Videos

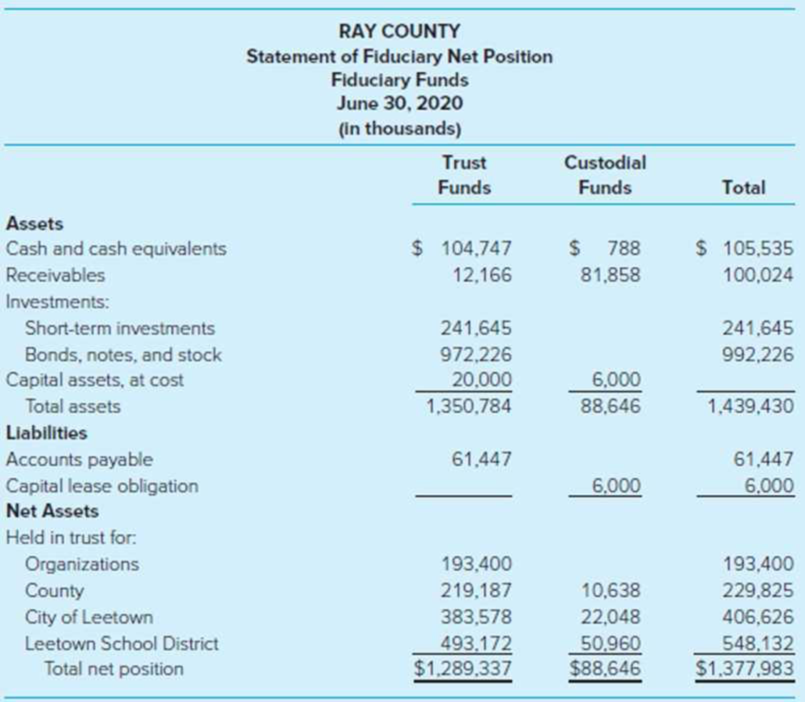

Fiduciary Financial Statements. (LO8-4) Ray County administers a tax custodial fund, an investment trust fund, and a private-purpose trust fund. The tax custodial fund acts as custodian for the county, a city within the county, and the school district within the county. Participants in the investment trust fund are the Ray County General Fund, the city, and the school district. The private-purpose trust is maintained for the benefit of a private organization located within the county. Ray County has prepared the following statement of fiduciary net position.

Required

The statement as presented is not in accordance with GASB standards. Using Illustration A2–10 (recall that the City and County of Denver statements use agency rather than custodial given they were issued prior to the change in terminology) and Illustration 8–6 as examples, identify the errors (problems) in the statement and explain how the errors should be corrected.

Want to see the full answer?

Check out a sample textbook solution

Chapter 8 Solutions

Accounting For Governmental & Nonprofit Entities

- For each of the following events or transactions, prepare the necessacry journal entries and identify the fund or funds that will be affected. 1. A governmental unit collects fees totaling $4,500 at the municipal pool. The fees are charged to recover costs of pool operation and maintenance 2. A county government that serves as a tax collection agency for all towns and cities located within the county collects county sales taxes totaling $125,000 for the month. 3. A $1,000,000 bond offering was issued, with a premium of $50,000, to subsidize the construction of a city visitor center. 4. A town receives a donation of $50,000 in bonds. The bonds should be held indefinitely, but bond income is to be donated to the local zoo. The zoo is associated with the town. 5. A central printing shop is established with a $150,000 nonreciprocal transfer from the general fund. 6. A $1,000,000 revenue bond offering was issued at par by a fund that provides water and sewer services to…arrow_forwardWilmer County provides a defined benefit pension plan for its employees. The county accounts for the pension plan in a pension trust fund, which is included in the county's basic financial statements. In the years indicated, the county engaged in the following transactions related to the pension trust fund. Prepare all necessary journal entries. Clearly indicate the fund in which the entry is being made. If no entry is needed, please write "No entry required." a) In Year 1, the pension trust fund sent billings to the general fund and the City Utility (enterprise) Fund for the actuarially determined amount of required contributions. The general fund was billed $300,000 but paid only $220,000 during the year. The enterprise fund was billed $450,000 and paid $530,000. b) In Year 2, the pension trust fund sent billings to the general fund and the City Utility Fund for the actuarially determined amount of required contributions. The general fund was billed $320,000 and paid the entire…arrow_forward6. Washington County assumed the responsibility of collecting property taxes for all governments within its boundaries. In order to reimburse the county for expenditures for administering the Tax Agency Fund, the Tax Agency Fund is to deduct 1.5 percent from the collections from the city and school district. The total amount deducted is to be added to the collections for the county and remitted to the County General Fund. You are to record the following transactions in the accounts of the Washington County Tax Agency Fund. 1. Current year tax levies to be collected by the Tax Agency Fund were:County General Fund -- $9,800,000Town of Samuels -- 6,200,000Washington County School District -- 9,600,000 2. In the first half of the year $4,120,000 was collected for the County General Fund, $3,456,000 for the Town and $4,608,000 for the School District. 3. Liabilities to all three units were recorded. Required: Record the transactions in the accounts of the Washington County Tax Agency Fund.arrow_forward

- CO G) Kirby County established a tax custodial fund to collect property taxes for the City of Kix, the City of Denton, and Kirby County Independent School District. Total tax levies of the three governments were $200,000 for the year, of which $60,000 was for the City of Kix, $40,000 for Denton, and $100,000 for the school district. The tax custodial fund charges a 2% collection fee that it transfers to the general fund of the county in order to cover costs incurred for custodial fund operations. During the year, the tax custodial fund collected and remitted $150,000 of the $200,000 levies to the various governments. Collection fees associated with the $150,000 were remitted to Kirby County's general fund prior to year-end. For the Kirby County Tax Custodial Fund, prepare the journal entries to record the taxes collected during the year and the remittances made to participating governments. (If no entry is required for a transaction or event, select No Journal Entry Required in the…arrow_forwardThe city of Belle collects property taxes for other local governments—Beau County and the Landis Independent School District (LISD). The city uses a Property Tax Collection Custodial Fund to account for its collection of property taxes for itself, Beau County, and LISD. The following transactions and events occurred for Belle's Custodial Fund. 1. Property taxes were levied for Belle ( $1,500,000), Beau County ( $750,000) and LISD ( $2,250,000). Assume taxes collected by the Custodial Fund will be paid to Belle’s General Fund. 2. Property taxes in the amount of $3,375,000 are collected. The percentage collected for each entity is in the same proportion as the original levy. 3. The amounts owed to Beau County and LISD are recognized. 4. The Custodial Fund distributes the amounts owed to the three governments. Prepare journal entries to record the above transactions and events for Belle’s Custodial Fund. If an entry affects more than one debit or credit account, enter the accounts in…arrow_forward5. Al Shahri community, located in the City of Duqm, voted to form a local improvement district to fund the construction of a new community center. The city agreed to construct the community center and administer the bond debt; however, the community was solely responsible for repaying the bond issue. To administer the bond debt, the city established the Local Improvement District Fund. Following are several events connected with the Local Improvement District Fund. 1. On June 30, 2019, the city assessed levies totaling OMR3,000,000. The levies are payable in 10 equal annual installments with 4.5 percent interest on unpaid installments. 2. All assessments for the current period were collected by June 30, 2020, as was the interest due on the unpaid installments. 3. On July 1, 2020, the first principal payment of OMR 300,000 was made to bond holders as was interest on the debt. Required Make journal entries for each of the foregoing events that affected the Local Improvement District…arrow_forward

- The City of Bagranoff holds $90,000 in cash that will be used to make a bond payment when the debt comes due early next year. The assistant treasurer had made that decision. However, just before the end of the current year, the city council formally approved using this money in this way. The city council has been designated as the highest level of decision-making authority for this government. What impact does the council’s action have on the reporting of fund financial statements? Fund balance—unassigned goes down and fund balance—restricted goes up. Fund balance—assigned goes down and fund balance—committed goes up. Fund balance—unassigned goes down and fund balance—assigned goes up. Fund balance—assigned goes down and fund balance—restricted goes up.arrow_forwardWhich of the following is an example of activities that are likely to be accounted for in a government's general fund? a. sales taxes collected by a state on behalf of counties within the state b. donations that must be kept intact, but whose income must be used to beautify parks c. property taxes levied and collected. d. electricity utilities of government that are financed by user chargesarrow_forwardThe city of Belle collects property taxes for other local governments—Beau County and the Landis Independent School District (LISD). The city uses a Property Tax Collection Custodial Fund to account for its collection of property taxes for itself, Beau County, and LISD.The following transactions and events occurred for Belle's Custodial Fund.1. Property taxes were levied for Belle ( $1,000,000), Beau County ( $500,000) andLISD ( $1,500,000). Assume taxes collected by the Custodial Fund will bepaid to Belle’s General Fund.2. Property taxes in the amount of $2,250,000 are collected. The percentage collectedfor each entity is in the same proportion as the original levy.3. The amounts owed to Beau County and LISD are recognized.4. The Custodial Fund distributes the amounts owed to the three governments.Prepare journal entries to record the above transactions and events for Belle’s Custodial Fund. If an entry affects more than one debit or credit account, enter the accounts in order of…arrow_forward

- The City of Wilmington, Delaware, has an Other Postemployment Benefit Trust Fund and a Tax Collection Agency Fund. The Preclosing Trial Balance for each of these funds as of June 30, 20X6, is as follows: City of Wilmington, Delaware Other Postemployment Benefit Trust Fund Preclosing Trial Balance June 30, 20X6 Dr. Cr. Cash and cash equivalents............................................. $ 405,476 Interest receivable.......................................................... 50,807 Investments.................................................................... 2,767,043 Employer contributions.................................................. $ 505,189 Employer contributions.................................................. 167,721 Interest income............................................................... 37,787 Increase…arrow_forwardFund A transfers $20,000 to Fund B. For each of the following, indicate whether the statement is true or false and, if false, explain why.a. If Fund A is the general fund and Fund B is an enterprise fund, nothing will be shown for this transfer on the statement of activities within the government-wide financial statements.b. If Fund A is the general fund and Fund B is a debt service fund, nothing will be shown for this transfer on the statement of activities within the government-wide financial statements.c. If Fund A is the general fund and Fund B is an enterprise fund, a $20,000 reduction will be reported on the statement of revenues, expenditures, and other changes in fund balance for the governmental funds within the fund financial statements.d. If Fund A is the general fund and Fund B is a special revenue fund (which is not considered a major fund), no changes will be shown on the statement of revenues, expenditures, and other changes in fund balance within the fund financial…arrow_forwardFund A transfers $20,000 to Fund B. For each of the following, indicate whether the statement is true or false and, if false, explain why. If Fund A is the general fund and Fund B is an enterprise fund, nothing will be shown for this transfer on the statement of activities within the government-wide financial statements. If Fund A is the general fund and Fund B is a debt service fund, nothing will be shown for this transfer on the statement of activities within the government-wide financial statements. If Fund A is the general fund and Fund B is an enterprise fund, a $20,000 reduction will be reported on the statement of revenues, expenditures, and other changes in fund balance for the governmental funds within the fund financial statements. If Fund A is the general fund and Fund B is a special revenue fund (which is not considered a major fund), no changes will be shown on the statement of revenues, expenditures, and other changes in fund balance within the fund financial statements.…arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education