Videos

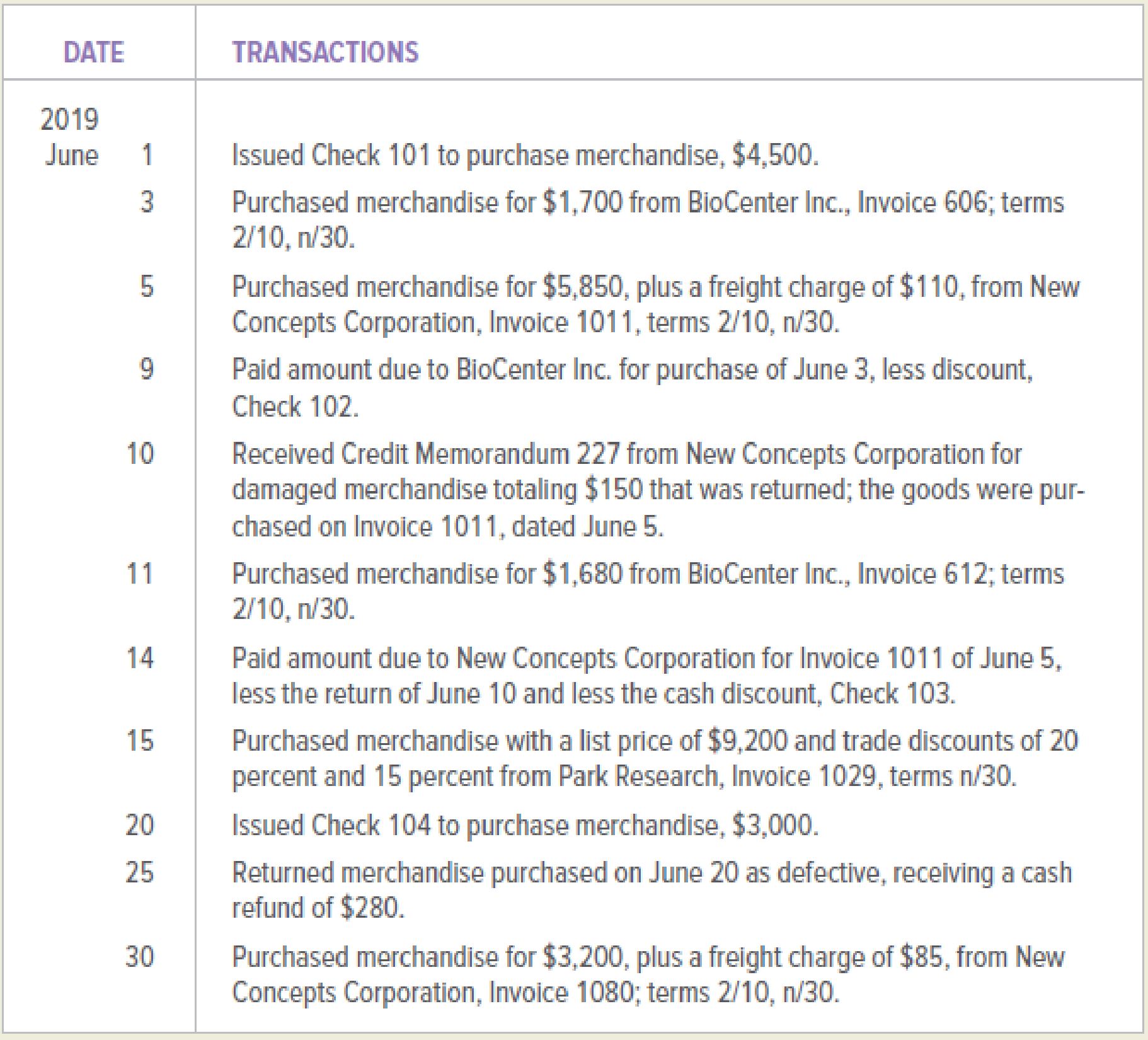

NewTech Medical Devices is a medical devices wholesaler that commenced business on June 1, 2019. NewTech Medical Devices purchases merchandise for cash and on open account. In June 2019, NewTech Medical Devices engaged in the following purchasing and cash payment activities:

INSTRUCTIONS

Journalize the transactions in a general journal. Use 1 as the journal page number.

Analyze: What was the amount of trade discounts received on the June 15 purchase from Park Research?

Record the transaction into general journal.

Explanation of Solution

Journalizing:

Journalizing refers to that process in which the transactions of an organization are recorded in a sequence. Based on the recorded entries, the accounts are posted to the relevant ledger accounts.

The general journal recording the transactions is as follows:

Recording the purchases on cash:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 1, 2019 | Purchases | 4,500 | ||

| Cash | 4,500 | |||

| (to record the inventory purchased on cash) | ||||

Table (1)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The cash account is an asset account and account balance for cash is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 3, 2019 | Purchases | 1,700 | ||

| Accounts payable/Company BC | 1,700 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (2)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • Since, the accounts payable is liability and account balance is increasing. Therefore, it is credited.

Recording the purchases on credit including freight charges:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 5, 2019 | Purchases | 5,850 | ||

| Freight In | 110 | |||

| Accounts payable/Company NC | 5,960 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (3)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The freight-in account is debited. This is because the freight-in account is an expense account and it has normal debit balance which is increasing.

- • Accounts payable is liability and balance for accounts payable is increasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 9, 2019 | Accounts payable/Company BC | 1,700 | ||

| Purchases discounts | 34 | |||

| Cash | 1,666 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (4)

- • The accounts payable is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and its increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases returned and credit memorandum received:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 10, 2019 | Accounts payable/Company NC | 150 | ||

| Purchases returns and allowances | 150 | |||

| (to record the inventory returned and credit memorandum received) | ||||

Table (5)

- • The accounts payable account is a liability account. The accounts payable account has the normal credit balance and it is decreasing. Therefore, it is debited.

- • The purchase returns and allowances account is contra expenses account. The account has the normal credit balance and increasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 11, 2019 | Purchases | 1,680 | ||

| Accounts payable/Company BC | 1,680 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (6)

- • The purchases account is debited. This is because the purchase account is an expense account and has normal debit balance which is increasing.

- • Since, the accounts payable is liability and account balance is increasing. Therefore, it is credited.

Recording the payment made:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 14, 2019 | Accounts payable/Company NC | 5,810 | ||

| Purchases discounts | 114 | |||

| Cash | 5,696 | |||

| (to record the payment made and receiving purchases discount) | ||||

Table (7)

- • The accounts payable is liability and the account balance is decreasing. Therefore, accounts payable account is debited.

- • The purchases discount account is a contra expense account. The account has the normal credit balance and its increasing. Therefore, it is credited.

- • The cash account is an asset account and the account balance is decreasing. Therefore, it is credited.

Recording the purchases on credit:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 15, 2019 | Purchases | 6,256 | ||

| Accounts payable/Company PR | 6,256 | |||

| (to record the inventory purchased on account with terms n/30) | ||||

Table (8)

- • The purchases account is debited. This is because the purchase account is an expense account and has normal debit balance which is increasing.

- • Since, the accounts payable is liability and account balance is increasing. Therefore, it is credited.

Recording the purchases on cash:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 20, 2019 | Purchases | 3,000 | ||

| Cash | 3,000 | |||

| (to record the inventory purchased on cash) | ||||

Table (9)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The cash account is credited. This is because the cash account is an asset account and account balance is decreasing.

Recording the purchases returned:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 25, 2019 | Cash | 280 | ||

| Purchases returns and allowances | 280 | |||

| (to record the inventory returned and cash received) | ||||

Table (10)

- • The cash account is debited. This is because the cash account is asset account and the account balance is increasing.

- • The purchase returns and allowances account is contra expenses account. The account has the normal credit balance and increasing. Therefore, it is credited.

Recording the purchases on credit including freight charges:

| GENERAL JOURNAL | Page 1 | |||

| Date | Account Title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| June 30, 2019 | Purchases | 3,200 | ||

| Freight In | 85 | |||

| Accounts payable/Company NC | 3,285 | |||

| (to record the inventory purchased on account with terms2/10, n/30) | ||||

Table (11)

- • The purchases account is an expense account. The purchases account has normal debit balance and the balance is increasing. Therefore, it is debited.

- • The freight In account is debited. This is because the freight In account is an expense account and it has normal debit balance which is increasing.

- • Since, the accounts payable is liability and account balance is increasing. Therefore, it is credited.

Calculation of total trade discount:

The formula to calculate the first trade discount is given below,

Substitute $9,200 for list price and 20 for percentage in the above formula.

The formula to calculate the second trade discount is given below,

Substitute $9,200 for list price, $1,840 for first trade discount and 15 for percentage in the above formula.

The formula to calculate the total trade discount is given below,

Substitute $1,840 for first trade discount and $1,104 for second trade discount in the above formula.

The total trade discount should be of $2,944 amount.

Working Note:

Calculation of purchases discount:

The purchases discounts are received by the buyer from the seller. The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company BC were agreed as 2/10, n/30. The terms 2/10, n/30 means the buyer is entitled to receive two percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $34.

Calculation of purchases discount:

The purchases discounts are received by the buyer from the seller. The purchases discounts are received by the buyer for fulfilling the terms of timely payment to seller for purchases. The terms related to paying on timely basis with the company BC were agreed as 2/10, n/30. The terms 2/10, n/30 means the buyer is entitled to receive two percent of purchase discount on the purchases amount. The buyer will be entitled to the discount only if the payment is paid within ten days after provided invoice.

The amount calculated as purchase discount would be $114.

Calculations for the purchases amount:

The seller provides the trade discount of twenty percent and the fifteen percent on the list price to the buyer. The purchases amount to be recorded by the buyer would be at the invoice price.

The purchases amount that would be calculated is $6,256.

Want to see more full solutions like this?

Chapter 8 Solutions

COLLEGE ACCOUNTING-ACCESS

- Dixon Menswear Shop purchased shirts from Colt Company on May 28, 2019, and received an invoice with a list price amount of 5,000 and payment terms of 2/10, n/30. Dixon uses the net method to record purchases. Dixon should record purchases of: a. 4,000 b. 4,900 c. 5,000 d. 5,100arrow_forwardOn January 1, Incredible Infants sold goods to Babies Inc. for $1,540, terms 30 days, and received payment on January 18. Which journal would the company use to record this transaction on the 18th? A. sales journal B. purchases journal C. cash receipts journal D. cash disbursements journal E. general journalarrow_forwardGuardian Services Inc. had the following transactions during the month of April: a. Record the June purchase transactions for Guardian Services Inc. in the following purchases journal format: b. What is the total amount posted to the accounts payable and office supplies accounts from the purchases journal for April? c. What is the April 30 balance of the Officemate Inc. creditor account assuming a zero balance on April 1?arrow_forward

- Palisade Creek Co. is a merchandising business that uses the perpetual inventory system. The account balances for Palisade Creek Co. as of May 1, 2019 (unless otherwise indicated), are as follows: During May, the last month of the fiscal year, the following transactions were completed: Instructions 1. Enter the balances of each of the accounts in the appropriate balance column of a four-column account. Write Balance in the item section and place a check mark () in the Posting Reference column. Journalize the transactions for May, starting on Page 20 of the journal. 2. Post the journal to the general ledger, extending the month-end balances to the appropriate balance columns after all posting is completed. In this problem, you are not required to update or post to the accounts receivable and accounts payable subsidiary ledgers. 3. Prepare an unadjusted trial balance. 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete (5) and (6). 5. (Optional) Enter the unadjusted trial balance on a 10-column end-of-period spreadsheet (work sheet), and complete the spreadsheet. 6. Journalize and post the adjusting entries. Record the adjusting entries on Page 22 of the journal. 7. Prepare an adjusted trial balance. 8. Prepare an income statement, a statement of owners equity, and a balance sheet. 9. Prepare and post the closing entries. Record the closing entries on Page 23 of the journal. Indicate closed accounts by inserting a line in both Balance columns opposite the closing entry. Insert the new balance in the owners capital account. 10. Prepare a post-closing trial balance.arrow_forwardThe following transactions were completed by Nelsons Boutique, a retailer, during July. Terms of sales on account are 2/10, n/30, FOB shipping point. July 3Received cash from J. Smith in payment of June 29 invoice of 350, less cash discount. 6Issued Ck. No. 1718, 742.50, to Designer, Inc., for invoice. no. 2256, recorded previously for 750, less cash discount of 7.50. July 9Sold merchandise in the amount of 250 on a credit card. Sales tax on this sale is 6%. The credit card fee the bank deducted for this transaction is 5. 10Issued Ck. No. 1719, 764.40, to Smart Style, Inc., for invoice no. 1825, recorded previously on account for 780. A trade discount of 25% was applied at the time of purchase, and Smart Style, Inc.s credit terms are 2/10, n/30. 12Received 180 cash in payment of June 20 invoice from R. Matthews. No cash discount applied. 18Received 1,575 cash in payment of a 1,500 note receivable and interest of 75. 21Voided Ck. No. 1720 due to error. 25Received and paid utility bill, 152; Ck. No. 1721, payable to City Utilities Company. 31Paid wages recorded previously for the month, 2,586, Ck. No. 1722. Required 1. Journalize the transactions for July in the cash receipts journal, the general journal (for the transaction on July 9th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forwardReview the following transactions, and prepare any necessary journal entries for Sewing Masters Inc. A. On October 3, Sewing Masters Inc. purchases 800 yards of fabric (Fabric Inventory) at $9.00 per yard from a supplier, on credit. Terms of the purchase are 1/5, n/40 from the invoice date of October 3. B. On October 8, Sewing Masters Inc. purchases 300 more yards of fabric from the same supplier at an increased price of $9.25 per yard, on credit. Terms of the purchase are 5/10, n/20 from the invoice date of October 8. C. On October 18, Sewing Masters pays cash for the amount due to the fabric supplier from the October 8 transaction. D. On October 23, Sewing Masters pays cash for the amount due to the fabric supplier from the October 3 transaction.arrow_forward

- The following transactions were completed by Nelsons Hardware, a retailer, during September. Terms on sales on account are 1/10, n/30, FOB shipping point. Sept. 4Received cash from M. Alex in payment of August 25 invoice of 275, less cash discount. 7Issued Ck. No. 8175, 915.75, to Top Tools, Inc., for invoice. no. 2256, recorded previously for 925, less cash discount of 9.25. 10Sold merchandise in the amount of 175 on a credit card. Sales tax on this sale is 8%. The credit card fee the bank deducted for this transaction is 5. 11Issued Ck. No. 8176, 653.40, to Snap Tools, Inc. for invoice no. 726, recorded previously on account for 660. A trade discount of 15% was applied at the time of purchase, and Snap Tools, Inc.s credit terms are 1/10, n/45. 15Received 95 cash in payment of August 20 invoice from N. Johnson. No cash discount applied. 19Received 1,165 cash in payment of a 1,100 note receivable and interest of 65. 22Voided Ck. No. 8177 due to error. 26Received and paid telephone bill, 62; Ck. No. 8178, payable to Southern Telephone Company. 30Paid wages recorded previously for the month, 3,266, Ck. No. 8179. Required 1. Journalize the transactions for September in the cash receipts journal, the general journal (for the transaction on Sept. 10th), or the cash payments journal as appropriate. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals. Prove the equality of debit and credit totals.arrow_forwardA retailer returns $400 worth of inventory to a manufacturer and receives a full refund. What accounts recognize this return before the retailer remits payment to the manufacturer? A. accounts payable, merchandise inventory B. accounts payable, cash C. cash, merchandise inventory D. merchandise inventory, cost of goods soldarrow_forwardGomez Company sells electrical supplies on a wholesale basis. The balances of the accounts as of April 1 have been recorded in the general ledger in your Working Papers and CengageNow. The following transactions took place during April of this year: Apr. 1 Sold merchandise on account to Myers Company, invoice no. 761, 570.40. 5 Sold merchandise on account to L. R. Foster Company, invoice no. 762, 486.10. 6 Issued credit memo no. 50 to Myers Company for merchandise returned, 40.70. 10 Sold merchandise on account to Diaz Hardware, invoice no. 763, 293.35. 14 Sold merchandise on account to Brooks and Bennett, invoice no. 764, 640.16. 17 Sold merchandise on account to Powell and Reyes, invoice no. 765, 582.12. 21 Issued credit memo no. 51 to Brooks and Bennett for merchandise returned, 68.44. 24 Sold merchandise on account to Ortiz Company, invoice no. 766, 652.87. 26 Sold merchandise on account to Diaz Hardware, invoice no. 767, 832.19. 30 Issued credit memo no. 52 to Diaz Hardware for damage to merchandise, 98.50. Required 1. Record these sales of merchandise on account in the sales journal. If using Working Papers, use page 39. Record the sales returns and allowances in the general journal. If using Working Papers, use page 74. 2. Immediately after recording each transaction, post to the accounts receivable ledger. 3. Post the amounts from the general journal daily. Post the sales journal amount as a total at the end of the month: Accounts Receivable 113, Sales 411, Sales Returns and Allowances 412. 4. Prepare a schedule of accounts receivable. Compare the balance of the Accounts Receivable controlling account with the total of the schedule of accounts receivable.arrow_forward

- Review the following transactions, and prepare any necessary journal entries for Renovation Goods. A. On May 12, Renovation Goods purchases 750 square feet of flooring (Flooring Inventory) at $3.00 per square foot from a supplier, on credit. Terms of the purchase are 2/10, n/30 from the invoice date of May 12. B. On May 15, Renovation Goods purchases 200 measuring tapes (Tape Inventory) at $5.75 per tape from a supplier, on credit. Terms of the purchase are 4/15, n/60 from the invoice date of May 15. C. On May 22, Renovation Goods pays cash for the amount due to the flooring supplier from the May 12 transaction. D. On June 3, Renovation Goods pays cash for the amount due to the tape supplier from the May 15 transaction.arrow_forwardReview the following transactions and prepare any necessary journal entries for Lands Inc. A. On December 10, Lands Inc. contracts with a supplier to purchase 450 plants for its merchandise inventory, on credit, for $12.50 each. Credit terms are 4/15, n/30 from the invoice date of December 10. B. On December 28, Lands pays the amount due in cash to the supplier.arrow_forwardPreston Company sells candy wholesale, primarily to vending machine operators. Terms of sales on account are 2/10, n/30, FOB shipping point. The following transactions involving cash receipts and sales of merchandise took place in May of this year: Required 1. Journalize the transactions for May in the cash receipts journal and the sales journal. Assume the periodic inventory method is used. 2. If you are using Working Papers, total and rule the journals and prove the equality of the debit and credit totals.arrow_forward

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781305088436Author:Carl Warren, Jim Reeve, Jonathan DuchacPublisher:Cengage Learning College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning,

College Accounting, Chapters 1-27AccountingISBN:9781337794756Author:HEINTZ, James A.Publisher:Cengage Learning, Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub

College Accounting (Book Only): A Career ApproachAccountingISBN:9781337280570Author:Scott, Cathy J.Publisher:South-Western College Pub College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning

College Accounting (Book Only): A Career ApproachAccountingISBN:9781305084087Author:Cathy J. ScottPublisher:Cengage Learning