FINANCIAL ACCOUNTING W/ACCESS >CI<

2nd Edition

ISBN: 9781259999024

Author: SPICELAND

Publisher: MCG CUSTOM

expand_more

expand_more

format_list_bulleted

Concept explainers

Videos

Textbook Question

Chapter 6, Problem 6.20E

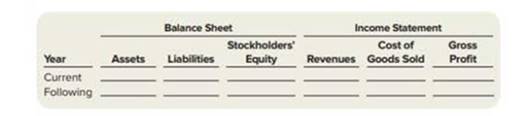

Mulligan Corporation purchases inventory on account with terms FOB shipping point. The goods are shipped on December 30, 2018, but do not reach Mulligan until January 5, 2019. Mulligan correctly records accounts payable associated with the purchase but does not include this inventory in its 2018 ending inventory count.

Required:

1. If an error has been made, explain why.

2. If an error has been made, indicate whether there is an understatement (U), overstatement (O), or no effect (N) on the reported amount of each financial statement element in the current year and following war. Ignore any tax effects.

Find financial statement effects of understatement in ending inventory (LO6-9)

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Chapter 6 Solutions

FINANCIAL ACCOUNTING W/ACCESS >CI<

Ch. 6 - 1.What is inventory? Where in the financial...Ch. 6 - Prob. 2RQCh. 6 - What is the difference among raw materials...Ch. 6 - Prob. 4RQCh. 6 - Prob. 5RQCh. 6 - What is a multiple-step income statement? What...Ch. 6 - Cheryl believes that companies report cost of...Ch. 6 - What are the three primary cost flow assumptions?...Ch. 6 - 9.Which cost flow assumption generally results in...Ch. 6 - Prob. 10RQ

Ch. 6 - Prob. 11RQCh. 6 - 12.Explain how LIFO generally results in lower...Ch. 6 - Prob. 13RQCh. 6 - Explain how freight charges, purchase returns, and...Ch. 6 - Explain the method of reporting inventory at lower...Ch. 6 - 16.How is cost of inventory determined? How is net...Ch. 6 - 17.Describe the entry to adjust from cost to net...Ch. 6 - Prob. 18RQCh. 6 - Prob. 19RQCh. 6 - How is gross profit calculated? What is the gross...Ch. 6 - 21.Explain how the sale of inventory on account is...Ch. 6 - Prob. 22RQCh. 6 - Prob. 23RQCh. 6 - Prob. 24RQCh. 6 - Understand terms related to types of companies...Ch. 6 - Prob. 6.2BECh. 6 - Calculate cost of goods sold (LO62) At the...Ch. 6 - Prob. 6.4BECh. 6 - Calculate ending inventory and cost of goods sold...Ch. 6 - Calculate ending inventory and cost of goods sold...Ch. 6 - Calculate ending inventory and cost of goods sold...Ch. 6 - Prob. 6.8BECh. 6 - Identify financial statement effects of FIFO and...Ch. 6 - Prob. 6.10BECh. 6 - Record freight charges for inventory using a...Ch. 6 - Record purchase returns of inventory using a...Ch. 6 - Prob. 6.13BECh. 6 - Prob. 6.14BECh. 6 - Prob. 6.15BECh. 6 - Prob. 6.16BECh. 6 - Prob. 6.17BECh. 6 - Prob. 6.18BECh. 6 - Record purchase returns of inventory using a...Ch. 6 - Refer to the information in BE613, but now assume...Ch. 6 - Prob. 6.21BECh. 6 - Prob. 6.22BECh. 6 - Calculate cost of goods sold (LO62) Russell Retail...Ch. 6 - Prob. 6.2ECh. 6 - Prob. 6.3ECh. 6 - Calculate inventory amounts when costs are rising...Ch. 6 - Calculate inventory amounts when costs are...Ch. 6 - Record Inventory transactions using o perpetual...Ch. 6 - Record inventory purchase and purchase return...Ch. 6 - Prob. 6.8ECh. 6 - Prob. 6.9ECh. 6 - Prob. 6.10ECh. 6 - Record transactions using a perpetual system...Ch. 6 - Record transactions using a perpetual system...Ch. 6 - Calculate inventory using lower of cost and net...Ch. 6 - Prob. 6.14ECh. 6 - Calculate cost of goods sold, the inventory...Ch. 6 - Prob. 6.16ECh. 6 - Prob. 6.17ECh. 6 - Prob. 6.18ECh. 6 - Record inventory purchases and sales using a...Ch. 6 - Mulligan Corporation purchases inventory on...Ch. 6 - Complete the accounting cycle using Inventory...Ch. 6 - Calculate ending inventory and cost of goods sold...Ch. 6 - Prob. 6.2APCh. 6 - Prob. 6.3APCh. 6 - Prob. 6.4APCh. 6 - Calculate ending inventory end cost of goods sold...Ch. 6 - Record transactions using a perpetual system,...Ch. 6 - Prob. 6.7APCh. 6 - Prob. 6.8APCh. 6 - Record transactions and prepare a partial income...Ch. 6 - Prob. 6.10APCh. 6 - Calculate ending inventory and cost of goods sold...Ch. 6 - Prob. 6.2BPCh. 6 - Prob. 6.3BPCh. 6 - Prob. 6.4BPCh. 6 - Prob. 6.5BPCh. 6 - Record transactions using a perpetual system,...Ch. 6 - Prob. 6.7BPCh. 6 - Use the inventory turnover retio end gross profit...Ch. 6 - Record transactions and prepare a partial income...Ch. 6 - Determine the effects of inventory errors using...Ch. 6 - Great Adventures (This is a continuation of the...Ch. 6 - Prob. 6.2APFACh. 6 - Prob. 6.3APFACh. 6 - Comparative Analysis American Eagle Outfitters,...Ch. 6 - Prob. 6.5APECh. 6 - Prob. 6.6APIRCh. 6 - Written Communication You have just been hired as...Ch. 6 - Prob. 6.8APEM

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Koopman Company began operations on January 1, 2018, and uses they FIFO inventory method for financial reporting and the average cost inventory method for income taxes. At the beginning of 2020, Koopman decided to switch to the average cost inventory method for financial reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the FIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Koopman is subject to a 21% income tax rate in all years; it pays the income taxes payable of a current year in the first quarter of the next year. Koopman had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Koopman had cash of 10,000, inventory of 24,000, other assets of 70,800, accounts payable of 4,500, and income taxes payable of 6,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in methods at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forwardGrimstad Company uses FIFO for internal reporting purposes and LIFO for financial reporting and income tax purposes. At the end of 2019, the following information was obtained from the inventory records: Required: 1. Prepare the necessary adjusting journal entry assuming that Grimstad converts the accounts to LIFO at the end of 2019. 2. Indicate how Grimstad would disclose the inventory value on its comparative balance sheets prepared at the end of 2019. 3. Next Level By how much would Grimstads cost of goods sold differ in 2019 if it used FIFO for external reporting?arrow_forwardSchmidt Company began operations on January 1, 2018, and used the LIFO inventory method for both financial reporting and income taxes. However, at the beginning of 2020, Schmidt decided to switch to the average cost inventory method for financial and income tax reporting. It had previously reported the following financial statement information for 2019: An analysis of the accounting records discloses the following cost of goods sold under the LIFO and average cost inventory methods: There are no indirect effects of the change in inventory method. Revenues for 2020 total 130,000; operating expenses for 2020 total 30,000. Schmidt is subject to a 21% income tax rate in all years; it pays all income taxes payable in the next quarter. Assume that any deferred tax liability was paid in the subsequent year. Schmidt had 10,000 shares of common stock outstanding during all years; it paid dividends of 1 per share in 2020. At the end of 2020, Schmidt had cash of 15,600, inventory of 34,000, other assets of 76,000, income taxes payable of 4,200, and accounts payable of 3,000. It desires to show financial statements for the current year and previous year in its 2020 annual report. Required: 1. Prepare the journal entry to reflect the change in method at the beginning of 2020. Show supporting calculations. 2. Prepare the 2020 financial statements. Notes to the financial statements are not necessary. Show supporting calculations.arrow_forward

- Company Edgar reported the following cost of goods sold but later realized that an error had been made in ending inventory for year 2021. The correct inventory amount for 2021 was 12,000. Once the error is corrected, (a) how much is the restated cost of goods sold for 2021? and (b) how much is the restated cost of goods sold for 2022?arrow_forwardAt the end of 2019, Manny Company recorded its ending inventory at 350,000 based on a physical count. During 2020, the company discovered that the correct inventory value at the end of 2019 should have been 400,000 because it made a counting error. Upon discovery of this error in 2020, what correcting journal entry will Manny make? Ignore income taxes.arrow_forwardThe following data were extracted from the accounting records of Harkins Company for the year ended April 30, 2019: a. Prepare the cost of merchandise sold section of the income statement for the year ended April 30, 2019, using the periodic inventory system. b. Determine the gross profit to be reported on the income statement for the year ended April 30, 2019. c. Would gross profit be different if the perpetual inventory system was used instead of the periodic inventory system?arrow_forward

- Refer to the information provided in RE8-4. If Paul Corporations inventory at January 1, 2019, had a cost and net realizable value of 300,000, prepare the journal entry to record the reductions to NRV for Paul Corporation assuming that Paul uses a periodic inventory system and the allowance method. Paul Corporation uses FIFO and reports the following inventory information: Assuming Paul uses a perpetual inventory system and the direct method, prepare the journal entry to record the write-down of inventory.arrow_forwardEffects of an Error in Ending Inventory Waymire Company prepared the partial income statements presented below for 2019 and 2018. During 2020, Waymires accountant discovered that ending inventory for 2018 had been understated by $6,500. Required: 1. Prepare corrected income statements for 2019 and 2018. 2. Prepare a schedule showing each financial statement item affected by the error and the amount of the error for that item (ignore the effect of income taxes). Indicate whether each error is an overstatement (+) or an understatement (-).arrow_forwardBorys Companys periodic inventory at December 31, 2019, is understated by 10,000, but purchases are correct. Johnson correctly values its 2020 ending inventory. What is the effect of this error on Boryss 2019 and 2020 financial statements?arrow_forward

- Company Elmira reported the following cost of goods sold but later realized that an error had been made in ending inventory for year 2021. The correct inventory amount for 2021 was 32,000. Once the error is corrected, (a) how much is the restated cost of goods sold for 2021? and (b) how much is the restated cost of goods sold for 2022?arrow_forwardGoods in Transit Gravais Company made two purchases on December 29, 2019. One purchase for 3,000 was shipped FOB destination, and the second for 4,000 was shipped FOB shipping point. Neither purchase had been received nor paid for on December 31, 2019. Required: Which of these purchases, if either, does Gravais include in inventory on December 31, 2019? What is the cost?arrow_forwardRefer to the information provided in RE8-4. If Paul Corporations inventory at January 1, 2019, had a cost and net realizable value of 300,000, prepare the journal entry to record the reductions to NRV for Paul Corporation assuming that Paul uses a periodic inventory system and the direct method. Paul Corporation uses FIFO and reports the following inventory information: Assuming Paul uses a perpetual inventory system and the direct method, prepare the journal entry to record the write-down of inventory.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

Cornerstones of Financial Accounting

Accounting

ISBN:9781337690881

Author:Jay Rich, Jeff Jones

Publisher:Cengage Learning

Intermediate Accounting: Reporting And Analysis

Accounting

ISBN:9781337788281

Author:James M. Wahlen, Jefferson P. Jones, Donald Pagach

Publisher:Cengage Learning

Financial Accounting

Accounting

ISBN:9781337272124

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Principles of Accounting Volume 1

Accounting

ISBN:9781947172685

Author:OpenStax

Publisher:OpenStax College

College Accounting, Chapters 1-27

Accounting

ISBN:9781337794756

Author:HEINTZ, James A.

Publisher:Cengage Learning,

Chapter 6 Merchandise Inventory; Author: Vicki Stewart;https://www.youtube.com/watch?v=DnrcQLD2yKU;License: Standard YouTube License, CC-BY

Accounting for Merchandising Operations Recording Purchases of Merchandise; Author: Socrat Ghadban;https://www.youtube.com/watch?v=iQp5UoYpG20;License: Standard Youtube License