Concept explainers

Videos

Paul Golding and his wife, Nancy, established Crunchy Chips in 1938. Over the past 60 years, the company has established distribution channels in 11 western states, with production facilities in Utah, New Mexico, and Colorado. In 1980, Paul’s son, Edward, took control of the business. By 2017, it was clear that the company’s plants needed to gain better control over production costs to stay competitive. Edward hired a consultant to install a

The manufacturing process for potato chips begins when the potatoes are placed into a large vat in which they are automatically washed. After washing, the potatoes flow directly to an automatic peeler. The peeled potatoes then pass by inspectors, who manually cut out deep eyes or other blemishes. After inspection, the potatoes are automatically sliced and dropped into the cooking oil. The frying process is closely monitored by an employee. After the chips are cooked, they pass under a salting device and then pass by more inspectors, who sort out the unacceptable finished chips (those that are discolored or too small). The chips then continue on the conveyor belt to a bagging machine that bags them in 1-pound bags. After bagging, the bags are placed in a box and shipped. The box holds 15 bags.

The raw potato pieces (eyes and blemishes), peelings, and rejected finished chips are sold to animal feed producers for $0.16 per pound. The company uses this revenue to reduce the cost of potatoes. We would like this reflected in the price standard relating to potatoes.

Crunchy Chips purchases high-quality potatoes at a cost of $0.245 per pound. Each potato averages 4.25 ounces. Under efficient operating conditions, it takes four potatoes to produce one 16-ounce bag of plain chips. Although we label bags as containing 16 ounces, we actually place 16.3 ounces in each bag. We plan to continue this policy to ensure customer satisfaction. In addition to potatoes, other raw materials are the cooking oil, salt, bags, and boxes. Cooking oil costs $0.04 per ounce, and we use 3.3 ounces of oil per bag of chips. The cost of salt is so small that we add it to overhead. Bags cost $0.11 each and boxes $0.52 each.

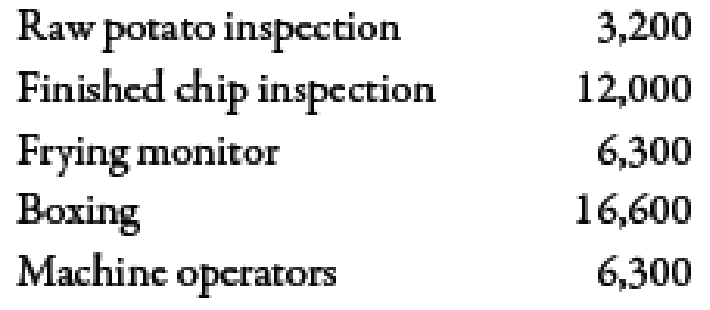

Our plant produces 8.8 million bags of chips per year. A recent engineering study revealed that we would need the following direct labor hours to produce this quantity if our plant operates at peak efficiency:

I’m not sure that we can achieve the level of efficiency advocated by the study. In my opinion, the plant is operating efficiently for the level of output indicated if the hours allowed are about 10% higher.

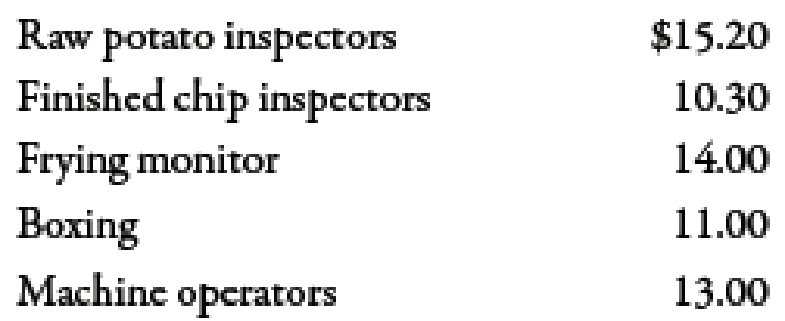

The hourly labor rates agreed upon with the union are:

Overhead is applied on the basis of direct labor dollars. We have found that variable overhead averages about 116% of our direct labor cost. Our fixed overhead is budgeted at $1,135,216 for the coming year.

Required:

- 1. Discuss the benefits of a standard costing system for Crunchy Chips.

- 2. Discuss the president’s concern about using the result of the engineering study to set the labor standards. What standard would you recommend?

- 3. Form a group with two or three other students. Develop a standard cost sheet for Crunchy Chips’ plain potato chips. Round all computations to four decimal places.

- 4. Suppose that the level of production was 8.8 million bags of potato chips for the year as planned. If 9.5 million pounds of potatoes were used, compute the materials usage variance for potatoes.

1.

Explain the benefits of a standard costing for Company CC.

Explanation of Solution

Variance:

The amount obtained when actual cost is deducted from budgeted cost is known as variance. Variance is calculated to find whether the cost is over applied or under applied.

The benefits of standard costing system for Company CC are explained below:

- Company CC is able to increase the control of its manufacturing inputs by using the standard costing.

- Company CC is able to evaluate the price and usage variances with the help of the price and quantity variances.

- Company CC is able to enhance its information by using the standard costing.

2.

Explain the concern of president about using the result of the engineering study to set the labor standards. Also, identify the best standard for the company.

Explanation of Solution

The concern of president is that whether the company is able to achieve its labor standards or not. If company is giving pressure on its workers for achieving the perfect standards, then it gives negative impact on the production of the workers. As a result, the outcome of the work of the workers is negative or unsatisfactory because workers get irritated and lower their performance. The best standard for the company is ideal standard because ideal standard is the most desired, highest quality or best standard that could easily achieve.

3.

Prepare a standard cost sheet for Company CC.

Explanation of Solution

Standard cost sheet for one box of chips:

| Particulars |

Quantity (Q) |

Price (P) ($) |

Amount ($) |

| Direct materials | |||

| Potatoes | 15.93751 | 0.238 | 3.7931 |

| Cooking oil | 49.5 | 0.04 | 1.9800 |

| Bags | 15 | 0.11 | 1.6500 |

| Boxes | 1 | 0.52 | 0.5200 |

| Total | 7.9431 |

Table (1)

Standard cost sheet of direct labor:

| Particulars |

Quantity (Q) |

Price (P) ($) |

Amount ($) |

| Direct labor | |||

| Potato inspection | 0.0062 | 15.20 | 0.0912 |

| Chip inspection | 0.02253 | 10.30 | 0.2318 |

| Frying monitor | 0.01184 | 14.00 | 0.1652 |

| Boxing | 0.03115 | 11.00 | 0.3421 |

| Machine operators | 0.01186 | 13.00 | 0.1534 |

| Variable overhead | 0.9837 | 1.16 | 1.1411 |

| Fixed overhead | 0.9837 | 1.96717 | 1.9350 |

| Direct material | 7.9431 | ||

| Total(A) | 12.0029 | ||

| Units of bags(B) | 15 | ||

|

Cost per bag | 0.8002 |

Table (2)

Working Note:

1.

Calculation of quantity of potatoes:

2.

Calcualtion of hours of potato inspection:

For calcualting the hours of potato inspection, first need to calculate the number of boxes per hour:

3.

Calcualtion of hours of Chips inspection:

4.

Calcualtion of hours of frying monitor:

5.

Calcualtion of hours of boxing:

6.

Calcualtion of hours of machine operators:

7.

Calculation of Fixed overhead rate:

4.

Calculate the material usage variances for potatoes.

Explanation of Solution

Use the following formula to calculate material usage variance of potato:

Substitute $9,500,000 for actual quantity, $9,350,000 for standard quantity and $0.238 for standard price in the above formula.

Therefore, the material usage variance is $37,500 (U).

Working Note:

1.

Calculation of standard quantity:

Want to see more full solutions like this?

Chapter 10 Solutions

Managerial Accounting

- Quincy Farms is a producer of items made from farm products that are distributed to supermarkets. For many years, Quincys products have had strong regional sales on the basis of brand recognition. However, other companies have been marketing similar products in the area, and price competition has become increasingly important. Doug Gilbert, the companys controller, is planning to implement a standard costing system for Quincy and has gathered considerable information from his coworkers on production and direct materials requirements for Quincys products. Doug believes that the use of standard costing will allow Quincy to improve cost control and make better operating decisions. Quincys most popular product is strawberry jam. The jam is produced in 10-gallon batches, and each batch requires six quarts of good strawberries. The fresh strawberries are sorted by hand before entering the production process. Because of imperfections in the strawberries and spoilage, one quart of strawberries is discarded for every four quarts of acceptable berries. Three minutes is the standard direct labor time required for sorting strawberries in order to obtain one quart of strawberries. The acceptable strawberries are then processed with the other ingredients: processing requires 12 minutes of direct labor time per batch. After processing, the jam is packaged in quart containers. Doug has gathered the following information from Joe Adams, Quincys cost accountant, relative to processing the strawberry jam. a. Quincy purchases strawberries at a cost of 0.80 per quart. All other ingredients cost a total of 0.45 per gallon. b. Direct labor is paid at the rate of 9.00 per hour. c. The total cost of direct material and direct labor required to package the jam is 0.38 per quart. Joe has a friend who owns a strawberry farm that has been losing money in recent years. Because of good crops, there has been an oversupply of strawberries, and prices have dropped to 0.50 per quart. Joe has arranged for Quincy to purchase strawberries from his friends farm in hopes that the 0.80 per quart will put his friends farm in the black. Required: 1. Discuss which coworkers Doug probably consulted to set standards. What factors should Doug consider in establishing the standards for direct materials and direct labor? 2. Develop the standard cost sheet for the prime costs of a 10-gallon batch of strawberry jam. 3. Citing the specific standards of the IMA Statement of Ethical Professional Practice described in Chapter 1, explain why Joes behavior regarding the cost information provided to Doug is unethical. (CMA adapted)arrow_forwardIngles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufactured table top and attaches the four purchased table legs. It takes 16 minutes of labor to assemble a table. The company follows a policy of producing enough tables to ensure that 40 percent of next months sales are in the finished goods inventory. Ingles also purchases sufficient materials to ensure that materials inventory is 60 percent of the following months scheduled production. Ingless sales budget in units for the next quarter is as follows: Ingless ending inventories in units for July 31 are as follows: Required: 1. Calculate the number of tables to be produced during August. 2. Disregarding your response to Requirement 1, assume the required production units for August and September are 2,100 and 1,900, respectively, and the July 31 materials inventory is 4,000 units. Compute the number of table legs to be purchased in August. 3. Assume that Ingles Corporation will produce 2,340 units in September. How many employees will be required for the Assembly Department in September? (Fractional employees are acceptable since employees can be hired on a part-time basis. Assume a 40-hour week and a 4-week month.) (CMA adapted)arrow_forwardPosavek is a wholesale supplier of building supplies building contractors, hardware stores, and home-improvement centers in the Boston metropolitan area. Over the years, Posavek has expanded its operations to serve customers across the nation and now employs over 200 people as technical representatives, buyers, warehouse workers, and sales and office staff. Most recently, Posavek has experienced fierce competition from the large online discount stores. In addition, the company is suffering from operational inefficiencies related to its archaic information system. Posavek revenue cycle procedures are described in the following paragraphs. Revenue Cycle Posaveks sales department representatives receive orders via traditional mail, e-mail, telephone, and the occasional walk-in customer. Because Posavek is a wholesaler, the vast majority of its business is conducted on a credit basis. The process begins in the sales department, where the sales clerk enters the customers order into the centralized computer sales order system. The computer and file server are housed in Posaveks small data processing department. If the customer has done business with Posavek in the past, his or her data are already on file. If the customer is a first-time buyer, however, the clerk creates a new record in the customer account file. The system then creates a record of the transaction in the open sales order file. When the order is entered, an electronic copy of it is sent to the customers e-mail address as confirmation. A clerk in the warehouse department periodically reviews the open sales order file from a terminal and prints two copies of a stock release document for each new sale, which he uses to pick the items sold from the shelves. The warehouse clerk sends one copy of the stock release to the sales department and the second copy, along with the goods, to the shipping department. The warehouse clerk then updates the inventory subsidiary file to reflect the items and quantities shipped. Upon receipt of the stock release document, the sales clerk accesses the open sales order file from a terminal, closes the sales order, and files the stock release document in the sales department. The sales order system automatically posts these transactions to the sales, inventory control, and cost-of-goods-sold accounts in the general ledger file. Upon receipt of the goods and the stock release, the shipping department clerk prepares the goods for shipment to the customer. The clerk prepares three copies of the bill of lading. Two of these go with the goods to the carrier and the third, along with the stock release document, is filed in the shipping department. The billing department clerk reviews the closed sales orders from a terminal and prepares two copies of the sales invoice. One copy is mailed to the customer, and the other is filed in the billing department. The clerk then creates a new record in the accounts receivable subsidiary file. The sales order system automatically updates the accounts receivable control account in the general ledger file. CASH RECEIPTS PROCEDURES Mail room clerks open customer cash receipts, reviews the check and remittance advices for completeness, and prepares two copies of a remittance list. One copy is sent with the checks to the cash receipts department. The second copy of the remittance advices are sent to the billing department. When the cash receipts clerk receives the checks and remittance list, he verifies the checks received against those on the remittance list and signs the checks For Deposit Only. Once the checks are endorsed, he records the receipts in the cash receipts journal from his terminal. The clerk then fills out a deposit slip and deposits the checks in the bank. Upon receipt of the remittances, the billing department clerk records the amounts in the accounts receivable subsidiary ledger from the department terminal. The system automatically updates the AR control account in the general ledger Posavek has hired your public accounting firm to review its sales order procedures for internal control compliance and to make recommendations for changes. Required a. Create a data flow diagram of the current system. b. Create a system flowchart of the existing system. c. Analyze the physical internal control weaknesses in the system. d. (Optional) Prepare a system flowchart of a redesigned computer-based system that resolves the control weaknesses that you identified. Explain your solution.arrow_forward

- Renslen, Inc., a truck manufacturing conglomerate, has recently purchased two divisions: Meyers Service Company and Wellington Products, Inc. Meyers provides maintenance service on large truck cabs for 10-wheeler trucks, and Wellington produces air brakes for the 10-wheeler trucks. The employees at Meyers take pride in their work, as Meyers is proclaimed to offer the best maintenance service in the trucking industry. The management of Meyers, as a group, has received additional compensation from a 10 percent bonus pool based on income before income taxes and bonus. Renslen plans to continue to compensate the Meyers management team on this basis as it is the same incentive plan used for all other Renslen divisions, except for the Wellington division. Wellington offers a high-quality product to the trucking industry and is the premium choice even when compared to foreign competition. The management team at Wellington strives for zero defects and minimal scrap costs; current scrap levels are at 2 percent. The incentive compensation plan for Wellington management has been a 1 percent bonus based on gross margin. Renslen plans to continue to compensate the Wellington management team on this basis. The following condensed income statements are for both divisions for the fiscal year ended May 31, 20x1: Renslen, Inc. Divisional Income Statements For the Year Ended May 31, 20x1 Each division has 1,000,000 of management salary expense that is eligible for the bonus pool. Renslen has invited the management teams of all its divisions to an off-site management workshop in July where the bonus checks will be presented. Renslen is concerned that the different bonus plans at the two divisions may cause some heated discussion. Required: 1. Determine the 20x1 bonus pool available for the management team at: a. Meyers Service Company b. Wellington Products, Inc. 2. Identify at least two advantages and disadvantages to Renslen, Inc., of the bonus pool incentive plan at: a. Meyers Service Company b. Wellington Products, Inc. 3. Having two different types of incentive plans for two operating divisions of the same corporation can create problems. a. Discuss the behavioral problems that could arise within management for Meyers Service Company and Wellington Products, Inc., by having different types of incentive plans. b. Present arguments that Renslen, Inc., can give to the management teams of both Meyers and Wellington to justify having two different incentive plans.arrow_forwardPaterson Company, a U.S.-based company, manufactures and sells electronic components worldwide. Virtually all its manufacturing takes place in the United States. The company has marketing divisions throughout Europe, including France. Debbie Kishimoto, manager of this division, was hired from a competitor 3 years ago. Debbie, recently informed of a price increase in one of the major product lines, requested a meeting with Jeff Phillips, marketing vice president. Their conversation follows. Debbie: Jeff, I simply dont understand why the price of our main product has increased from 5.00 to 5.50 per unit. We negotiated an agreement earlier in the year with our manufacturing division in Philadelphia for a price of 5.00 for the entire year. I called the manager of that division. He said that the original price was still acceptablethat the increase was a directive from headquarters. Thats why I wanted to meet with you. I need some explanations. When I was hired, I was told that pricing decisions were made by the divisions. This directive interferes with this decentralized philosophy and will lower my divisions profits. Given current market conditions, there is no way we can pass on the cost increase. Profits for my division will drop at least 600,000 if this price is maintained. I think a midyear increase of this magnitude is unfair to my division. Jeff: Under normal operating conditions, headquarters would not interfere with divisional decisions. But as a company, we are having some problems. What you just told me is exactly why the price of your product has been increased. We want the profits of all our European marketing divisions to drop. Debbie: What do you mean that you want the profits to drop? That doesnt make any sense. Arent we in business to make money? Jeff: Debbie, what you lack is corporate perspective. We are in business to make money, and thats why we want European profits to decrease. Our U.S. divisions are not doing well this year. Projections show significant losses. At the same time, projections for European operations show good profitability. By increasing the cost of key products transferred to Europeto your division, for examplewe increase revenues and profits in the United States. By decreasing your profits, we avoid paying taxes in France. With losses on other U.S. operations to offset the corresponding increase in domestic profits, we avoid paying taxes in the United States as well. The net effect is a much-needed increase in our cash flow. Besides, you know how hard it is in some of these European countries to transfer out capital. This is a clean way of doing it. Debbie: Im not so sure that its clean. I cant imagine the tax laws permitting this type of scheme. There is another problem, too. You know that the companys bonus plans are tied to a divisions profits. This plan could cost all of the European managers a lot of money. Jeff: Debbie, you have no reason to worry about the effect on your bonusor on our evaluation of your performance. Corporate management has already taken steps to ensure no loss of compensation. The plan is to compute what income would have been if the old price had prevailed and base bonuses on that figure. Ill meet with the other divisional managers and explain the situation to them as well. Debbie: The bonus adjustment seems fair, although I wonder if the reasons for the drop in profits will be remembered in a couple of years when Im being considered for promotion. Anyway, I still have some strong ethical concerns about this. How does this scheme relate to the tax laws? Jeff: We will be in technical compliance with the tax laws. In the United States, Section 482 of the Internal Revenue Code governs this type of transaction. The key to this law, as well as most European laws, is evidence of an arms-length price. Since youre a distributor, we can use the resale price method to determine such a price. Essentially, the arms-length price for the transferred good is backed into by starting with the price at which you sell the product and then adjusting that price for the markup and other legitimate differences, such as tariffs and transportation. Debbie: If I were a French tax auditor, I would wonder why the markup dropped from last year to this year. Are we being good citizens and meeting the fiscal responsibilities imposed on us by each country in which we operate? Jeff: Well, a French tax auditor might wonder about the drop in markup. But, the markup is still within reason, and we can make a good argument for increased costs. In fact, weve already instructed the managers of our manufacturing divisions to legitimately reassign as many costs as they can to the European product lines. So far, they have been very successful. I think our records will support the increase that you are receiving. You really do not need to be concerned with the tax authorities. Our tax department assures me that this has been carefully researchedits unlikely that a tax audit will create any difficulties. Itll all be legal and above board. Weve done this several times in the past with total success. Required: 1. Do you think that the tax-minimization scheme described to Debbie Kishimoto is in harmony with the ethical behavior that should be displayed by top corporate executives? Why or why not? What would you do if you were Debbie? 2. Apparently, the tax department of Paterson Company has been strongly involved in developing the tax-minimization scheme. Assume that the accountants responsible for the decision are CMAs and members of the IMA, subject to the IMA standards of ethical conduct. Review the IMA standards for ethical conduct in Chapter 1. Are any of these standards being violated by the accountants in Patersons tax department? If so, identify them. What should these tax accountants do if requested to develop a questionable taxminimization scheme?arrow_forwardLeather Works is a family-owned maker of leather travel bags and briefcases located in the northeastern part of the United States. Foreign competition has forced its owner, Heather Gray, to explore new ways to meet the competition. One of her cousins, Wallace Hayes, who recently graduated from college with a major in accounting, told her about the use of cost variance analysis to learn about efficiencies of production. In May of last year, Heather asked Matt Jones, chief accountant, and Alfred Prudest, production manager, to implement a standard costing system. Matt and Alfred, in turn, retained Shannon Leikam, an accounting professor at Hardings College, to set up a standard costing system by using information supplied to her by Matts and Alfreds staff. To verify that the information was accurate, Shannon visited the plant and measured workers output using time and motion studies. During those visits, she was not accompanied by either Matt or Alfred, and the workers knew about Shannons schedule in advance. The cost system was implemented in June of last year. Recently, the following dialogue took place among Heather, Matt, and Alfred: HEATHER: How is the business performing? ALFRED: You know, we are producing a lot more than we used to, thanks to the contract that you helped obtain from Lean, Inc., for laptop covers. (Lean is a national supplier of computer accessories.) MATT: Thank goodness for that new product. It has kept us from sinking even more due to the inroads into our business made by those foreign suppliers of leather goods. HEATHER: What about the standard costing system? MATT: The variances are mostly favorable, except for the first few months when the supplier of leather started charging more. HEATHER: How did the union members take to the standards? ALFRED: Not bad. They grumbled a bit at first, but they have taken it in stride. Weve consistently shown favorable direct labor efficiency variances and direct materials usage variances. The direct labor rate variance has been flat. MATT: It should be since direct labor rates are negotiated by the union representative at the start of the year and remain the same for the entire year. HEATHER: Matt, would you send me the variance report for laptop covers immediately? The following chart summarizes the direct materials and direct labor variances from November of last year through April of this year (extracted from the report provided by Matt). Standards for each laptop cover are as follows: a. Three feet of direct materials at 7.50 per foot b. Forty-five minutes of direct labor at 14 per hour In addition, the data for May of this year, but not the variances for the month, are as follows: Actual direct labor cost per hour exceeded the budgeted rate by 0.10 per hour. Required: 1. For May of this year, calculate the price and quantity variances for direct labor and direct materials. 2. Discuss the trend of the direct materials and labor variances. 3. What type of actions must the workers have taken during the period they were being observed for the setting of standards? 4. What can be done to ensure that the standards are set correctly? (CMA adapted)arrow_forward

- As CEO of Riverside Marine, Rachel Moore knows it is important to control costs and to respond quickly to changes in the highly competitive boat-building industry. When Gerbig Consulting proposes that Riverside Marine invest in an ERP system, she forms a team to evaluate the proposal: the plant engineer, the plant foreman, the systems specialist, the human resources director, the marketing director, and the management accountant. A month later, the management accountant Miles Cobalt reports that the team and Gerbig estimate that if Riverside Marine implements the ERP system, it will incur the following costs: Costs of the Project a.$390,000 in software costs b. $85,000 to customize the ERP software and load Riverside Marine'sdata into the new ERP system c. $112,000 for employee training Benefits of the Project a. More efficient order processing should lead to savings of $185,000. b. Streamlining the manufacturing process so that it maps into the ERP…arrow_forwardMirabel Manufacturing is a small but growing company that manufactures and sells marine sonar equipment. They employ a national sales force and their primary customers are marine retailers and boat dealerships. The company has expanded over the last 5 years and Paul Mirabel, the founder, and CEO has become concerned that he no longer has a clear picture of their cost structure. He calls his CFO, Mary Jane Montgomery in for a meeting. “Mary Jane, I am concerned that I am not current on our cost structure and how that is impacting our bottom line,” Paul begins. “Well, Paul, the company has grown considerably over the past 5 years, so I’m not surprised that you feel a little disconnected with how things are going,” Mary Jane replied. She continued “In fact, I’ve been meaning to talk to you about a couple of big items such as increasing the sales commission to 15%. We’ve lost two of our best account managers in the last 9 months. It seems like we are behind the curve paying only 12% on…arrow_forwardMark Benny started MM LTD, a niche furniture brand, 10 years ago. he ran the business as a sole proprietorship. While he has 50 skilled carpenters and 5 sales people on his payroll, he has been taking care of the accounting by himself. Now, he intends to offer 40% of the ownership to public in next couple years and is willing to make changes and has hired George as a management accountant to organize and improve the accounting systems. MM LTD's total budgeted manufacturing overheads cost for the current year is Ugx 111,240,000 and budgeted total labor hours are 20,000. Jemba Fred the financial accountant has been applying traditional costing method during the whole 10 years period. MM LTD's sofas includes the 2-set, 3-set and 6-set options. State House recently placed an order for 150 units of the 6-set type. The order is expected to be delivered in one-month time. Since it is a customized order, State House will be billed at cost plus 25%. George is not a fan of traditional costing…arrow_forward

- Ingles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufactured table top and attaches the four purchased table legs. It takes 16 minutes of labor to assemble a table. The company follows a policy of producing enough tables to ensure that 40 percent of next month’s sales are in the finished goods inventory. Ingles also purchases sufficient materials to ensure that materials inventory is 60 percent of the following month’s scheduled production. Ingles’s sales budget inunits for the next quarter is as follows: July 2,450August 2,900September 2,100Ingles’s ending inventories in units for July 31 are as follows:Finished goods 1,900Materials (legs) 4,000 Required:1. Calculate the number of tables to be produced during August. 2. Disregarding your response to Requirement 1, assume the required…arrow_forwardSteven oversees the production department for a factory that makes plastic outdoor chairs. department sells all of its production to external parties, and the department has an overall production capacity of 150,000 chairs. Their sales data is as follows: Sales (90,000 chairs) a $460,000, Variable Costs are $206,200, and Fixed Costs are $194,350. The internal Resale would like to purchase 26,700 chairs from the Production Department. They will be selling external retailers for $15.49 per chair. If the Resale Division negotiates a deal with the Pro Department to purchase each chair for its absorption cost plus a 2.4% markup, then what amount of Operating Income the Resale Division would report for their sale of 26,700 cha per unit cost to nearest cents. O $291,831 O $351,105 O $198,235 O $3,612arrow_forwardBlue Skies Inc. is a retail gardening company that is piloting a new strategic initiative aimed at increasing gross profit. Currently, the company’s gross profit is 25% of sales, and its target gross profit percentage is 30%. The company’s current monthly sales revenue is $600,000.The new initiative being piloted is to produce goods in-house instead of buying them from wholesale suppliers. Its in-house production process has two procedures. The makeup of the costsof production for Procedure 1 is 40% direct labor, 45% direct materials, and 15% overhead. The makeup of the costs of production for Procedure 2 is 60% direct labor, 30% direct materials, and 10% overhead. Assume that Procedure 1 costs twice as much as Procedure 2.Instructions1. Determine what the cost of labor, materials, and overhead for both Procedures 1 and 2 wouldneed to be for the company to meet its target gross profit.2. The company’s actual labor cost is $114,000 for Procedure 1. Determine the actual cost of…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,