PRINCIPLES OF TAXATION F/BUS...(LL)

23rd Edition

ISBN: 9781260433197

Author: Jones

Publisher: MCG

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 11, Problem 4AP

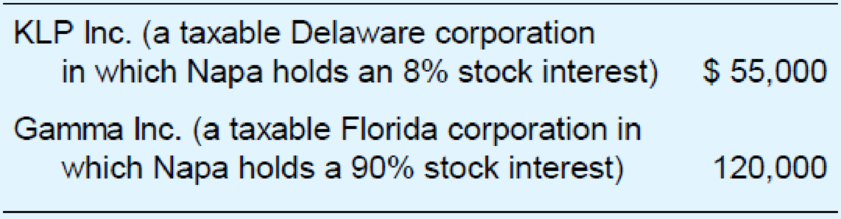

This year, Napa Corporation received the following dividends.

Napa and Gamma do not file a consolidated tax return. Compute Napa’s dividends-received deduction.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

In its first year of existence (year 1), Willow Corp. (a C corporation) reports a loss for tax purposes of $50,000. In year 2 it reports a $40,000 loss. For year 3, it reports taxable income from operations of $100,000 before any loss carryovers. How much tax will Willow Corp. pay in year 3, what is its NOL carryover to year 4, and when will the NOL expire under the following assumptions? (New Corporate income tax rate has been mentioned as "21% on all taxable income" as per the recent change. Leave no answer blank. Enter zero if applicable.)

a. Year 1 is 2017.

Willow Corp. tax liability in Year 3

Willow Corp. NOL carryover to Year 4

An S corporation’s only transaction for the year was the receipt of $10,000 in tax-exempt interest. How would a $6,000 distribution be taxed to the sole shareholder if the S corporation has an accumulated adjustments account of a negative $6,500 at the beginning of the year?

Which

of the following dividends received by lon Corp. would NOT be subject to Part IV tax?

O A. Dividends received from a wholly owned subsidiary of lon Corp. and, as a result of distributing this dividend, the wholly owned subsidiary received a

dividend refund of $5,000.

O B. Dividends received from lon Corp.'s portfolio of investments that are deductible in the calculation of taxable income for lon Corp.

O C. Dividends received from an unconnected company that is deductible in the calculation of taxable income for lon Corp.

O D. Dividends received from a wholly owned subsidiary of lon Corp. and the wholly owned subsidiary did not receive a dividend refund in the current year.

Chapter 11 Solutions

PRINCIPLES OF TAXATION F/BUS...(LL)

Ch. 11 - Prob. 1QPDCh. 11 - Prob. 2QPDCh. 11 - Prob. 3QPDCh. 11 - Prob. 4QPDCh. 11 - Prob. 5QPDCh. 11 - Libretto Corporation owns a national chain of...Ch. 11 - Prob. 7QPDCh. 11 - Prob. 8QPDCh. 11 - Prob. 9QPDCh. 11 - In your own words, explain the conclusion that...

Ch. 11 - Prob. 1APCh. 11 - Prob. 2APCh. 11 - Corporation P owns 93 percent of the outstanding...Ch. 11 - This year, Napa Corporation received the following...Ch. 11 - This year, GHJ Inc. received the following...Ch. 11 - In its first year, Camco Inc. generated a 92,000...Ch. 11 - Prob. 7APCh. 11 - Prob. 8APCh. 11 - Cranberry Corporation has 3,240,000 of current...Ch. 11 - Hallick Inc. has a fiscal year ending June 30....Ch. 11 - Landover Corporation is looking for a larger...Ch. 11 - Cramer Corporation, a calendar year, accrual basis...Ch. 11 - Prob. 13APCh. 11 - Prob. 14APCh. 11 - Prob. 15APCh. 11 - Prob. 16APCh. 11 - In each of the following cases, compute the...Ch. 11 - Prob. 18APCh. 11 - Prob. 19APCh. 11 - Jackson Corporation has accumulated minimum tax...Ch. 11 - Camden Corporation, a calendar year accrual basis...Ch. 11 - Callen Inc. has accumulated minimum tax credits of...Ch. 11 - Prob. 23APCh. 11 - Prob. 24APCh. 11 - In 2018, NB Inc.s federal taxable income was...Ch. 11 - James, who is in the 35 percent marginal tax...Ch. 11 - Leona, whose marginal tax rate on ordinary income...Ch. 11 - Prob. 28APCh. 11 - Prob. 29APCh. 11 - Prob. 30APCh. 11 - Prob. 1IRPCh. 11 - Prob. 2IRPCh. 11 - Prob. 3IRPCh. 11 - Prob. 4IRPCh. 11 - Prob. 5IRPCh. 11 - Prob. 6IRPCh. 11 - Prob. 7IRPCh. 11 - Prob. 8IRPCh. 11 - Prob. 1RPCh. 11 - Prob. 2RPCh. 11 - Prob. 3RPCh. 11 - This year, Prewer Inc. received a 160,000 dividend...Ch. 11 - Prob. 1TPCCh. 11 - Prob. 2TPC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Which of the following statements is false? A. A corporation must file a Federal income tax return even if it has no taxable income for the year. B. Dividend received deduction is calculated as the dividend received times deduction percentage. C. A corporation cannot deduct net capital losses against its operating income. D. A C corporation with taxable income of $100,000 in the current year will have a tax liability of $21,000. E. Schedule M-1 is used to reconcile net income as computed for financial accounting purposes with taxable income reported on the corporation's income tax return.arrow_forwardMultiple Choice $200,933 $174,983 $208,433 $172,509arrow_forwardAnn Corporation reported pretax book income of $1,800,000. Included in the computation were favorable temporary differences of $182,500, unfavorable temporary differences of $267,000, and favorable permanent differences of $112,000. Compute the company’s book equivalent of taxable income. Use this number to compute the company’s total income tax provision or benefit. Determine the book equavalent of taxable income and total income tax proivison or benefit.arrow_forward

- Relix, Inc., is a domestic corporation. Relix, Inc., reported two permanent differences between book and taxable income. It earned $2,375 in tax-exempt municipal bond interest, and it incurred $780 in nondeductible business meals expense. Relix's book income before tax is $4,800. Assume a 21% Federal corporate tax rate. Provide the information for the income tax footnote rate reconciliation for Relix. For dollar amounts, round to the nearest dollar and use rounded amounts in subsequent computations. For the percentage answers, round to four decimal places before converting to a percentage. For example, round .56329 to .5633 and enter as 56.33%. Dollars Percentage Tax on book income at U.S. statutory rate % Tax-exempt income % Nondeductible business meals % Provision for income tax expense %arrow_forwardRiverbend Inc. received a $267,500 dividend from stock it held in Hobble Corporation. Riverbend's taxable income is $2,440,000 before deducting the dividends received deduction (DRD), a $45,000 NOL carryover, and a $137,000 charitable contribution Assuming the facts in part (c), what is Riverbend’s marginal tax rate on the dividend?arrow_forwardOn its year 1 financial statements, Seatax Corporation, an accrual-method taxpayer, reported federal income tax expense of $570,000. On its year 1 tax return, it reported a tax liability of $650,000. During year 1, Seatax made estimated tax payments of $700,000. What book-tax difference, if any, associated with its federal income tax expense should Seatax have reported when computing its year 1 taxable income? Is the difference favorable or unfavorable? Is it temporary or permanent? Year 1 Book-tax Difference Favorable or Unfavorable Temporary or Permanentarrow_forward

- [The following information applies to the questions displayed below] What book-tax differences in year 1 and year 2 associated with its capital gains and losses would ABD Incorporated report in the following alternative scenarios? Identify each book-tax difference as favorable or unfavorable and as permanent or temporary. Note: Leave no answer blank. Enter zero if applicable and select "Not applicable" if no effect. f. Answer for year 7 only. Capital gains Capital losses Year 1 $ 0 10,000 Years 2 Year 7 $ 0 0 $ 15,000 0 Book-tax Difference Favorable or Unfavorable Year 7 Temporary or Permanentarrow_forwardDuring the year, CDE Corporation earned enough profits to pay dividends to its shareholders. CDE is a C corporation. What are the tax consequences of this distribution? (a) The corporation will increase their earnings and profits by the amount distributed. (b) The corporation will reduce its taxable income by the amount distributed to the shareholders. (c) The corporation will pay a flat tax of 21% on the amount distributed. The shareholders also include their dividends received in taxable income. (d) There are no direct tax consequences for either the corporation or the shareholders.arrow_forward1)During the year, CDE Corporation earned enough profits to pay dividends to its shareholders. CDE is a C corporation. What are the tax consequences of this distribution? The corporation will increase their earnings and profits by the amount distributed. The corporation will reduce its taxable income by the amount distributed to the shareholders. The corporation will pay a flat tax of 21% on the amount distributed. The shareholders also include their dividends received in taxable income. There are no direct tax consequences for either the corporation or the shareholders. 20 Choose the response that correctly describes a guaranteed payment. A loan payment from the partnership to pay back a loan from a partner. A loan payment from the partner to pay back a loan from a partnership. A payment made to a partner from the profits of the partnership. A payment made to a partner without regard to the income of the partnership. 3)Which of the following expenses may a partnership…arrow_forward

- The Parent consolidated group reports the following results for the 2021 tax year. Entity Income or Loss Parent $13,600 Sub1 (1,360) Sub2 5,440 Sub3 2,720 Do not round any division in your computations. If required, round your answers to nearest whole dollar. If an amount is zero, enter "0". a. What is the group's consolidated taxable income and consolidated tax liability? If the relative taxable income method, the consolidated taxable income is $fill in the blank 1 and the total consolidated tax liability is $fill in the blank 2 . b. If the Parent group has consented to the relative taxable income method, how will the consolidated tax liability be allocated among the Parent and Subsidiaries 1, 2, and 3? Entity Income or Loss Parent $fill in the blank 3 Sub1 $fill in the blank 4 Sub2 $fill in the blank 5 Sub3 $fill in the blank 6arrow_forwardThe following information is taken from the current year financial statements of Esper Corpo tion. (Dollar figures and shares of stock are in thousands.) The first three items are net of an cable income tax. The loss from continuing operations does not include the loss from lawsuit.arrow_forwardThe Parent consolidated group reports the following results for the 2021 tax year. Entity Parent Income or Loss $78,600 Sub1 (7,860) Sub2 Sub3 31,440 15,720 Do not round any division in your computations. If required, round your answers to nearest whole dollar. If an amount is zero, enter "0". a. What is the group's consolidated taxable income and consolidated tax liability? If the relative taxable income method, the consolidated taxable income is $ the total consolidated tax liability is $ b. If the Parent group has consented to the relative taxable income method, how will the consolidated tax liability be allocated among the Parent and Subsidiaries 1, 2, and 3? Entity Income or Loss Parent $ Sub1 $ Sub2 $ Sub3 $ HA andarrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Operating Loss Carryback and Carryforward; Author: SuperfastCPA;https://www.youtube.com/watch?v=XiYhgzSGDAk;License: Standard Youtube License