Managerial Economics & Business Strategy (Mcgraw-hill Series Economics)

9th Edition

ISBN: 9781259290619

Author: Michael Baye, Jeff Prince

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 12, Problem 3CACQ

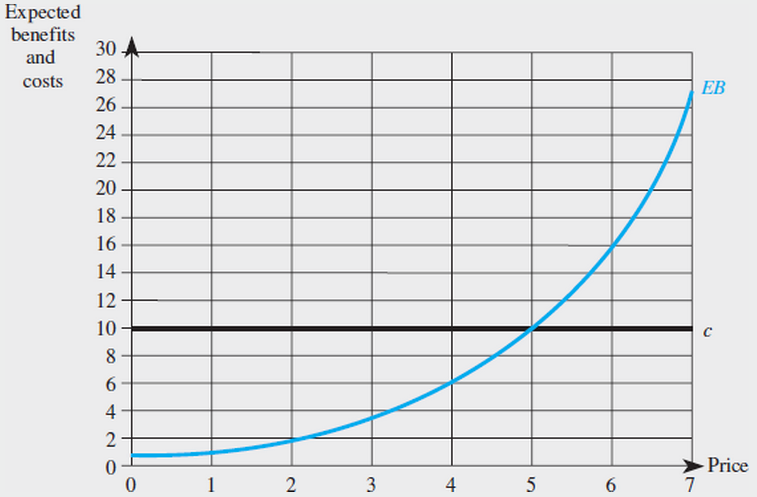

Your store sells an item desired by a consumer. The consumer is using an optimal search strategy; the accompanying graph shows the consumer’s expected benefits and costs of searching for a lower

- What is the consumer’s reservation price?

- If your price is $3 and the consumer visits your store, will she purchase the item or continue to search? Explain.

- Suppose the consumer’s cost of each search rises to $16. What is the highest price you can charge and still sell the item to the consumer if she visits your store?

- Suppose the consumer’s cost of each search falls to $2. If the consumer finds a store charging $3, will she purchase at that price or continue to search?

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

give me correct answer with proper explanation

A network effect, or network externality, exists when: Group of answer choices a firm

’

s average total cost rises continuously over the entire ran the customers of one business overlap with those of another competing business. the costs of resources for an industry rises as the number of sellers in an industry expands. the value of a product or service to each consumer increases as the number of users expands.

Harriet McNeil, proprietor of McNeil's Auto Mall, believes that it is good business for her automobile dealership to have more customers on the lot than can be served, as she believes this creates an impression that demand for the automobiles on her lot is high. However, she also understands that if there are far more customers on the lot than can be served by her salespeople, her dealership may lose sales to customers who become frustrated and leave without making a purchase.

Ms. McNeil is primarily concerned about the staffing of salespeople on her lot on Saturday mornings (8:00 a.m. to noon), which are the busiest time of the week for McNeil's Auto Mall. On Saturday mornings, an average of 6.8 customers arrive per hour. The customers arrive randomly at a constant rate throughout the morning, and a salesperson spends an average of one hour with a customer. Ms. McNeil's experience has led her to conclude that if there are two more customers on her lot than can be served at any time…

TRUE OR FALSE?

An increase in price tends to make consumer buy less and sellers to sell more. A price decrease tends to cause the opposite reaction.

An increase in income will shift the demand curve to the left on the graph. A decrease in income will shift the demand curve to the right.

Shifts in either the demand curve alone or the supply curve alone cannot cause a change in the equilibrium point. It is only when both the demand curve and supply curve shift that the equilibrium point is changed.

Chapter 12 Solutions

Managerial Economics & Business Strategy (Mcgraw-hill Series Economics)

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, economics and related others by exploring similar questions and additional content below.Similar questions

- Suppose research at Panasonic reveals that prospective buyers are anxious about buying high definition television sets. What strategies might you recommend to the company to reduce consumer anxietyarrow_forwardOne method of solving this problem is through signaling. Signaling is a strategy one uses when they have information. The goal is to use a signal to convince the buyer that the good or service that is being sold is quality and will meet the buyer's wants. Offer an example of a company that uses a signal to help sell its product. What is the signal? What information is the signal trying to convey? Do you think the signal is effective? Why or why not? Does this signal improve market efficiency? Why or why not?arrow_forwardAn advertisement in the local paper offers a "fully loaded" car that is only six months old and has only been driven 5,000 miles at a price that is 20 percent lower than the average selling price of a brand new car with the same options. Use precise economic terminology to explain whether this discount most likely reflects a "fantastic deal" or something else.arrow_forward

- Suppose a firm sells two goods, Good A and Good B. Use the following information to Calculate the mark-up and the profit-maximizing price that the firm should change for Good B. Profit maximizing price of Good A = $6000 MC at profit-maximizing level of output of Good A = $1200 MC at profit-maximizing level of output of Good B = $400 Total revenue of Good A = $80000 Total revenue of Good B = $68000 Rothschild index of Good B = 0.6 Price elasticity of the market demand for Good B = -1.2arrow_forwardSuppose Brian is in the market for a used textbook and the campus bookstore is having a sale. If the initial price of the used book is $75$75 and the discounted price is $50$50, what is the percentage change in the book price? Round your answer to two places after the decimal. percentage change:arrow_forwardWhich statement is TRUE? Group of answer choices If there are no congestion or network effects, changes in preferences affect the market demand curve but not individual demand curves. If there are no congestion or network effects, changes in income affect the market demand curve but not individual demand curves. If there are no congestion or network effects, changes in the number of buyers affect the market demand curve but not individual demand curves. If there are no congestion or network effects, changes in the prices of related goods affect the market demand curve but not individual demand curves.arrow_forward

- What is the difference between a price strategy and a price tactic? Give an example.arrow_forwardIn economics, customer sorting rules are often applied to understand how customers choose among various options based on their preferences and the available information. Which of the following best describes a common customer sorting rule? A. Price Maximization Rule B. Utility Maximization Rule C. Information Aversion Rule D. Brand Loyalty Rule Please refrain from offering handwritten solutions. Please ensure that your response maintains accuracy and quality to avoid receiving a downvote. Take care of plagiarism. Answer completely.arrow_forwardA supplier is selling tomatoes in two cities, Antalya and Istanbul. It costs him 1 TRY per kg of tomatoes delivered in each city. Let p1 be the price of a kg of tomatoes in Antalya and p2 be the price of a kg tomatoes in Istanbul. The price-response curves in each city: Antalya: d1(p1) = 500 - 100p1 Istanbul: d2(p2) = 1,200 - 200p2 Assuming the supplier can charge any price he likes, what prices should be charged for a kg of tomatoes in Antalya and Istanbul to maximize total contribution? What are the corresponding demands, revenues, and total contributions in each city? What is the total demand, total revenue, and total contribution over the two cities?arrow_forward

- Seven years ago, you started a cross-town delivery service. You have two types of deliveryservices. You have a small parcel service for anything that is flat and measures less than 11x17. You have a package service using a 100 lb capacity bike trailer for anything weighting up to 10lbs. Initially, you charged the same price for each service, but since the beginning of the Covid19 pandemic you have seen an increased in the demand for your package service. The demand for the package services seems to be more inelastic than the demand for parcels. You are now wondering if you should charge different prices for the parcel and package service or should you segment the market and charge two different prices? Complete the tables below and determine the best price strategy: price the services differently in each segment; or continue the one price policy? The Parcels Market Price Parcels TR MR TC MC MR-MC…arrow_forwardSeven years ago, you started a cross-town delivery service. You have two types of deliveryservices. You have a small parcel service for anything that is flat and measures less than 11x17. You have a package service using a 100 lb capacity bike trailer for anything weighting up to 10lbs. Initially, you charged the same price for each service, but since the beginning of the Covid19 pandemic you have seen an increased in the demand for your package service. The demand for the package services seems to be more inelastic than the demand for parcels. You are now wondering if you should charge different prices for the parcel and package service or should you segment the market and charge two different prices? Complete the tables below and determine the best price strategy: price the services differently in each segment; or continue the one price policy? The Packages Market Price Packages TR MR TC MC…arrow_forwardSeven years ago, you started a cross-town delivery service. You have two types of deliveryservices. You have a small parcel service for anything that is flat and measures less than 11x17. You have a package service using a 100 lb capacity bike trailer for anything weighting up to 10lbs. Initially, you charged the same price for each service, but since the beginning of the Covid19 pandemic you have seen an increased in the demand for your package service. The demand for the package services seems to be more inelastic than the demand for parcels. You are now wondering if you should charge different prices for the parcel and package service or should you segment the market and charge two different prices? Complete the tables below and determine the best price strategy: price the services differently in each segment; or continue the one price policy? Combined Parcels & PackagesPrice Parcels and Packages TR MR TC MC MR-MC…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Managerial Economics: A Problem Solving ApproachEconomicsISBN:9781337106665Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike ShorPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Economics (MindTap Course List)EconomicsISBN:9781337617383Author:Roger A. ArnoldPublisher:Cengage Learning

Managerial Economics: A Problem Solving Approach

Economics

ISBN:9781337106665

Author:Luke M. Froeb, Brian T. McCann, Michael R. Ward, Mike Shor

Publisher:Cengage Learning

Economics (MindTap Course List)

Economics

ISBN:9781337617383

Author:Roger A. Arnold

Publisher:Cengage Learning

Decision Tree Analysis - Intro and Example with Expected Monetary Value; Author: Vincent Stevenson;https://www.youtube.com/watch?v=cbCsCQ4l4Zs;License: Standard Youtube License