Concept explainers

Videos

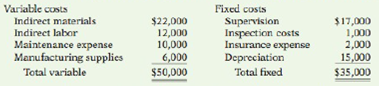

The manufacturing overhead budget for Fleming Company contains the following items.

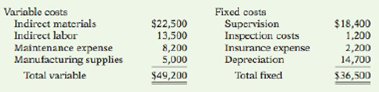

The budget was based on an estimated 2,000 units being produced. During the past month, 1,500 units were produced, and the following costs incurred.

Instructions

(a) Determine which items would be controllable by Fred Bedner, the production manager.

(b) How much should have been spent during the month for the manufacture of the 1,500 units?

(c) Prepare a flexible manufacturing overhead budget report for Mr. Bedner.

(d) Prepare a responsibility report. Include only the costs that would have been controllable by Mr. Bedner. Assume that the supervision cost above includes Mr Bedners salary of $10,000, both at budget and actual. In an attached memo, describe clearly for Mr. Bedner the areas in which his performance needs to be improved.

Want to see the full answer?

Check out a sample textbook solution

Chapter 10 Solutions

Managerial Accounting: Tools for Business Decision Making

Additional Business Textbook Solutions

Financial Accounting

Construction Accounting And Financial Management (4th Edition)

Principles of Accounting Volume 2

Horngren's Financial & Managerial Accounting, The Financial Chapters (6th Edition)

Managerial Accounting (4th Edition)

Intermediate Accounting (2nd Edition)

- Thomas Textiles Corporation began November with a budget for 60,000 hours of production in the Weaving Department. The department has a full capacity of 75,000 hours under normal business conditions. The budgeted overhead at the planned volumes at the beginning of November was as follows: The actual factory overhead was 725,000 for November. The actual fixed factory overhead was as budgeted. During November, the Weaving Department had standard hours at actual production volume of 64,500 hours. a. Determine the variable factory overhead controllable variance. b. Determine the fixed factory overhead volume variance.arrow_forwardSalisbury Bottle Company manufactures plastic two-liter bottles for the beverage industry. The cost standards per 100 two-liter bottles are as follows: At the beginning of March, Salisburys management planned to produce 500,000 bottles. The actual number of bottles produced for March was 525,000 bottles. The actual costs for March of the current year were as follows: a. Prepare the March manufacturing standard cost budget (direct labor, direct materials, and factory overhead) for Salisbury, assuming planned production. b. Prepare a budget performance report for manufacturing costs, showing the total cost variances for direct materials, direct labor, and factory overhead for March. c. Interpret the budget performance report.arrow_forwardUSD Inc. has established the following standard cost per unit: Although 10,000 units were budgeted, 12,000 units were produced. The Purchasing department bought 50,000 lb of materials at a cost of $237,500. Actual pounds of materials used were 46,000. Direct labor cost was $287,500 for 25,000 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forward

- Adam Corporation manufactures computer tables and has the following budgeted indirect manufacturing cost information for the next year: If Adam uses the step-down (sequential) method, beginning with the Maintenance Department, to allocate support department costs to production departments, the total overhead (rounded to the nearest dollar) for the Machining Department to allocate to its products would be: a. 407,500. b. 422,750. c. 442,053. d. 445,000.arrow_forwardFlexible budget for factory overhead Presented below are the monthly factory overhead cost budget (at normal capacity of 5,000 units or 20,000 direct labor hours) and the production and cost data for a month. The predetermined overhead rate is based on normal capacity. Required: 1. Assuming that variable costs will vary in direct proportion to the change in volume, prepare a flexible budget for production levels of 80%, 90%, and 110% of normal capacity. Also determine the predetermined factory overhead rate at each level of volume in both units and direct labor hours. 2. Prepare a flexible budget for production levels of 80%, 90%, and 110%, assuming that variable costs will vary in direct proportion to the change in volume, but with the following exceptions. (Hint: Set up a third category for semi-variable expenses.) a. At 110% of capacity, another supervisor will be needed at a salary of 24,000 annually. b. At 80% of capacity, the repairs expense will drop to one-half of the amount at 100% capacity. c. At 80% of capacity, one part-time maintenance worker, earning 10,000 a year, will be laid off. d. At 110% of capacity, a machine not normally in use and on which no depreciation is normally recorded will be used in production. Its cost was 12,000, it has a 10-year life, and straight-line depreciation will be taken.arrow_forwardAt the beginning of the period, the Fabricating Department budgeted direct labor of 72,000 and equipment depreciation of 18,500 for 2,400 hours of production. The department actually completed 2,350 hours of production. Determine the budget for the department, assuming that it uses flexible budgeting.arrow_forward

- Mesa Aquatics, Inc. estimated direct labor hours as 1,900 in quarter 1, 2,000 in quarter 2.2,200 in quarter 3, and 1,800 in quarter 4. a sales and administration budget using the information provided.arrow_forwardCarlo Lee Corp. has established the following standard cost per unit: Although 10,000 units were budgeted, only 8,800 units were produced. The purchasing department bought 55,000 lb of materials at a cost of $123,750. Actual pounds of materials used were 54,305. Direct labor cost was $186,550 for 18,200 hours worked. Required: Make journal entries to record the materials transactions, assuming that the materials price variance was recorded at the time of purchase. Make journal entries to record the labor variances.arrow_forwardDirect labor hours are estimated as 2,000 in Quarter 1; 2,100 in Quarter 2; 1,900 in Quarter 3; and 2,300 in Quarter 4. Prepare a manufacturing overhead budget using the information provided.arrow_forward

- Factory overhead cost variance report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 20,000 hours for production: Tannin has available 25,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 22,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Construct a factory overhead cost variance report for the Trim Department for July.arrow_forwardThe controller for Muir Companys Salem plant is analyzing overhead in order to determine appropriate drivers for use in flexible budgeting. She decided to concentrate on the past 12 months since that time period was one in which there was little important change in technology, product lines, and so on. Data on overhead costs, number of machine hours, number of setups, and number of purchase orders are in the following table. Required: 1. Calculate an overhead rate based on machine hours using the total overhead cost and total machine hours. (Round the overhead rate to the nearest cent and predicted overhead to the nearest dollar.) Use this rate to predict overhead for each of the 12 months. 2. Run a regression equation using only machine hours as the independent variable. Prepare a flexible budget for overhead for the 12 months using the results of this regression equation. (Round the intercept and x-coefficient to the nearest cent and predicted overhead to the nearest dollar.) Is this flexible budget better than the budget in Requirement 1? Why or why not?arrow_forwardListed below are the budgeted factory overhead costs for 2011 for Moss Industries at a projected level of 2,000 units: Required: Prepare flexible budgets for factory overhead at the 1,000, 2,000, and 4,000 unit levels. (Hint: You must first decide which of the listed costs should be considered variable and which should be fixed.)arrow_forward

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College