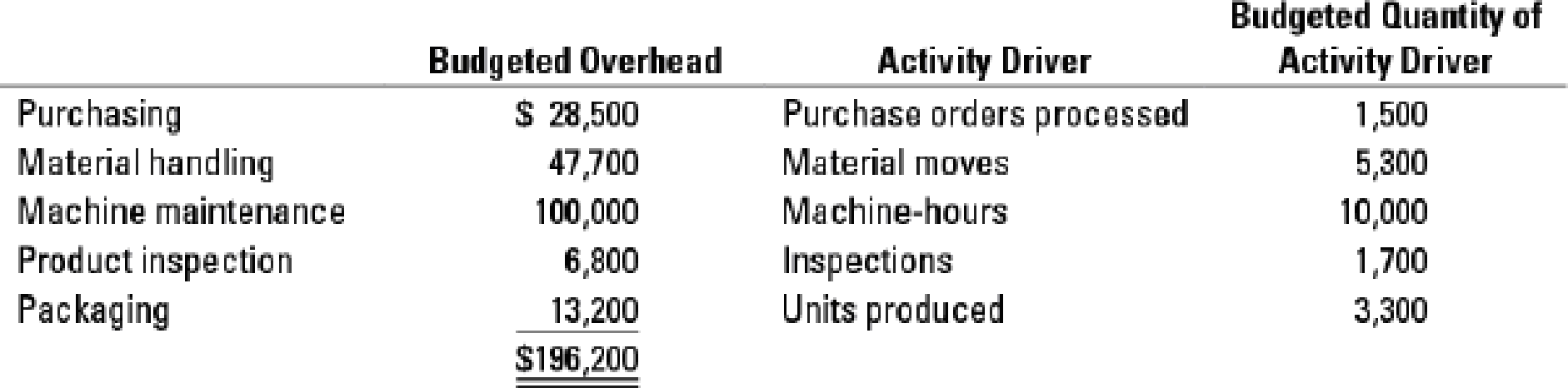

Activity-based costing. The

Information related to Job 220 and Job 330 follows. Job 220 incurs more batch-level costs because it uses more types of materials that need to be purchased, moved, and inspected relative to Job 330.

| Job 220 | Job 330 | |

| Number of purchase orders | 21 | 9 |

| Number of material moves | 18 | 6 |

| Machine-hours | 30 | 70 |

| Number of inspections | 10 | 2 |

| Units produced | 17 | 5 |

- 1. Compute the total overhead allocated to each job under a simple costing system, where overhead is allocated based on machine-hours.

Required

- 2. Compute the total overhead allocated to each job under an activity-based costing system using the appropriate activity drivers.

- 3. Explain why Melody’s Custom Framing might favor the ABC job-costing system over the simple job-costing system, especially in its bidding process.

Learn your wayIncludes step-by-step video

Chapter 5 Solutions

HORNGRENS COST ACCOUNTING W/ACCESS

Additional Business Textbook Solutions

Horngren's Accounting (12th Edition)

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Horngren's Financial & Managerial Accounting, The Managerial Chapters (6th Edition)

Intermediate Accounting

Financial Accounting

Managerial Accounting (4th Edition)

- Handy Leather, Inc., produces three sizes of sports gloves: small, medium, and large. A glove pattern is first stencilled onto leather in the Pattern Department. The stenciled patterns are then sent to the Cut and Sew Department, where the glove is cut and sewed together. Handy Leather uses the multiple production department factory overhead rate method of allocating factory overhead costs. Its factory overhead costs were budgeted as follows: The direct labor estimated for each production department was as follows: Direct labor hours are used to allocate the production department overhead to the products. The direct labor hours per unit for each product for each production department were obtained from the engineering records as follows: a. Determine the two production department factory overhead rates. b. Use the two production department factory overhead rates to determine the factory overhead per unit for each product.arrow_forwardThe management of Gwinnett County Chrome Company, described in Problem 1A, now plans to use the multiple production department factory overhead rate method. The total factory overhead associated with each department is as follows: Instructions 1. Determine the multiple production department factory overhead rates, using direct labor hours for the Stamping Department and machine hours for the Plating Department. 2. Determine the product factory overhead costs, using the multiple production department rates in (1).arrow_forwardGeneva, Inc., makes two products, X and Y, that require allocation of indirect manufacturing costs. The following data were compiled by the accountants before making any allocations: The total cost of purchasing and receiving parts used in manufacturing is 60,000. The company uses a job-costing system with a single indirect cost rate. Under this system, allocated costs were 48,000 and 12,000 for X and Y, respectively. If an activity-based system is used, what would be the allocated costs for each product?arrow_forward

- Activity-based product costing Sweet Sugar Company manufactures three products (white sugar, brown sugar, and powdered sugar) in a continuous production process. Senior management has asked the controller to conduct an activity-based costing study. The controller identified the amount of factory overhead required by the critical activities of the organization as follows: The activity bases identified for each activity are as follows: The activity-base usage quantities and units produced for the three products were determined from corporate records and are as follows: Each product requires 0.5 machine hour per unit. Instructions Determine the activity rate for each activity. Determine the total and per-unit activity cost for all three products. Round to nearest cent. Why arent the activity unit costs equal across all three products since they require the same machine time per unit?arrow_forwardTom Young, vice president of Dunn Company (a producer of plastic products), has been supervising the implementation of an activity-based cost management system. One of Toms objectives is to improve process efficiency by improving the activities that define the processes. To illustrate the potential of the new system to the president, Tom has decided to focus on two processes: production and customer service. Within each process, one activity will be selected for improvement: molding for production and sustaining engineering for customer service. (Sustaining engineers are responsible for redesigning products based on customer needs and feedback.) Value-added standards are identified for each activity. For molding, the value-added standard calls for nine pounds per mold. (Although the products differ in shape and function, their size, as measured by weight, is uniform.) The value-added standard is based on the elimination of all waste due to defective molds (materials is by far the major cost for the molding activity). The standard price for molding is 15 per pound. For sustaining engineering, the standard is 60 percent of current practical activity capacity. This standard is based on the fact that about 40 percent of the complaints have to do with design features that could have been avoided or anticipated by the company. Current practical capacity (the first year) is defined by the following requirements: 18,000 engineering hours for each product group that has been on the market or in development for five years or less, and 7,200 hours per product group of more than five years. Four product groups have less than five years experience, and 10 product groups have more. There are 72 engineers, each paid a salary of 70,000. Each engineer can provide 2,000 hours of service per year. There are no other significant costs for the engineering activity. For the first year, actual pounds used for molding were 25 percent above the level called for by the value-added standard; engineering usage was 138,000 hours. There were 240,000 units of output produced. Tom and the operational managers have selected some improvement measures that promise to reduce non-value-added activity usage by 30 percent in the second year. Selected actual results achieved for the second year are as follows: The actual prices paid per pound and per engineering hour are identical to the standard or budgeted prices. Required: 1. For the first year, calculate the non-value-added usage and costs for molding and sustaining engineering. Also, calculate the cost of unused capacity for the engineering activity. 2. Using the targeted reduction, establish kaizen standards for molding and engineering (for the second year). 3. Using the kaizen standards prepared in Requirement 2, compute the second-year usage variances, expressed in both physical and financial measures, for molding and engineering. (For engineering, explain why it is necessary to compare actual resource usage with the kaizen standard.) Comment on the companys ability to achieve its targeted reductions. In particular, discuss what measures the company must take to capture any realized reductions in resource usage.arrow_forwardActivity-based product costing Mello Manufacturing Company is a diversified manufacturer that manufactures three products (Alpha, Beta, and Omega) in a continuous production process. Senior management has asked the controller to conduct an activity-based costing study. The controller identified the amount of factory overhead required by the critical activities of the organization as follows: The activity bases identified for each activity are as follows: The activity-base usage quantities and units produced for the three products were determined from corporate records and are as follows: Each product requires 40 minutes per unit of machine time. Instructions Determine the activity rate for each activity. Determine the total and per-unit activity cost for all three products. Round to nearest cent. Why arent the activity unit costs equal across all three products since they require the same machine time per unit?arrow_forward

- John Sheng, a cost accountant at Starlet Company, is developing departmental factory overhead application rates for the companys Tooling and Fabricating departments. The budgeted overhead for each department and the data for one job are as follows: Using the departmental overhead application rates, total overhead applied to Job 231 in the Tooling and Fabricating departments will be: a. 225. b. 303. c. 537. d. 671.arrow_forwardWoolCorp is currently using the single plantwide factory overhead rate method, which uses a predetermined overhead rate based on an estimated allocation base such as direct labor hours or machine hours. The rate is computed as follows: Single Plantwide Factory Overhead Rate = (Total Budgeted Factory Overhead) ÷ (Total Budgeted Plantwide Allocation Base) WoolCorp has been using combing machine hours as its allocation base. The company would like to consider activity-based costing. In order to understand their current system better, you evaluate WoolCorp’s current method of costing for raw wool and wool yarn. The production staff has compiled the following information for you on the production of 550 pounds of either raw wool or wool yarn: FactoryOverhead Type BudgetedFactoryOverhead Sorting $25,600 Cleaning 38,400 Combing 1,200 Raw Wool Wool Yarn Hours of combing machine use required 80 20 In the following table, use combing machine hours as the allocation…arrow_forwardTime-Driven Activity-Based Costing Saratoga Company manufactures jobs to customer specifications. The company is conducting a time-driven activity-based costing study in its Purchasing Department to better understand how Purchasing Department labor costs are consumed by individual jobs. To aid the study, the company provided the following data regarding its Purchasing Department and three of its many jobs: Required: 1. Calculate the cost per minute of the resource supplied in the Purchasing Department. 2. Calculate the time-driven activity rate for each of Saratoga’s three activities. 3. Calculate the total purchasing labor costs assigned to Job X, Job Y, and Job Z.arrow_forward

- Creations is a wholesaler that bakes and decorates special occasion multi-tiered cakes, the majority of which are wedding cakes. The supervisor, Clara Cook, is questioning if using direct labor cost provides an accurate allocation base for overhead assigned to each cake. Creations uses job costing for each job which usually consists of six to nine cakes. Cakes produced for each job are delivered to local retail locations that have ordered the cakes for their respective customers. After meeting with the cost accountant, Clara identified seven activities used in the production of cakes. She has provided estimates of the annual activities along with the actual usage of activities for the jobs completed during the busiest quarter of the year presented here. Annual estimated activity Number of cakes 1,531 Number of cakes $452,000 Average direct labor cost per cake $295.23 Activities, drivers, annual estimated activity, and estimated annual overhead cost…arrow_forwardThe company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding system is fitted with every watch Quality inspection (machine) 60,000 Quality inspection (manual) 21,000 Finishing 140,000 Hand-made finishing Packaging and delivery 44,250 The…arrow_forwardHow can I get this problem resolve? High Desert Potteryworks makes a variety of pottery products that it sells to retailers. The company uses a job-order costing system in which departmental predetermined overhead rates are used to apply manufacturing overhead cost to jobs. The predetermined overhead rate in the Molding Department is based on machine-hours, and the rate in the Painting Department is based on direct labor-hours. At the beginning of the year, the company provided the following estimates: Department Molding Painting Direct labor-hours 36,500 59,800 Machine-hours 87,000 34,000 Fixed manufacturing overhead cost $ 208,800 $ 532,220 Variable manufacturing overhead per machine-hour $ 3.20 - Variable manufacturing overhead per direct labor-hour - $ 5.20 Job 205 was started on August 1 and completed on August 10. The company's cost records show the following information concerning the job: Department…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning