Videos

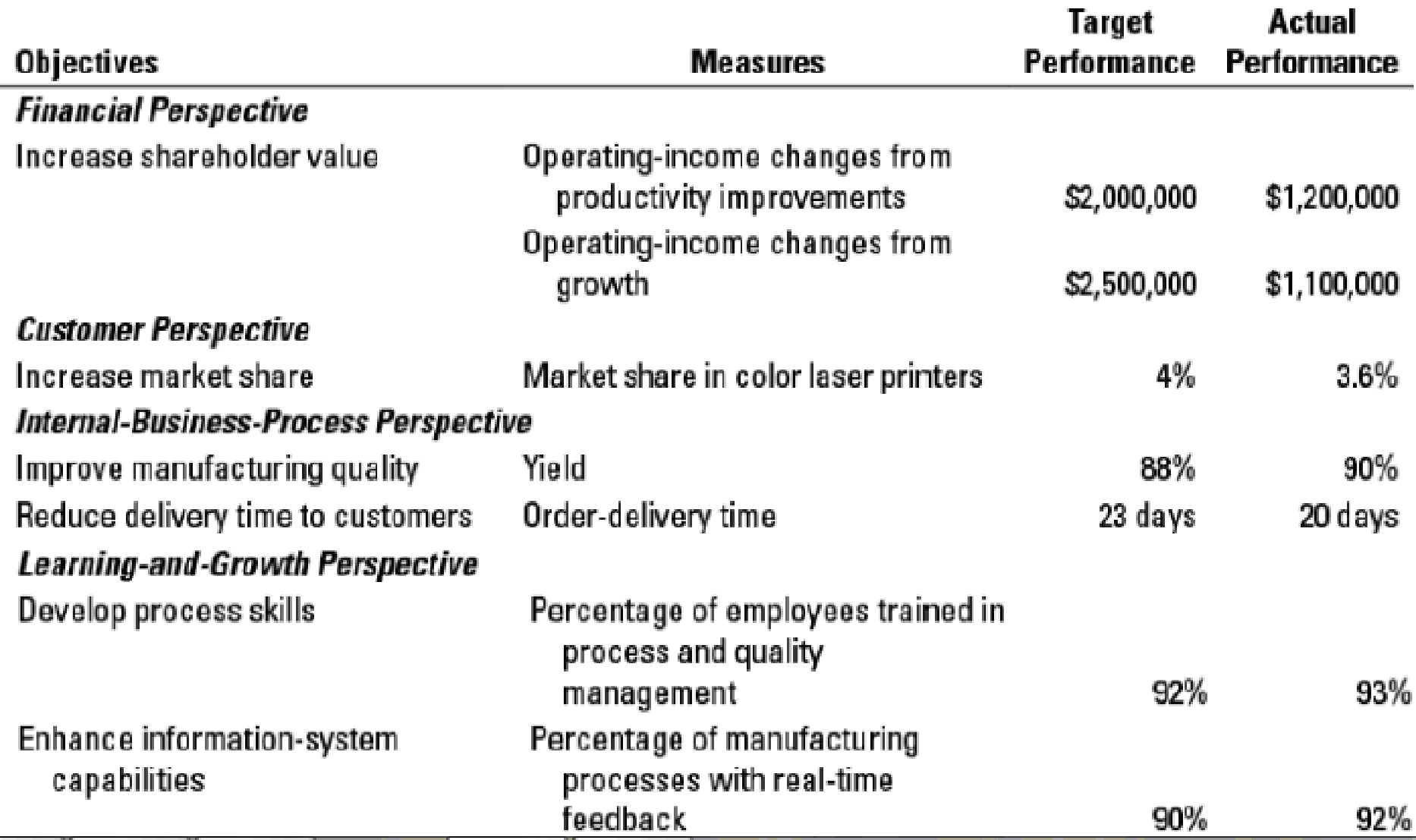

Balanced scorecard. Vic Corporation manufactures various types of color laser printers in a highly automated facility with high fixed costs. The market for laser printers is competitive. The various color laser printers on the market are comparable in terms of features and price. Vic believes that satisfying customers with products of high quality at low costs is important to achieving its target profitability. For 2017, Vic plans to achieve higher quality and lower costs by improving yields and reducing defects in its manufacturing operations. Vic will train workers and encourage and empower them to take the necessary actions. Currently, a significant amount of Vic’s capacity is used to produce products that are defective and cannot be sold. Vic expects that higher yields will reduce the capacity that Vic needs to manufacture products. Vic does not anticipate that improving manufacturing will automatically lead to lower costs because many costs are fixed costs. To reduce fixed costs per unit, Vic could lay off employees and sell equipment, or it could use the capacity to produce and sell more of its current products or improved models of its current products.

Vic’s balanced scorecard (initiatives omitted) for the just-completed fiscal year 2017 follows.

- 1. Was Vic successful in implementing its strategy in 2017? Explain.

Required

- 2. Is Vic’s balanced scorecard useful in helping the company understand why it did not reach its target market share in 2017? If it is, explain why. If it is not, explain what other measures you might want to add under the customer perspective and why.

- 3. Would you have included some measure of employee satisfaction in the learning-and-growth perspective and new-product development in the internal-business-process perspective? That is, do you think employee satisfaction and development of new products are critical for Vic to implement its strategy? Why or why not? Explain briefly.

- 4. What problems, if any, do you see in Vic improving quality and significantly downsizing to eliminate unused capacity?

Trending nowThis is a popular solution!

Chapter 12 Solutions

HORNGRENS COST ACCOUNTING W/ACCESS

- Balanced scorecard. Pineway Electric manufactures electric motors. It competes and plans to grow by selling high-quality motors at a low price and by delivering them to customers in a reasonable time after receiving customers’ orders. There are many other manufacturers who produce similar motors. Pineway believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy in 2017.arrow_forwardBalanced scorecard. Pineway Electric manufactures electric motors. It competes and plans to grow by selling high-quality motors at a low price and by delivering them to customers in a reasonable time after receiving customers’ orders. There are many other manufacturers who produce similar motors. Pineway believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy in 2017. Q.Ramsey Corporation, a competitor of Pineway, manufactures electric motors with more sizes and features than Pineway at a higher price. Ramsey’s motors are of high quality but require more time to produce and so have longer delivery times. Draw a simple customer preference map as in Exhibit 12-1 for Pineway and Ramsey using the attributes of price, delivery time, quality, and design features.arrow_forwardBalanced scorecard. Pineway Electric manufactures electric motors. It competes and plans to grow by selling high-quality motors at a low price and by delivering them to customers in a reasonable time after receiving customers’ orders. There are many other manufacturers who produce similar motors. Pineway believes that continuously improving its manufacturing processes and having satised employees are critical to implementing its strategy in 2017.arrow_forward

- Balanced scorecard. Pineway Electric manufactures electric motors. It competes and plans to grow by selling high-quality motors at a low price and by delivering them to customers in a reasonable time after receiving customers’ orders. There are many other manufacturers who produce similar motors. Pineway believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy in 2017. Q.Is Pineway’s 2017 strategy one of product differentiation or cost leadership? Explain briefly.arrow_forwardBalanced scorecard. Pineway Electric manufactures electric motors. It competes and plans to grow by selling high-quality motors at a low price and by delivering them to customers in a reasonable time after receiving customers’ orders. There are many other manufacturers who produce similar motors. Pineway believes that continuously improving its manufacturing processes and having satisfied employees are critical to implementing its strategy in 2017. Q. Draw a strategy map as in Exhibit 12-2 with at least two strategic objectives you would expect to see under each balanced scorecard perspective. Identify what you believe are any (a) strong ties, (b) focal points, (c) trigger points, and (d) distinctive objectives. Comment on the structural analysis of your strategy map.arrow_forwardBalanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to nancial success is to offer a quality service at the lowest cost. Comtex currently spends a signicant amount of hours on installation and postinstallation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows.arrow_forward

- Balanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to financial success is to offer a quality service at the lowest cost. Comtex currently spends a significant amount of hours on installation and post-installation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows in the attatched: Q. Why do you think Comtex included balanced scorecard measures relating to employee safety and community engagement? How well is the company doing on these measures?arrow_forwardBalanced scorecard, social performance. Comtex Company provides cable and Internet services in the greater Boston area. There are many competitors that provide similar services. Comtex believes that the key to financial success is to offer a quality service at the lowest cost. Comtex currently spends a significant amount of hours on installation and post-installation support. This is one area that the company has targeted for cost reduction. Comtex’s balanced scorecard for 2017 follows.arrow_forwardStrategy, balanced scorecard, service company. Compton Associates is an architectural rm that has been in practice only a few years. Because it is a relatively new rm, the market for the rm’s services is very competitive. To compete successfully, Compton must deliver quality services at a low cost. Compton presents the following data for 2016 and 2017.arrow_forward

- Coral Creations has strategic plans that call for rapid growth, a limited number of units for each design to enhance exclusivity, designs for the perfect fit, on-time delivery to customers, retention of highly trained employees with innovative skills, and excellent inventory control. A. Suggest one performance measure for each dimension of the balanced scorecard for Coral Creations. B. Take one of your measures and discuss the linkage it has to multiple strategies in Corals plan.arrow_forwardJolene Askew, manager of Feagan Company, has committed her company to a strategically sound cost reduction program. Emphasizing life-cycle cost management is a major part of this effort. Jolene is convinced that production costs can be reduced by paying more attention to the relationships between design and manufacturing. Design engineers need to know what causes manufacturing costs. She instructed her controller to develop a manufacturing cost formula for a newly proposed product. Marketing had already projected sales of 25,000 units for the new product. (The life cycle was estimated to be 18 months. The company expected to have 50 percent of the market and priced its product to achieve this goal.) The projected selling price was 20 per unit. The following cost formula was developed: Y=200,000+10X1 where X1=Machinehours(Theproductisexpectedtouseonemachinehourforeveryunitproduced.) Upon seeing the cost formula, Jolene quickly calculated the projected gross profit to be 50,000. This produced a gross profit of 2 per unit, well below the targeted gross profit of 4 per unit. Jolene then sent a memo to the Engineering Department, instructing them to search for a new design that would lower the costs of production by at least 50,000 so that the target profit could be met. Within two days, the Engineering Department proposed a new design that would reduce unit-variable cost from 10 per machine hour to 8 per machine hour (Design Z). The chief engineer, upon reviewing the design, questioned the validity of the controllers cost formula. He suggested a more careful assessment of the proposed designs effect on activities other than machining. Based on this suggestion, the following revised cost formula was developed. This cost formula reflected the cost relationships of the most recent design (Design Z). Y=140,000+8X1+5,000X2+2,000X3 where X1=MachinehoursX2=NumberofbatchesX3=Numberofengineeringchangeorders Based on scheduling and inventory considerations, the product would be produced in batches of 1,000; thus, 25 batches would be needed over the products life cycle. Furthermore, based on past experience, the product would likely generate about 20 engineering change orders. This new insight into the linkage of the product with its underlying activities led to a different design (Design W). This second design also lowered the unit-level cost by 2 per unit but decreased the number of design support requirements from 20 orders to 10 orders. Attention was also given to the setup activity, and the design engineer assigned to the product created a design that reduced setup time and lowered variable setup costs from 5,000 to 3,000 per setup. Furthermore, Design W also creates excess activity capacity for the setup activity, and resource spending for setup activity capacity can be decreased by 40,000, reducing the fixed cost component in the equation by this amount. Design W was recommended and accepted. As prototypes of the design were tested, an additional benefit emerged. Based on test results, the post-purchase costs dropped from an estimated 0.70 per unit sold to 0.40 per unit sold. Using this information, the Marketing Department revised the projected market share upward from 50 percent to 60 percent (with no price decrease). Required: 1. Calculate the expected gross profit per unit for Design Z using the controllers original cost formula. According to this outcome, does Design Z reach the targeted unit profit? Repeat, using the engineers revised cost formula. Explain why Design Z failed to meet the targeted profit. What does this say about the use of unit-based costing for life-cycle cost management? 2. Calculate the expected profit per unit using Design W. Comment on the value of activity information for life-cycle cost management. 3. The benefit of the post-purchase cost reduction of Design W was discovered in testing. What direct benefit did it create for Feagan Company (in dollars)? Reducing post-purchase costs was not a specific design objective. Should it have been? Are there any other design objectives that should have been considered?arrow_forwardLuxe Inc., a chain of gasoline service stations, has a strategy of charging premium prices for its gasoline by providing excellent service such as attendants to pump gas, clean restrooms, and free air for tire inflation. Its balanced scorecard performance measures include: Increase in operating income through cost reduction (Financial); market share in the overall gasoline market (Customer); wait-time at the pump (Internal Business Processes); and employee bonus based on number of customers served (Learning and Growth). Indicate whether each of these performance measures is appropriate, given Luxes strategy.arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning