Concept explainers

Videos

Activity-Based Costing versus Traditional Costing

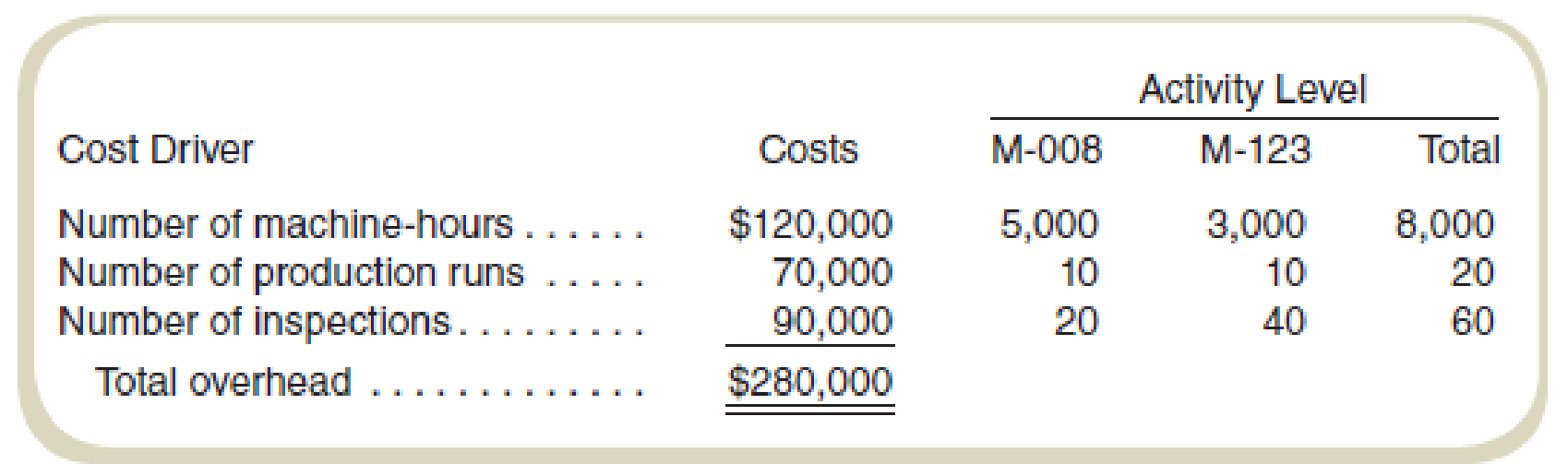

Doaktown Products manufactures fishing equipment for recreational uses. The Miramichi plant produces the company’s two versions of a special reel used for river fishing. The two models are the M-008, a basic reel, and the M-123, a new and improved version. Cost accountants at company headquarters have prepared costs for the two reels for the most recent period. The plant manager is concerned. The cost report does not coincide with her intuition about the relative costs of the two models. She has asked you to review the cost accounting and help her prepare a response to headquarters.

Manufacturing

Management determined that overhead costs are caused by three cost drivers. These drivers and their costs for last year were as follows:

Required

- a. How much overhead will be assigned to each product if these three cost drivers are used to allocate overhead? What is the total cost per unit produced for each product?

- b. How much of the overhead will be assigned to each product if direct labor cost is used to allocate overhead? What is the total cost per unit produced for each product?

- c. Draft a memo for the plant manager explaining why the two systems result in different costs along with your recommendation for which costing system to use.

Want to see the full answer?

Check out a sample textbook solution

Chapter 9 Solutions

Gen Combo Fundamentals Of Cost Accounting; Connect Access Card

- Functional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the companys market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way the backpacks were produced. After some discussion, the two managers decided that the problem had to be connected to the addition of the duffel-bag line. Upon investigation, they were informed that the only real change in product-costing procedures was in the way overhead costs are assigned. A two-stage procedure was now in use. First, overhead costs are assigned to the two producing departments, Patterns and Finishing. Second, the costs accumulated in the producing departments are assigned to the two products by using direct labor hours as a driver (the rate in each department is based on direct labor hours). The managers were assured that great care was taken to associate overhead costs with individual products. So that they could construct their own example of overhead cost assignment, the controller provided them with the information necessary to show how accounting costs are assigned to products: The controller remarked that the cost of operating the accounting department had doubled with the addition of the new product line. The increase came because of the need to process additional transactions, which had also doubled in number. During the first year of producing duffel bags, the company produced and sold 100,000 backpacks and 25,000 duffel bags. The 100,000 backpacks matched the prior years output for that product. Required: (Note: Round rates and unit cost to the nearest cent.) 1. CONCEPTUAL CONNECTION Compute the amount of accounting cost assigned to a backpack before the duffel-bag line was added by using a plantwide rate approach based on units produced. Is this assignment accurate? Explain. 2. Suppose that the company decided to assign the accounting costs directly to the product lines by using the number of transactions as the activity driver. What is the accounting cost per unit of backpacks? Per unit of duffel bags? 3. Compute the amount of accounting cost assigned to each backpack and duffel bag by using departmental rates based on direct labor hours. 4. CONCEPTUAL CONNECTION Which way of assigning overhead does the best jobthe functional-based approach by using departmental rates or the activity-based approach by using transactions processed for each product? Explain. Discuss the value of ABC before the duffel-bag line was added.arrow_forwardActivity-based costing and product cost distortion The management of Four Finger Appliance Company in Exercise 14 has asked you to use activity-based costing instead of direct labor hours to allocate factory overhead costs to the two products. You have determined that 81,000 of factory overhead from each of the production departments can be associated with setup activity (162,000 in total). Company records indicate that blenders required 135 setups, while the toaster ovens required only 45 setups. Each product has a production volume of 7,500 units. Determine the three activity rates (assembly, test and pack, and setup). Determine the total factory overhead and factory overhead per unit allocated to each product using the activity rates in (A).arrow_forwardFunctional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the company's market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way…arrow_forward

- Functional-Based versus Activity-Based Costing For years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindo added a line of duffel bags. With this addition, the company began assigning overhead costs by using departmental rates. (Prior to this, the company used a predetermined plantwide rate based on units produced.) Surprisingly, after the addition of the duffel-bag line and the switch to departmental rates, the costs to produce the backpacks increased, and their profitability dropped. Josie, the marketing manager, and Steve, the production manager, both complained about the increase in the production cost of backpacks. Josie was concerned because the increase in unit costs led to pressure to increase the unit price of backpacks. She was resisting this pressure because she was certain that the increase would harm the company's market share. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way…arrow_forwardActivity-Based Costing and Conventional Costs ComparedHickory Grill Company manufactures two types of cooking grills: the Gas Cooker and the Charcoal Smoker. The Cooker is a premium product sold in upscale outdoor shops; the Smoker is sold in major discount stores. Following is information pertaining to the manufacturing costs for the current month. Gas Cooker Charcoal Smoker Units 1,000 5,000 Number of batches 50 10 Number of batch moves 80 20 Direct materials $90,000 $150,000 Direct labor $20,000 $25,000 Manufacturing overhead follows: Activity Cost Cost Driver Materials acquisition and inspection $80,800 Amount of direct materials cost Materials movement 16,200 Number of batch moves Scheduling 36,000 Number of batches $133,000 a. Determine the total and per-unit costs of manufacturing the Gas Cooker and Charcoal Smoker for the month, assuming all manufacturing overhead is assigned on the basis of direct labor dollars.Round…arrow_forwardActivity-Based Life-Cycle Costing Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $600 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system:Variable conversion activity rate: $110 per direct labor hourMaterial usage rate: $15 per partABC system:Labor usage: $20 per direct labor hourMaterial usage (direct materials): $25 per partMachining: $80 per machine hourPurchasing activity: $150 per purchase orderSetup activity:…arrow_forward

- Production-Based Costing versus Activity-Based Costing,Assigning Costs to Activities, Resource DriversWillow Company produces lawnmowers. One of its plants produces two versions of mowers:a basic model and a deluxe model. The deluxe model has a sturdier frame, a higher horsepowerengine, a wider blade, and mulching capability. At the beginning of the year, the following datawere prepared for this plant: Facility-level costs are allocated in proportion to machine hours (provides a measure oftime the facility is used by each product). Receiving and materials handling use three inputs:two forklifts, gasoline to operate the forklift, and three operators. The three operators are paid asalary of $40,000 each. The operators spend 25% of their time on the receiving activity and 75%on moving goods (materials handling). Gasoline costs $3 per move. Depreciation amounts to$8,000 per forklift per year.Required:(Note: Round answers to two decimal places.)1. Calculate the cost of the materials…arrow_forwardActivity-Based Life-Cycle Costing Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $500 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system:Variable conversion activity rate: $100 per direct labor hourMaterial usage rate: $20 per partABC system:Labor usage: $15 per direct labor hourMaterial usage (direct materials): $20 per partMachining: $85 per machine hourPurchasing activity: $170 per purchase orderSetup activity:…arrow_forwardFunctional-Based versus Activity-Based CostingFor years, Tamarindo Company produced only one product: backpacks. Recently, Tamarindoadded a line of duffel bags. With this addition, the company began assigning overhead costsby using departmental rates. (Prior to this, the company used a predetermined plantwide ratebased on units produced.) Surprisingly, after the addition of the duffel-bag line and the switchto departmental rates, the costs to produce the backpacks increased, and their profitabilitydropped.Josie, the marketing manager, and Steve, the production manager, both complainedabout the increase in the production cost of backpacks. Josie was concerned because theincrease in unit costs led to pressure to increase the unit price of backpacks. She was resistingthis pressure because she was certain that the increase would harm the company’s marketshare. Steve was receiving pressure to cut costs also, yet he was convinced that nothing different was being done in the way the backpacks…arrow_forward

- Activity-Based Supplier Costing Bowman Company manufactures cooling systems. Bowman produces all the parts necessary for its product except for one electronic component, which is purchased from two local suppliers: Manzer Inc. and Buckner Company. Both suppliers are reliable and seldom deliver late; however, Manzer sells the component for $89 per unit, while Buckner sells the same component for $86. Bowman purchases 80% of its components from Buckner because of its lower price. The total annual demand is 4,000,000 components. To help assess the cost effect of the two components, the following data were collected for supplier-related activities and suppliers: Required: 1. Calculate the cost per component for each supplier, taking into consideration the costs of the supplier-related activities and using the current prices and sales volume. ( Note : Round the unit cost to two decimal places.) 2. Suppose that Bowman loses $4,000,000 in sales per year because it develops a poor…arrow_forwardActivity-Based Supplier Costing Bowman Company manufactures cooling systems. Bowman produces all the parts necessary for its product except for one electronic component, which is purchased from two local suppliers: Manzer Inc. and Buckner Company. Both suppliers are reliable and seldom deliver late; however, Manzer sells the component for $89 per unit, while Buckner sells the same component for $86. Bowman purchases 80% of its components from Buckner because of its lower price. The total annual demand is 4,000,000 components. To help assess the cost effect of the two components, the following data were collected for supplier-related activities and suppliers: I. Activity Data Activity Cost Inspecting components (sampling only) $630,000 Reworking products (due to failed component) 7,770,000 Warranty work (due to failed component) 8,770,000 II. Supplier Data Manzer Inc. Buckner Company Unit purchase price $89 $86 Units purchased 800,000 3,200,000 Sampling hours*…arrow_forwardActivity-Based Supplier Costing Bowman Company manufactures cooling systems. Bowman produces all the parts necessary for its product except for one electronic component, which is purchased from two local suppliers: Manzer Inc. and Buckner Company. Both suppliers are reliable and seldom deliver late; however, Manzer sells the component for $89 per unit, while Buckner sells the same component for $86. Bowman purchases 80% of its components from Buckner because of its lower price. The total annual demand is 4,000,000 components. To help assess the cost effect of the two components, the following data were collected for supplier-related activities and suppliers: I. Activity Data Activity Cost Inspecting components (sampling only) $605,000 Reworking products (due to failed component) 7,570,000 Warranty work (due to failed component) 10,270,000 II. Supplier Data Manzer Inc. Buckner Company Unit purchase price $89 $86 Units purchased 800,000 3,200,000 Sampling hours*…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning