Concept explainers

Videos

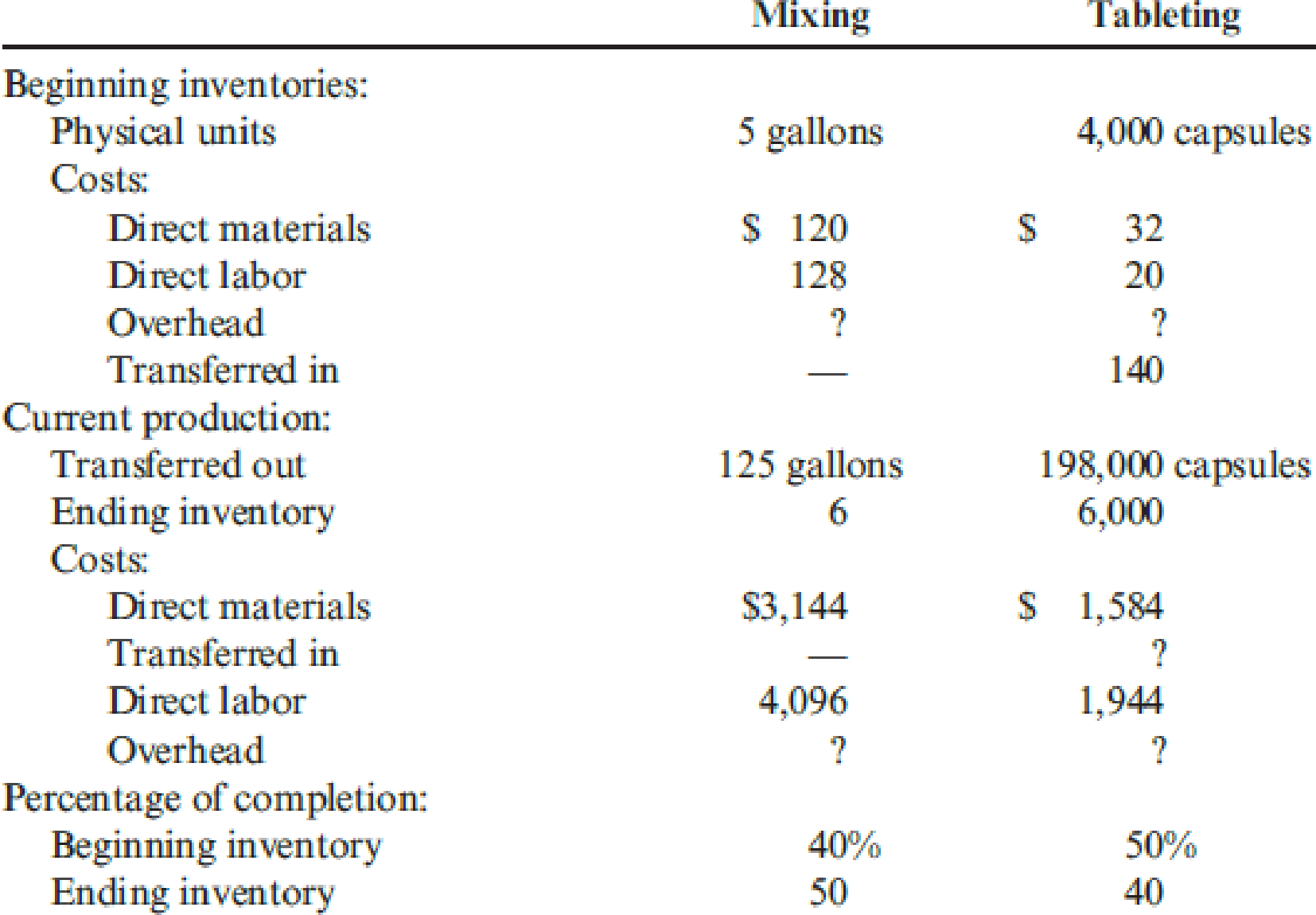

Healthway uses a process-costing system to compute the unit costs of the minerals that it produces. It has three departments: Mixing, Tableting, and Bottling. In Mixing, at the beginning of the process all materials are added and the ingredients for the minerals are measured, sifted, and blended together. The mix is transferred out in gallon containers. The Tableting Department takes the powdered mix and places it in capsules. One gallon of powdered mix converts to 1,600 capsules. After the capsules are filled and polished, they are transferred to Bottling where they are placed in bottles, which are then affixed with a safety seal and a lid and labeled. Each bottle receives 50 capsules.

During July, the following results are available for the first two departments (direct materials are added at the beginning in both departments):

Overhead in both departments is applied as a percentage of direct labor costs. In the Mixing Department, overhead is 200 percent of direct labor. In the Tableting Department, the overhead rate is 150 percent of direct labor.

Required:

- 1. Prepare a production report for the Mixing Department using the weighted average method. Follow the five steps outlined in the chapter. Round unit cost to three decimal places.

- 2. Prepare a production report for the Tableting Department. Materials are added at the beginning of the process. Follow the five steps outlined in the chapter. Round unit cost to four decimal places.

Trending nowThis is a popular solution!

Chapter 6 Solutions

EBK CORNERSTONES OF COST MANAGEMENT

- Benson Pharmaceuticals uses a process-costing system to compute the unit costs of the over-the-counter cold remedies that it produces. It has three departments: mixing, encapsulating, and bottling. In mixing, the ingredients for the cold capsules are measured, sifted, and blended (with materials assumed to be uniformly added throughout the process). The mix is transferred out in gallon containers. The encapsulating department takes the powdered mix and places it in capsules (which are necessarily added at the beginning of the process). One gallon of powdered mix converts into 1,500 capsules. After the capsules are filled and polished, they are transferred to bottling, where they are placed in bottles that are then affixed with a safety seal, lid, and label. Each bottle receives 50 capsules. During March, the following results are available for the first two departments: Overhead in both departments is applied as a percentage of direct labor costs. In the mixing department, overhead is 200% of direct labor. In the encapsulating department, the overhead rate is 150% of direct labor. Required: 1. Prepare a production report for the mixing department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to two decimal places for the unit cost.) 2. Prepare a production report for the encapsulating department using the weighted average method. Follow the five steps outlined in the chapter. (Note: Round to four decimal places for the unit cost.) 3. CONCEPTUAL CONNECTION Explain why the weighted average method is easier to use than FIFO. Explain when weighted average will give about the same results as FIFO.arrow_forwardChristie's Co. manufactures cookies. The company has two departments, Mixing and Baking. For the Baking Department, material is added at the beginning of the process. Work happens evenly throughout the process, so Conversion Costs are added evenly to the product. Once mixing is complete, the cookies pieces are immediately transferred to the Baking Department. Once the baking is complete, the final product is transferred to Finished Goods Inventory. Data for the Baking Department is as follows: Units Transfer $ DirectMaterials $ % Complete Conv Costs % Complete Opening WIP 550 $3,500 $2,800 100% $2,100 30% New units & Costs 2,000 $12,300 $8,100 $14,000 Ending WIP 680 ??? 65% Calculate the physical and equivalent units for Transferred-In, Direct Materials and Conversion Costsarrow_forwardTime Clock Shop manufactures clocks on an automated assembly line. It utilizes two cost categories: direct materials and conversion costs. Each product must pass through the Assembly Department and the Testing Department. Direct materials are added at the beginning of production, while conversion costs are allocated evenly throughout production. The company uses weighted-average costing. Data for the Assembly Department are given in the table. (Click the icon to view the table.) What is the total amount debited to the work-in-process account during the month of June at Time Clock Shop? A. $450,000 B. $2,270,000 C. $3,250,000 D. $2,000,000 E. $2,450,000 Table Work in process, beginning inventory Direct materials (100% complete) Conversion costs (50% complete) Units started during June Work in process, ending inventory Direct materials (100% complete) Conversion costs (75% complete) Work in process, beginning inventory Direct materials Conversion costs Direct materials costs added during…arrow_forward

- Mountain Springs Water Company has two departments, Purifying and Bottling. The Bottling Department had 3,740 liters in beginning work in process that were 30% completed. During the period, 61,450 liters were completed. The ending work in process had 6,590 liters that were 70% completed. Assume that Mountain Springs uses the FIFO cost flow method and that materials are added at the beginning of the process. What are the materials equivalent units of production for the period? equivalent units for materials A7 items (XƏN pe here to search 9:39 PM 53°F Cloudy a. 12/6/2021 delete pause 1 shift alt home pua ctri USE YOUR SMARTPHONE FOR du Reviews Videos Features Specs Support intel)arrow_forwardK-Briggs Company uses the FIFO method to account for the costs of production. For Crushing, the first processing department, the following equivalent units schedule has been prepared: The cost per equivalent unit for the period was as follows: The cost of beginning work in process was direct materials, 40,000; conversion costs, 30,000. Required: 1. Determine the cost of ending work in process and the cost of goods transferred out. 2. Prepare a physical flow schedule.arrow_forwardLacy, Inc., produces a subassembly used in the production of hydraulic cylinders. The subassemblies are produced in three departments: Plate Cutting, Rod Cutting, and Welding. Materials are added at the beginning of the process. Overhead is applied using the following drivers and activity rates: Other data for the Plate Cutting Department are as follows: Required: 1. Prepare a physical flow schedule. 2. Calculate equivalent units of production for: a. Direct materials b. Conversion costs 3. Calculate unit costs for: a. Direct materials b. Conversion costs c. Total manufacturing 4. Provide the following information: a. The total cost of units transferred out b. The journal entry for transferring costs from Plate Cutting to Welding c. The cost assigned to units in ending inventoryarrow_forward

- Lens Care Inc. (LCI) manufactures specialized equipment for polishing optical lenses. There are two models - one mainly used for fine eyewear (F-32) and another for lenses used in binoculars, cameras, and similar equipment (B-13).The manufacturing cost of each unit is calculated using activity-based costing, using the following manufacturing cost pools: Cost Pools Allocation Base Costing Rate Materials handling Number of parts $ 3.00 per part Manufacturing supervision Hours of machine time $ 14.86 per hour Assembly Number of parts $ 3.60 per part Machine setup Each setup $ 56.80 per setup Inspection and testing Logged hours $ 45.80 per hour Packaging Logged hours $ 19.80 per hour LCI currently sells the B-13 model for $3,125 and the F-32 model for $2,900. Manufacturing costs and activity usage for the two products are as follows: B-13 F-32 Direct materials $ 164.80 $ 75.84 Number of parts 166 126 Machine hours 8.20 4.26…arrow_forwardLens Care Inc. (LCI) manufactures specialized equipment for polishing optical lenses. There are two models - one mainly used for fine eyewear (F-32) and another for lenses used in binoculars, cameras, and similar equipment (B-13).The manufacturing cost of each unit is calculated using activity-based costing, using the following manufacturing cost pools: Cost Pools Allocation Base Costing Rate Materials handling Number of parts $ 2.50 per part Manufacturing supervision Hours of machine time $ 14.81 per hour Assembly Number of parts $ 3.35 per part Machine setup Each setup $ 56.55 per setup Inspection and testing Logged hours $ 45.55 per hour Packaging Logged hours $ 19.55 per hour LCI currently sells the B-13 model for $2,000 and the F-32 model for $1,500. Manufacturing costs and activity usage for the two products are as follows: B-13 F-32 Direct materials $ 164.55 $ 75.64 Number of parts 161 121 Machine hours 7.95 4.21…arrow_forwardLens Care Inc. (LCI) manufactures specialized equipment for polishing optical lenses. There are two models - one mainly used for fine eyewear (F-32) and another for lenses used in binoculars, cameras, and similar equipment (B-13).The manufacturing cost of each unit is calculated using activity-based costing, using the following manufacturing cost pools: Cost Pools Allocation Base Costing Rate Materials handling Number of parts $ 2.50 per part Manufacturing supervision Hours of machine time $ 14.81 per hour Assembly Number of parts $ 3.35 per part Machine setup Each setup $ 56.55 per setup Inspection and testing Logged hours $ 45.55 per hour Packaging Logged hours $ 19.55 per hour LCI currently sells the B-13 model for $2,000 and the F-32 model for $1,500. Manufacturing costs and activity usage for the two products are as follows: B-13 F-32 Direct materials $ 164.55 $ 75.64 Number of parts 161 121 Machine hours 7.95 4.21…arrow_forward

- Diamond Inc. manufactures jewelry. The company has two departments, Assembly and Polishing. For the Polishing Department, material is added when the process is 80% complete. Work happens evenly throughout the process, so Conversion Costs are added evenly to the product. Once assembly is complete, the jewelry pieces are immediately transferred to the Polishing Department. Once the polishing is complete, the final product is transferred to Finished Goods Inventory. Data for the Polishing Department is as follows: Equiv Units Ending Equiv Units Open WIP New Costs Transferred-In 200 60 $250 $15,050 Direct Materials 140 - $500 $1,500 Conversion Costs 182 42 $1,250 $4,000 Actual units Ending Inventory 60 Units Transferred out 140 Provide calculations in good form for the costs per equivalent units and the total cost reconciliation for the department. If Diamond…arrow_forwardLens Care Inc. (LCI) manufactures specialized equipment for polishing optical lenses. There are two models - one mainly used for fine eyewear (F-32) and another for lenses used in binoculars, cameras, and similar equipment (B-13).The manufacturing cost of each unit is calculated using activity-based costing, using the following manufacturing cost pools: Cost Pools Allocation Base Costing Rate Materials handling Number of parts $ 3.20 per part Manufacturing supervision Hours of machine time $ 14.88 per hour Assembly Number of parts $ 3.70 per part Machine setup Each setup $ 56.90 per setup Inspection and testing Logged hours $ 45.90 per hour Packaging Logged hours $ 19.90 per hour LCI currently sells the B-13 model for $3,575 and the F-32 model for $3,460. Manufacturing costs and activity usage for the two products are as follows: B-13 F-32 Direct materials $ 164.90 $ 75.92 Number of parts 168 128 Machine hours 8.30 4.28…arrow_forwardMuskoge Company uses a process-costing system. The company manufactures a product that isprocessed in two departments: Molding and Assembly. In the Molding Department, directmaterials are added at the beginning of the process; in the Assembly Department, additionaldirect materials are added at the end of the process. In both departments, conversion costs areincurred uniformly throughout the process. As work is completed, it is transferred out. Thefollowing table summarizes the production activity and costs for February: Molding AssemblyBeginning inventories: Physical units 10,000 8,000 Costs: Transferred in — $ 45,400 Direct materials $22,000 — Conversion costs $13,800 $ 16,700Current production: Units started 25,000 ? Units transferred out 30,000 35,000 Costs: Transferred in — ? Direct materials $ 56,250 $ 40,250 Conversion costs $103,500 $142,845 Percentage of completion: Beginning inventory 40% 55% Ending inventory 80 50Required:3. Using the FIFO method, prepare the following for…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning