Concept explainers

Videos

Cost Data for Managerial Purposes—Budgeting

Refer to Exhibit 1.5. Assume that Carmen’s Cookies is preparing a budget for the month ending September 30. Management prepares the budget by starting with the actual results for April that appear in Exhibit 1.5. Then, management considers what the differences in costs will be between April and September.

Management expects cookie sales to be 20 percent greater in September than in April, and it expects all food costs (e.g., flour, eggs) to be 20 percent higher in September than in April because of the increase in cookie sales. Management expects “other” labor costs to be 25 percent higher in September than in April, partly because more labor will be required in September and partly because employees will get a pay raise. The manager will get a pay raise that will increase the salary from $3,000 in April to $3,500 in September. Utilities will be 5 percent higher in September than in April. Rent will be the same in September as in April.

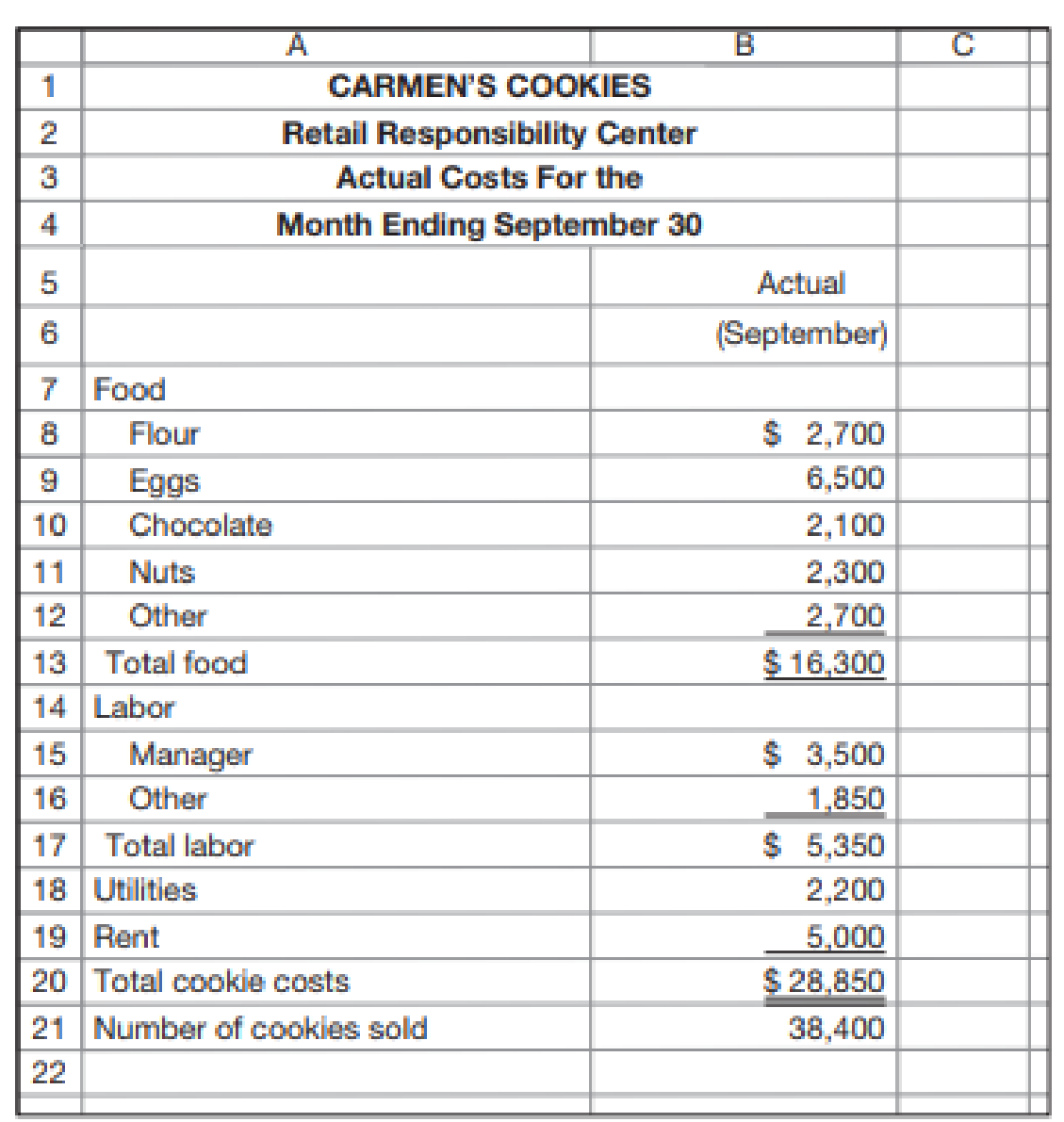

Now, fast forward to early October and assume the following actual results occurred in September:

Required

- a. Prepare a statement like the one in Exhibit 1.5 that compares the budgeted and actual costs for September.

- b. Suppose that you have limited time to determine why actual costs are not the same as budgeted costs. Which three cost items would you investigate to see why actual and budgeted costs are different? Why would you choose those three costs?

a.

Prepare a statement like the one in Exhibit 1.5 that compares the budgeted and actual costs for September.

Explanation of Solution

Budgeted costs: The costs which are pre-determined at the beginning of the year are termed as the budgeted costs. These costs are considered as standard during the year while performing business activities.

Actual costs: The costs which are actually incurred during the year are termed as the actual costs. These costs are the actual figure of costs for the particular period.

The statement that compares the budgeted and actual costs for September is as follows:

| Company C | |||

| Retail Responsibility Center | |||

| Budgeted versus Actual Costs | |||

| For the Month Ending September 30 | |||

| Actual | Budget | Difference | |

| (September) | (September) | ||

| Food | |||

| Flour | $ 2,700 | $ 2,520 (1) | $ 180 |

| Eggs | $ 6,500 | $ 6,240 (2) | $ 260 |

| Chocolate | $ 2,100 | $ 2,400 (3) | $ (300) |

| Nuts | $ 2,300 | $ 2,400 (4) | $ (100) |

| Other | $ 2,700 | $ 2,640 (5) | $ 60 |

| Total food | $ 16,300 | $ 16,200 | $ 100 |

| Labor: | |||

| Manager | $ 3,500 | $ 3,500 | $ - |

| Other | $ 1,850 | $ 1,875 (6) | $ (25) |

| Total labor cost | $ 5,350 | $ 5,375 | $ (25) |

| Utilities | $ 2,200 | $ 1,890 | $ 310 |

| Rent | $ 5,000 | $ 5,000 | $ - |

| Total cost of cookies | $ 28,850 | $ 28,465 | $ 385 |

| Number of cookies sold | 38,400 | 38,400 | |

Working note 1:

Compute the budgeted cost of flour in September:

Working note 2:

Compute the budgeted cost of eggs for September:

Working note 3:

Compute the budgeted cost of chocolate for September:

Working note 4:

Compute the budgeted cost of nuts for September:

Working note 5:

Compute the other budgeted costs for September:

Working note 6:

Compute the other labor costs for September:

b.

Identify the three cost items which would be investigated to see why actual and budgeted costs are different and why those three costs would be chosen.

Explanation of Solution

The three cost items which would be investigated to see why actual and budgeted costs are different are as follows:

- • The cost of chocolates

- • The cost of eggs

- • The cost of utilities

The three items are having more difference between the budgeted and the actual figures. Thus, these items should be investigated, and the reason for such difference should be observed.

Want to see more full solutions like this?

Chapter 1 Solutions

FUNDAMENTALS OF COST ACCOUNTING

- Budgeted income statement and supporting budgets The budget director of Gold Medal Athletic Co., with the assistance of the controller, treasurer, production manager, and sales manager, has gathered the following data for use in developing the budgeted income statement for March: Estimated sales for March: Estimated inventories at March 1: Desired inventories at March 31: Direct materials used in production: Anticipated cost of purchases and beginning and ending inventory of direct materials: Direct labor requirements: Estimated factory overhead costs for March: Estimated operating expenses for March: Estimated other revenue and expense for March: Estimated tax rate: 30% Instructions Prepare a sales budget for March. Prepare a production budget for March. Prepare a direct materials purchases budget for March. Prepare a direct labor cost budget for March. Prepare a factory overhead cost budget for March. Prepare a cost of goods sold budget for March. Work in process at the beginning of March is estimated to be 15,300, and work in process at the end of March is desired to be 14,800. Prepare a selling and administrative expenses budget for March. Prepare a budgeted income statement for March.arrow_forwardUsing High-Low to Calculate Predicted Total Variable Cost and Total Cost for Budgeted Output Refer to the information for Pizza Vesuvio on the previous page. Assume that this information was used to construct the following formula for monthly labor cost. TotalLaborCost=5,237+(7.40EmployeeHours) Required: Assume that 675 employee hours are budgeted for the month of September. Use the total labor cost formula for the following calculations: 1. Calculate total variable labor cost for September. 2. Calculate total labor cost for September.arrow_forwardSales, production, direct materials purchases, and direct labor cost budgets The budget director of Gourmet Grill Company requests estimates of sales, production, and other operating data from the various administrative units every month. Selected information concerning sales and production for July is summarized as follows: Estimated sales for July by sales territory: Estimated inventories at July 1: Desired inventories at July 31: Direct materials used in production: Anticipated purchase price for direct materials: Direct labor requirements: Instructions Prepare a sales budget for July. Prepare a production budget for July. Prepare a direct materials purchases budget for July. Prepare a direct labor cost budget for July.arrow_forward

- Using High-Low to Calculate Predicted Total Variable Cost and Total Cost for Budgeted Output Refer to the information for Speedy Petes above. Assume that this information was used to construct the following formula for monthly delivery cost. TotalDeliveryCost=41,850+(12.00NumberofDeliveries) Required: Assume that 3,000 deliveries are budgeted for the following month of January. Use the total delivery cost formula for the following calculations: 1. Calculate total variable delivery cost for January. 2. Calculate total delivery cost for January.arrow_forwardBudget performance reports for cost centers Partially completed budget performance reports for Delmar Company, a manufacturer of light duty motors, follow: a. Complete the budget performance reports by determining the correct amounts for the lettered spaces. b. Compose a memo to Randi Wilkes, vice president of production for Delmar Company, explaining the performance of the production division for June.arrow_forwardGHT Tech Inc. sells electronics over the Internet. The Consumer Products Division is organized as a cost center. The budget for the Consumer Products Division for the month ended January 31 is as follows: During January, the costs incurred in the Consumer Products Division were as follows: Instructions 1. Prepare a budget performance report for the director of the Consumer Products Division for the month of January. 2. For which costs might the director be expected to request supplemental reports?arrow_forward

- Preparing a performance report Use the flexible budget prepared in P7-6 for the 29,000-unit level of activity and the actual operating results listed below for the 29,000- unit level. Required: 1. Prepare a performance report. 2. List the major reasons why the actual operating income at 29,000 units differs from the master budget operating income at 30,000 units in Figure 7-12. 3. Given the level at which the company operated, how was its cost control? Item Direct materials: Direct labor:arrow_forwardDigital Solutions Inc. uses flexible budgets that are based on the following data: Prepare a flexible selling and administrative expenses budget for October for sales volumes of 500,000, 750,000, and 1,000,000.arrow_forwardBudgeted income statement and supporting budgets for three months Bellaire Inc. gathered the following data for use in developing the budgets for the first quarter (January, February, March) of its fiscal year: Estimated sales at 125 per unit: Estimated finished goods inventories: Work in process inventories are estimated to be insignificant (zero). Estimated direct materials inventories: Manufacturing costs: Selling expenses: Instructions Prepare the following budgets using one column for each month and a total column for the first quarter, as shown for the sales budget: Prepare a sales budget for March. Prepare a production budget for March. Prepare a direct materials purchases budget for March. Prepare a direct labor cost budget for March. Prepare a factory overhead cost budget for March. Prepare a cost of goods sold budget for March. Prepare a selling and administrative expenses budget for March. Prepare a budgeted income statement with budgeted operating income for March.arrow_forward

- Preparing a performance report Use the flexible budget prepared in P7-6 for the 31,000-unit level and the actual operating results listed below for the 31,000-unit level. Required: 1. Prepare a performance report. 2. List the major reasons why the actual operating income at 31,000 units differs from the master budget operating income at 30,000 units in Figure 7-12. 3. Given the level at which the company operated, how was its cost control? Item Direct materials: Direct labor:arrow_forwardFlexible budget for factory overhead Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month. The predetermined overhead rate is based on normal capacity. Required: 1. Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of 80%, 90%, and 110% of normal capacity. Also determine the predetermined factory overhead rate at each level of volume in both units and direct labor hours. 2. Prepare a flexible budget for production levels of 80%, 90%, and 110%, assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions. (Hint: Set up a third category for semi-variable expenses.) a. At 110% of capacity, another supervisor will be needed at a salary of 24,000 annually. b. At 80% of capacity, the repairs expense will drop to one-half of the amount at 100% capacity. c. At 80% of capacity, one part-time maintenance worker, earning 10,000 a year, will be laid off. d. At 110% of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was 12,000, it has a 10-year life, and straight-line depreciation will be taken.arrow_forwardStatic budget versus flexible budget The production supervisor of the Machining Department for Hagerstown Company agreed to the following monthly static budget for the upcoming year: The actual amount spent and the actual units produced in the first three months in the Machining Department were as follows: The Machining Department supervisor has been very pleased with this performance because actual expenditures for May-July have been significantly less than the monthly static budget of2,358,000. However, the plant manager believes that the budget should not remain fixed for every month but should flex or adjust to the volume of work that is produced in the Machining Department. Additional budget information for the Machining Department is as follows: a. Prepare a flexible budget for the actual units produced for May, June, and July in the MachiningDepartment. Assume depreciation is a fixed cost. b. Compare the flexible budget with the actual expenditures for the first three months.What does this comparison suggest?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT

EBK CONTEMPORARY FINANCIAL MANAGEMENTFinanceISBN:9781337514835Author:MOYERPublisher:CENGAGE LEARNING - CONSIGNMENT