Concept explainers

Videos

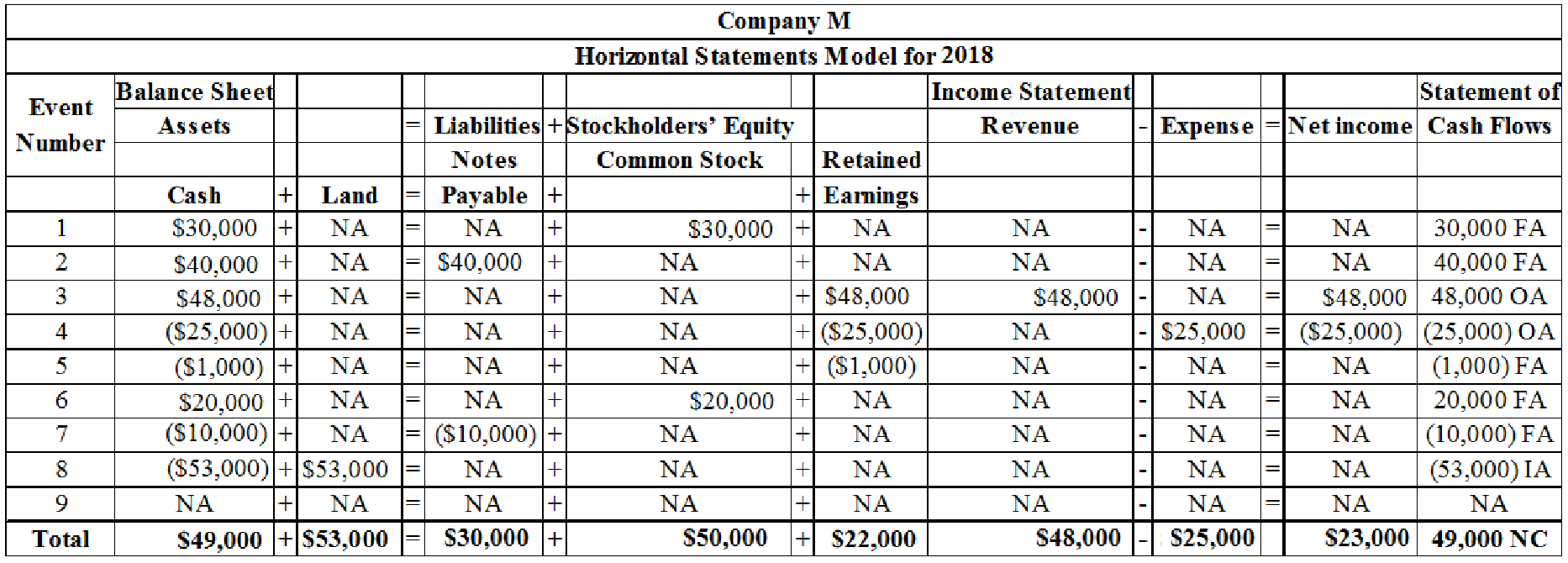

Maben Company was started on January 1, 2018, and experienced the following events during its first year of operation:

- 1. Acquired $30,000 cash from the issue of common stock.

- 2. Borrowed $40,000 cash from National Bank.

- 3. Earned cash revenues of $48,000 for performing services.

- 4. Paid cash expenses of $25,000.

- 5. Paid a $1,000 cash dividend to the stockholders.

- 6. Acquired an additional $20,000 cash from the issue of common stock.

- 7. Paid $10,000 cash to reduce the principal balance of the bank note.

- 8. Paid $53,000 cash to purchase land.

- 9. Determined that the market value of the land is $75,000.

Required

- a. Record the preceding transactions in the horizontal statements model. Also, in the Cash Flows column, classify the cash flows as operating activities (OA), investing activities (IA), or financing activities (FA). The first event is shown as an example.

- b. Determine the amount of total assets that Maben would report on the December 31, 2018,

balance sheet . - c. Identify the asset source transactions and related amounts for 2018.

- d. Determine the net income that Maben would report on the 2018 income statement. Explain why dividends do not appear on the income statement.

- e. Determine the net cash flows from operating activities, financing activities, and investing activities that Maben would report on the 2018 statement of cash flows.

- f. Determine the percentage of assets that were provided by investors, creditors, and earnings. Round to three decimal places.

- g. What is the balance in the

Retained Earnings account immediately after Event 3 is recorded?

a.

Prepare horizontal analysis to show the affect of each event in the balance sheet, income statement, and statement of cash flows.

Explanation of Solution

Accounting event: An accounting event is a cost-effective event that affects assets, liabilities, or stockholders’ equity of a Company.

Income statement: Income statement is the financial statement of a company which shows all the revenues earned and expenses incurred by the company over a period of time.

Balance sheet: Balance Sheet is one of the financial statements that summarize the assets, the liabilities, and the Shareholder’s equity of a company at a given date. It is also known as the statement of financial status of the business.

Statement of cash flows: Statement of cash flows is one among the financial statement of a Company statement that shows aggregate data of all cash inflows and cash outflows that is received and paid by the Company from its ongoing business operations.

Operating activities: Operating activities refer to the normal activities of a company to carry out the business. The examples for operating activities are purchase of inventory, payment of salary, sales, and others.

Investing activities: Investing activities refer to the activities carried out by a company for acquisition of long term assets. The examples for investing activities are purchase of equipment, long term investment, sale of land, and others.

Financing activities: Financing activities refer to the activities carried out by a company to mobilize funds to carry out the business activities. The examples for financing activities are purchase of bonds, issuance of common shares, and others.

Horizontal statements model: In this model the analysts will analyse the effect of the transactions on balance sheet, income statement, and statement of cash flows.

Prepare horizontal analysis:

Table (1)

Note: FA represents financing activity, OA represents operating activity, IA represents investing activity, NA represents no affect and NC represents net change.

b.

Report the amount of total assets that is reported on the December 31, 2016, balance sheet.

Explanation of Solution

Balance sheet:

Balance is the financial statement that reports a company’s resources (assets) and claims of creditors (liabilities) and stockholders (stockholders’ equity) over those resources. The resources of the company are assets which include money contributed by stockholders and creditors. Hence, the main elements of the balance sheet are assets, liabilities, and stockholders’ equity.

Calculate the total amount of assets:

Therefore, the total amount of cash reported on the balance sheet is $102,000.

c.

Identify the asset source transactions and related amounts for 2016.

Explanation of Solution

Assets source transaction: Transaction that acquires the assets from primary sources of the business is called as assets source transaction. Assets source transactions increase the value of assets account, and increase the corresponding liabilities or stockholder’s equity account. The increased assets account is recorded with the debit entry, and increased liabilities or stockholder’s equity account is recorded with credit entry.

The asset source transaction are identifed as follows along with the related amounts:

| Sources of Assets | Amount ($) |

| 1. Issue of stock | 30,000 |

| 2. Cash from loan | 40,000 |

| 3. Cash from revenue | 48,000 |

| 6. Issue of stock | 20,000 |

| Total Sources of Assets | 138,000 |

Table (2)

d.

Calculate the net income that is reported on the income statement for the 2016 and Explain the reason for the non appearance of dividends in the income statement.

Explanation of Solution

The amount of net income reported is $23,000 (refer table (1)). But dividend does not appear in the income statement because it is no considered as an expense.

e.

Calculate the net cash flows from operating activities, financing activities, and investing activities.

Explanation of Solution

Operating activities: Operating activities refer to the normal activities of a company to carry out the business. The examples for operating activities are purchase of inventory, payment of salary, sales, and others.

Investing activities: Investing activities refer to the activities carried out by a company for acquisition of long term assets. The examples for investing activities are purchase of equipment, long term investment, sale of land, and others.

Financing activities: Financing activities refer to the activities carried out by a company to mobilize funds to carry out the business activities. The examples for financing activities are purchase of bonds, issuance of common shares, and others.

The net cash flows from operating activities, financing activities, and investing activities are calculated as follows:

| Operating Activities: | |

| Particulars | Amount ($) |

| Cash from revenue | 48,000 |

| Cash paid for expenses | (25,000) |

| Net Cash Flow from Operating Activities | $23,000 |

Table (3)

| Investing Activities: | |

| Particulars | Amount ($) |

| Cash paid to purchase land | (53,000) |

| Net Cash Flow from Investing Activities | ($53,000) |

Table (4)

| Financing Activities: | |

| Particulars | Amount ($) |

| Cash from stock issue ($30,000 + $20,000) | 50,000 |

| Cash from loan | 40,000 |

| Paid cash dividend | (1,000) |

| Cash paid on loan principal | (10,000) |

| Net Cash Flow from Financing Activities | $79,000 |

Table (5)

f.

Calculate the percentage of assets that were provided by investors, creditors and earnings.

Explanation of Solution

Stockholders’ equity to asset ratio:

Stockholders ‘equity to asset ratio is the ratio that measures the difference between total asset and stockholders ‘equity of the company. Stockholders’ equity ratio reflects the amount of assets that can be claimed by the stockholders in proportion to the value of shares owned by them.

Percentage of total assets acquired from investors is calculated as follows:

Note: Total

Debt to Asset Ratio:

Debt to asset ratio is the ratio that measures the difference between total asset and total liability of the company. Debt ratio reflects the finance strategy of the company. It is used to evaluate company’s ability to pay its debts. Higher debt ratio implies the higher financial risk.

Percentage of assets acquired from creditors is calculated as follows:

Note: Total

Return on assets:

Return on assets is the financial ratio which determines the amount of net income earned by the business with the use of total assets owned by it. It indicates the magnitude of the company’s earnings with relative to its total assets.

Percentage of total assets acquired from retained earnings:

Note: Total

Therefore the percentage of total assets acquired from investors is 49.0%, the percentage of total assets acquired from creditors is 29.4% and the percentage of total assets from retained earnings is 21.6%.

g.

Calculate the balance in the retained accounts

Explanation of Solution

Retained earnings:

Retained earnings are the portion of earnings kept by the business for the purpose of reinvestments, payment of debts, or for future growth.

Balance in the retained earnings account is as follows:

The balance in the account of retained earnings is zero. The revenue earned is recorded in the revenue accounts and not recorded in the retained earnings account.

Want to see more full solutions like this?

Chapter 1 Solutions

Survey Of Accounting

- Analyzing Transactions. Using the analytical framework, indicate the effect of the following related transactions of a firm. a. January 1: Issued 10,000 shares of common stock for 50,000. b. January 1: Acquired a building costing 35,000, paying 5,000 in cash and borrowing the remainder from a bank. c. During the year: Acquired inventory costing 40,000 on account from various suppliers. d. During the year: Sold inventory costing 30,000 for 65,000 on account. e. During the year: Paid employees 15,000 as compensation for services rendered during the year. f. During the year: Collected 45,000 from customers related to sales on account. g. During the year: Paid merchandise suppliers 28,000 related to purchases on account. h. December 31: Recognized depreciation on the building of 7,000 for financial reporting. Depreciation expense for income tax purposes was 10,000. i. December 31: Recognized compensation for services rendered during the last week in December but not paid by year-end of 4,000. j. December 31: Recognized and paid interest on the bank loan in Part b of 2,400 for the year. k. Recognized income taxes on the net effect of the preceding transactions at an income tax rate of 40%. Assume that the firm pays cash immediately for any taxes currently due to the government.arrow_forwardProvide journal entries to record each of the following transactions. For each, identify whether the transaction represents a source of cash (S), a use of cash (U), or neither (N). A. Declared and paid to shareholders, a dividend of $24,000. B. Issued common stock at par value for $12,000 cash. C. Sold a tract of land that had cost $10,000, for $16,000. D. Purchased a company truck, with a note payable of $38,000. E. Collected $8,000 from customer accounts receivable.arrow_forwardProvide journal entries to record each of the following transactions. For each, identify whether the transaction represents a source of cash (S), a use of cash (U), or neither (N). A. Paid $22,000 cash on bonds payable. B. Collected $12,600 cash for a note receivable. C. Declared a dividend to shareholders for $16,000, to be paid in the future. D. Paid $26,500 to suppliers for purchases on account. E. Purchased treasury stock for $18,000 cash.arrow_forward

- Krespy Corp. has a cash balance of $7,500 before the following transactions occur: A. received customer payments of $965 B. supplies purchased on account $435 C. services worth $850 performed, 25% is paid in cash the rest will be billed D. corporation pays $275 for an ad in the newspaper E. bill is received for electricity used $235. F. dividends of $2,500 are distributed What is the balance in cash after these transactions are journalized and posted?arrow_forwardNet income and dividends The income statement of a corporation for the month of November indicates a net income of $90,000. During the same period, $100,000 in cash dividends were paid. Would it be correct to say that the business incurred a net loss of $10,000 during the month? Discuss.arrow_forwardProvide journal entries to record each of the following transactions. For each, also identify *the appropriate section of the statement of cash flows, and s utility bill, $1,500arrow_forward

- Visual Inspection Noble Companys accounting records provided the following changes in account balances and other information for 2019: Additional information: Net income was 9,900. Dividends were declared and paid. Land was sold for 1,700. No land was purchased. A building was purchased for 23,000. No buildings and equipment were sold. Bonds payable were issued at the end of the year. Two hundred shares of stock were issued for 15 per share. The beginning cash balance was 4,800. Required: Using visual inspection, prepare a 2019 statement of cash flows for Noble.arrow_forwardMontana Incorporated began the year with a retained earnings balance of $50,000. The company paid a total of $5,000 in dividends and experienced a net loss of $25,000 this year. What is the ending retained earnings balance?arrow_forwardAssume that as of January 1, 20Y8, Sylvester Con- suiting has total assets of $500,000 and total assets of $150,000. As of December 31, 20Y8, Sylvester has total liabilities of $200,000 and total stockholders’ equity of $400,000. (a) What was Sylvester’s stockholders’ equity as of January 1, 20Y8? (b) Assume that Sylvester did not pay any dividends during 20Y8. What was the amount of net income for 20Y8?arrow_forward

- Farmington Corporation began the year with a retained earnings balance of $20,000. The company paid a total of $3,000 in dividends and earned a net income of $60,000 this year. What is the ending retained earnings balance?arrow_forwardComprehensive The following are Farrell Corporations balance sheets as of December 31, 2019, and 2018, and the statement of income and retained earnings for the year ended December 31, 2019: Additional information: a. On January 2, 2019, Farrell sold equipment costing 45,000, with a book value of 24,000, for 19,000 cash. b. On April 2, 2019, Farrell issued 1, 000 shares of common stock for 23,000 cash. c. On May 14, 2019, Farrell sold all of its treasury stock for 25,000 cash. d. On June 1, 2019, Farrell paid 50, 000 to retire bonds with a face value (and book value) of 50, 000. e. On July 2, 2019, Farrell purchased equipment for 63, 000 cash. f. On December 31, 2019, land with a fair market value of 150,000 was purchased through the issuance of a long-term note in the amount of 150,000. The note bears interest at the rate of 15% and is due on December 31, 2021. g. Deferred taxes payable represent temporary differences relating to the use of accelerated depreciation methods for income tax reporting and the straight-line method for financial statement reporting. Required: 1. Prepare a spreadsheet to support a statement of cash flows for Farrell for the year ended December 31, 2019, based on the preceding information. 2. Prepare the statement of cash flows. (Appendix 21.1) Spreadsheet and Statement Refer to the information for Farrell Corporation in P21-13. Required: 1. Using the direct method for operating cash flows, prepare a spreadsheet to support a 2019 statement of cash flows. (Hint: Combine the income statement and December 31, 2019, balance sheet items for the adjusted trial balance. Use a retained earnings balance of 291,000 in this adjusted trial balance.) 2. Prepare the statement of cash flows. (A separate schedule reconciling net income to cash provided by operating activities is not necessary.)arrow_forwardComprehensive The following are Farrell Corporations balance sheets as of December 31, 2019, and 2018, and the statement of income and retained earnings for the year ended December 31, 2019: Additional information: a. On January 2, 2019, Farrell sold equipment costing 45,000, with a book value of 24,000, for 19,000 cash. b. On April 2, 2019, Farrell issued 1,000 shares of common stock for 23,000 cash. c. On May 14, 2019, Farrell sold all of its treasury stock for 25,000 cash. d. On June 1, 2019, Farrell paid 50,000 to retire bonds with a face value (and book value) of 50,000. e. On July 2, 2019, Farrell purchased equipment for 63,000 cash. f. On December 31, 2019. land with a fair market value of 150,000 was purchased through the issuance of a long-term note in the amount of 150,000. The note bears interest at the rate of 15% and is due on December 31, 2021. g. Deferred taxes payable represent temporary differences relating to the use of accelerated depreciation methods for income tax reporting and the straight-line method for financial statement reporting. Required: 1. Prepare a spreadsheet to support a statement of cash flows for Farrell for the year ended December 31, 2019, based on the preceding information. 2. Prepare the statement of cash flows.arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning

Financial Accounting: The Impact on Decision Make...AccountingISBN:9781305654174Author:Gary A. Porter, Curtis L. NortonPublisher:Cengage Learning Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning

Financial Reporting, Financial Statement Analysis...FinanceISBN:9781285190907Author:James M. Wahlen, Stephen P. Baginski, Mark BradshawPublisher:Cengage Learning