Concept explainers

Videos

Choosing an Activity-Based Costing System

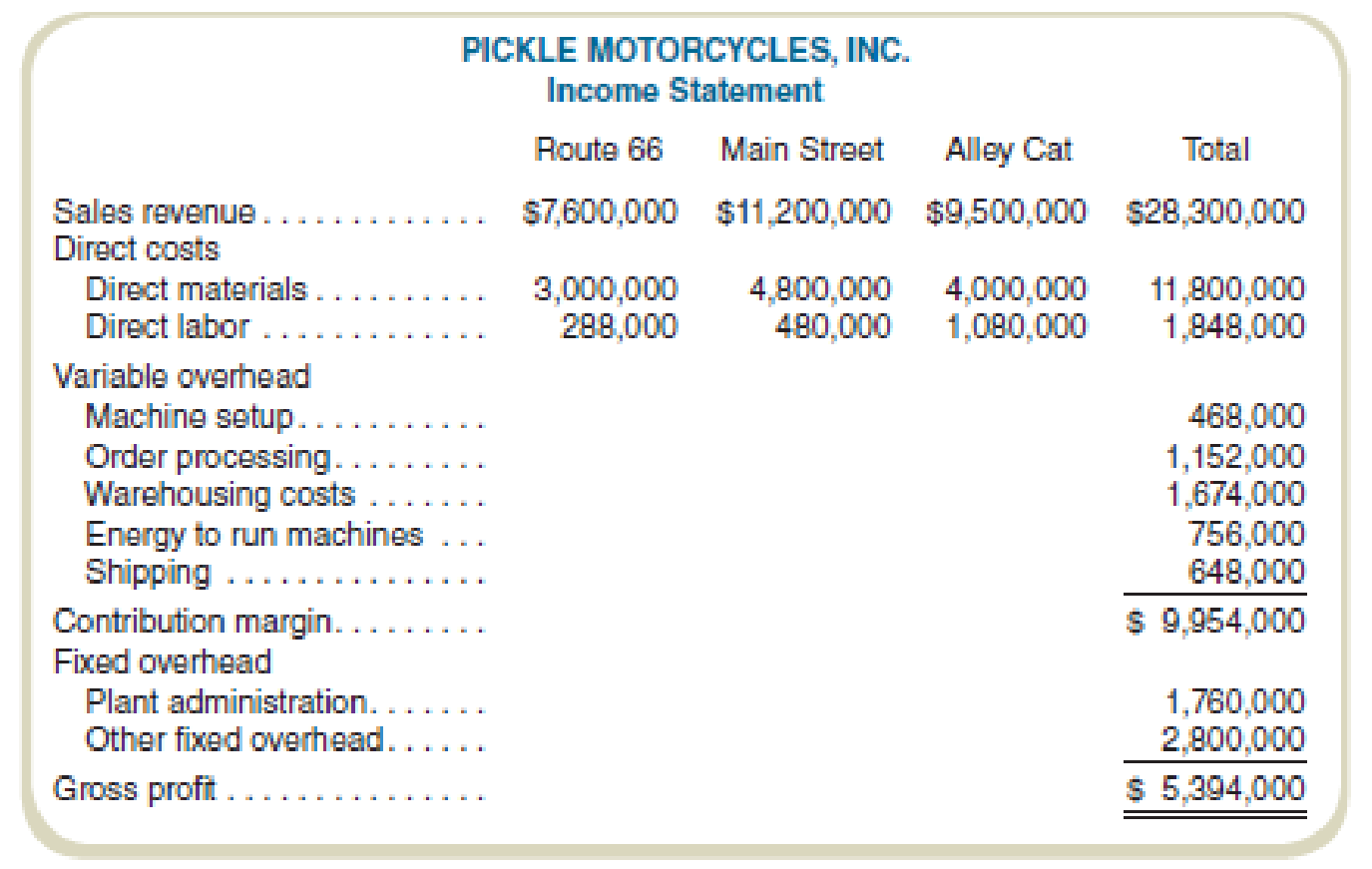

Pickle Motorcycles, Inc. (PMI), manufactures three motorcycle models: a cruising bike (Route 66), a street bike (Main Street), and a starter model (Alley Cat). Because of the different materials used, production processes for each model differ significantly in terms of machine types and time requirements. Once parts are produced, however, assembly time per unit required for each type of bike is similar. For this reason, PMI allocates

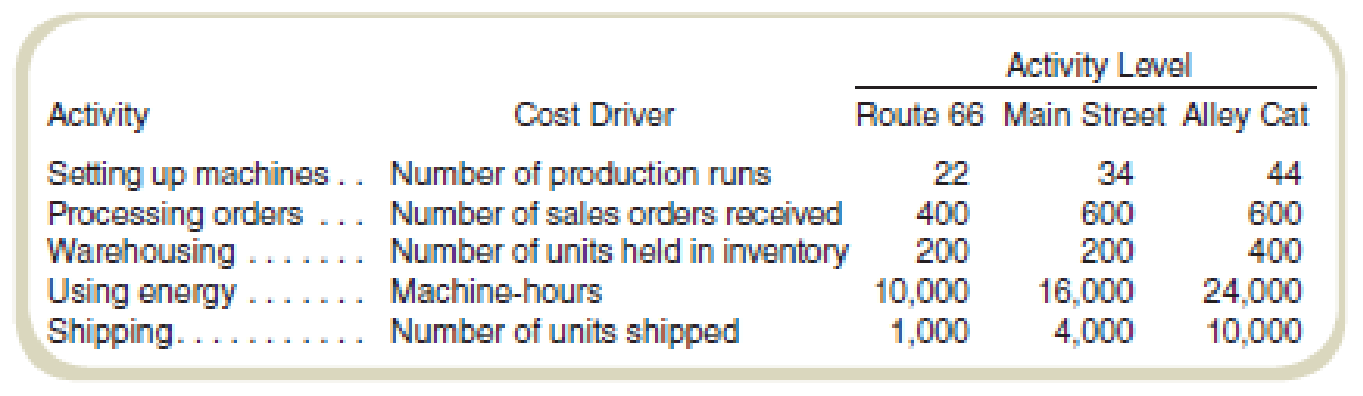

PMI’s chief financial officer (CFO) hired a consultant to recommend cost allocation bases. The consultant recommended the following:

The consultant found no basis for allocating the plant administration and other fixed overhead costs and recommended that these not be applied to products.

Required

- a. Using machine-hours to allocate production overhead, complete the income statement for Pickle Motorcycles. (See the “using energy” activity for machine-hours.) Do not attempt to allocate plant administration or other fixed overhead.

- b. Complete the income statement using the bases recommended by the consultant.

- c. How might activity-based costing result in better decisions by Pickle Motorcycles’s management?

- d. After hearing the consultant’s recommendations, the CFO decides to adopt activity-based costing but expresses concern about not allocating some of the overhead to the products (plant administration and other fixed overhead). In the CFO’s view, “Products have to bear a fair share of all overhead or we won’t be covering all of our costs.” How would you respond to this comment?

a.

Complete the income statement.

Explanation of Solution

Traditional labor-hour based costing method:

Traditional labor-hour based costing method assumes that the direct labor-hour is the base allocation of the process. The process of allocation of overhead computes the indirect overhead with respect to the labor-hours only.

Complete the income statement:

| Particulars | Route 66 | Main street | Alley cat | Total |

| Sales revenue | $7,600,000 | $11,200,000 | $9,500,000 | $28,300,000 |

| Direct costs: | ||||

| Direct materials | $3,000,000 | $4,800,000 | $4,000,000 | $11,800,000 |

| Direct labor | $288,000 | $480,000 | $1,080,000 | $1,848,000 |

|

Variable overhead | $939,600 | $1,503,360 | $2,255,040 | $4,698,000 |

| Contribution margin | $3,372,400 | $4,416,640 | $2,164,960 | $9,954,000 |

| Fixed overhead: | ||||

| Plant admin | $1,760,000 | |||

| Other | $2,800,000 | |||

| Gross profit | $5,394,000 |

Table: (1)

Compute the rate of variable overhead:

Thus, the rate of variable overhead is $93.96.

b.

Complete the income statement using the recommendations.

Explanation of Solution

Activity-based costing (ABC):

Activity-based costing is the method of costing where the overhead cost is assigned to various products. This method of costing establishes the relationship between the manufacturing overhead costs and the activities. The relationship is then implemented for the allocation of indirect costs to the products.

Complete the income statement using the recommendations:

| Particulars | Route 66 | Main street | Alley cat | Total |

| Sales revenue | $7,600,000 | $11,200,000 | $9,500,000 | $28,300,000 |

| Direct costs: | ||||

| Direct materials | $3,000,000 | $4,800,000 | $4,000,000 | $11,800,000 |

| Direct labor | $288,000 | $480,000 | $1,080,000 | $1,848,000 |

| Variable overhead | ||||

|

Machine setup | $102,960 | $159,120 | $205,920 | $468,000 |

|

Order processing | $288,000 | $432,000 | $432,000 | $1,152,000 |

|

Warehousing | $418,500 | $418,500 | $837,000 | $1,674,000 |

|

Energy | $151,200 | $241,920 | $362,880 | $756,000 |

|

Shipping | $43,200 | $172,800 | $432,000 | $648,000 |

|

Contribution margin | $3,308,140 | $4,495,660 | $2,150,200 | $9,954,000 |

| Fixed overhead | ||||

| Plant admin | $1,760,000 | |||

| Other | $2,800,000 | |||

| Gross profit | $5,394,000 |

Table: (2)

Compute the applicable rate:

| Particulars | Total cost | Total respective units | Applicable rate |

| Machine setup | $468,000 | 100 | $4,680 |

| Order processing | $1,152,000 | 1,600 | $720 |

| Warehousing | $1,674,000 | 800 | $2,093 |

| Energy | $756,000 | 50,000 | $15 |

| Shipping | $648,000 | 15,000 | $43 |

Table: (3)

c.

Determine how activity-based costing result is better.

Explanation of Solution

Activity-based costing (ABC):

Activity-based costing is the method of costing where the overhead cost is assigned to various products. This method of costing establishes the relationship between the manufacturing overhead costs and the activities. The relationship is then implemented for the allocation of indirect costs to the products.

Traditional labor-hour based costing method:

Traditional labor-hour based costing method assumes that the direct labor-hour is the base allocation of the process. The process of allocation of overhead computes the indirect overhead with respect to the labor-hours only.

The relevance of ABC method:

The ABC method gives a better and detailed cost structure of the process. A better cost report will provide a better assessment of the costing. The information that is churned out enables the management to take appropriate decisions.

d.

Provide the appropriate response to the statement in question.

Explanation of Solution

Activity-based costing (ABC):

Activity-based costing is the method of costing where the overhead cost is assigned to various products. This method of costing establishes the relationship between the manufacturing overhead costs and the activities. The relationship is then implemented for the allocation of indirect costs to the products.

The statement in question:

“Products have to bear a fair share of all overhead, or we won’t be covering all of our costs.”

The relevance of statement with respect to the ABC:

There are few costs that do not correlate with volume or any other base of activity. Allocation of such costs would make information distorted. Preferable means to record these costs would require determination of contribution margin from each product.

Want to see more full solutions like this?

Chapter 9 Solutions

FUNDAMENTALS OF COST ACCOUNTING

- Production-Based Costing versus Activity-Based Costing, Assigning Costs to Activities, Resource Drivers Willow Company produces lawnmowers. One of its plants produces two versions of mowers: a basic model and a deluxe model. The deluxe model has a sturdier frame, a higher horsepower engine, a wider blade, and mulching capability. At the beginning of the year, the following data were prepared for this plant: Additionally, the following overhead activity costs are reported: Facility-level costs are allocated in proportion to machine hours (provides a measure of time the facility is used by each product). Receiving and materials handling use three inputs: two forklifts, gasoline to operate the forklift, and three operators. The three operators are paid a salary of 40,000 each. The operators spend 25% of their time on the receiving activity and 75% on moving goods (materials handling). Gasoline costs 3 per move. Depreciation amounts to 8,000 per forklift per year. Required: (Note: Round answers to two decimal places.) 1. Calculate the cost of the materials handling activity. Label the cost assignments as driver tracing or direct tracing. Identify the resource drivers. 2. Calculate the cost per unit for each product by using direct labor hours to assign all overhead costs. 3. Calculate activity rates, and assign costs to each product. Calculate a unit cost for each product, and compare these costs with those calculated in Requirement 2. 4. Calculate consumption ratios for each activity. 5. CONCEPTUAL CONNECTION Explain how the consumption ratios calculated in Requirement 4 can be used to reduce the number of rates. Calculate the rates that would apply under this approach.arrow_forwardTri-bikes manufactures two different levels of bicycles: the Standard and the Extreme. The total overhead of $300,000 has traditionally been allocated by direct labor hours, with 150.000 hours for the Standard and 50,000 hours for the Extreme. After analyzing and assigning costs to two cost pools, it was determined that machine hours is estimated to have $200,000 of overhead, with 4,000 hours used on the Standard product and 1,000 hours used on the Extreme product. k was also estimated that the setup cost pool would have $100000 of overhead, with 1,000 hours for the Standard and 1,500 hours for the Extreme. What is the overhead rate per product, under traditional and under ABC costing?arrow_forwardFisico Company produces exercise bikes. One of its plants produces two versions: a standard model and a deluxe model. The deluxe model has a wider and sturdier base and a variety of electronic gadgets to help the exerciser monitor heartbeat, calories burned, distance traveled, etc. At the beginning of the year, the following data were prepared for this plant: Additionally, the following overhead activity costs are reported: Required: 1. Calculate the cost per unit for each product using direct labor hours to assign all overhead costs. 2. Calculate activity rates and determine the overhead cost per unit. Compare these costs with those calculated using the unit-based method. Which cost is the most accurate? Explain.arrow_forward

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardBumblebee Mobiles manufactures a line of cell phones. The management has identified the following overhead costs and related cost drivers for the coming year. The following were incurred in manufacturing two of their cell phones, Bubble and Burst, during the first quarter. REQUIREMENT Review the worksheet called ABC that follows these requirements. You have been asked to determine the cost of each product using an activity-based cost system. Note that the problem information is already entered into the Data Section of the ABC worksheet.arrow_forwardSilven Company has identified the following overhead activities, costs, and activity drivers for the coming year: Silven produces two models of cell phones with the following expected activity demands: 1. Determine the total overhead assigned to each product using the four activity drivers. 2. Determine the total overhead assigned to each model using the two most expensive activities. The costs of the two relatively inexpensive activities are allocated to the two expensive activities in proportion to their costs. 3. Using ABC as the benchmark, calculate the percentage error and comment on the accuracy of the reduced system. Explain why this approach may be desirable.arrow_forward

- Wrappers Tape makes two products: Simple and Removable. It estimates it will produce 369,991 units of Simple and 146,100 of Removable, and the overhead for each of its cost pools is as follows: It has also estimated the activities for each cost driver as follows: Â How much is the overhead allocated to each unit of Simple and Removable?arrow_forwardJulio produces two types of calculator, standard and deluxe. The company is currently using a traditional costing system with machine hours as the cost driver but is considering a move to activity-based costing. In preparing for the possible switch, Julio has identified two cost pools: materials handling and setup. The collected data follow: Standard Model Deluxe Model Number of machine hours 26,500 31,500 Number of material moves 625 925 Number of setups 85 575 Total estimated overhead costs are $382,020, of which $186,000 is assigned to the material handling cost pool and $196,020 is assigned to the setup cost pool Im not understadning how to find the over head costsarrow_forwardActivity-Based Life-Cycle Costing Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $600 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system:Variable conversion activity rate: $110 per direct labor hourMaterial usage rate: $15 per partABC system:Labor usage: $20 per direct labor hourMaterial usage (direct materials): $25 per partMachining: $80 per machine hourPurchasing activity: $150 per purchase orderSetup activity:…arrow_forward

- Activity-Based Life-Cycle Costing Kagle design engineers are in the process of developing a new “green” product, one that will significantly reduce impact on the environment and yet still provide the desired customer functionality. Currently, two designs are being considered. The manager of Kagle has told the engineers that the cost for the new product cannot exceed $500 per unit (target cost). In the past, the Cost Accounting Department has given estimated costs using a unit-based system. At the request of the Engineering Department, Cost Accounting is providing both unit- and activity-based accounting information (made possible by a recent pilot study producing the activity-based data). Unit-based system:Variable conversion activity rate: $100 per direct labor hourMaterial usage rate: $20 per partABC system:Labor usage: $15 per direct labor hourMaterial usage (direct materials): $20 per partMachining: $85 per machine hourPurchasing activity: $170 per purchase orderSetup activity:…arrow_forwardVaughn, Inc produces two types of gas grill: a family model and deluxe model. Vaughn’s controller has decided to use overhead rate based on direct labor costs. The president of the company recently heard of activity based on direct labor costs. The president of the company recently heard of activity- based costing and wants to see hoe the results would differ if this system were used. Two activity cost pools were developed: machine setup. Presented below is information related to the company’s operation: Family model Deluxe Model Direct Labor Cost: $78,000 $156,000 Machine Hours: 2,000 2,000 Setup Hours: 200 800 Total estimated overhead costs are $468,000. Overhead cost allocated to the machining activity cost pool is $280,800 and $187,200 is allocated to the machine setup activity cost pool. Compute the overhead rates using the activity-bases costing approach.arrow_forwardPrivott, Inc., manufactures and sells two products: Product Z9 and Product N0. The company is considering adopting an activity-based costing system with the following activity cost pools, activity measures, and expected activity: Estimated Expected Activity Activity Cost Pools Activity Measures Overhead Cost Product Z9 Product N0 Total Labor-related DLHs $ 327,018 6,700 3,300 10,000 Product testing tests 47,247 550 650 1,200 Order size MHs 472,608 4,300 4,600 8,900 $ 846,873 The activity rate for the Labor-Related activity cost pool under activity-based costing is closest to: Multiple Choice A. $72.69 per DLH B. $705.73 per DLH C. $85.90 per DLH D. $32.70 per DLHarrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning