Videos

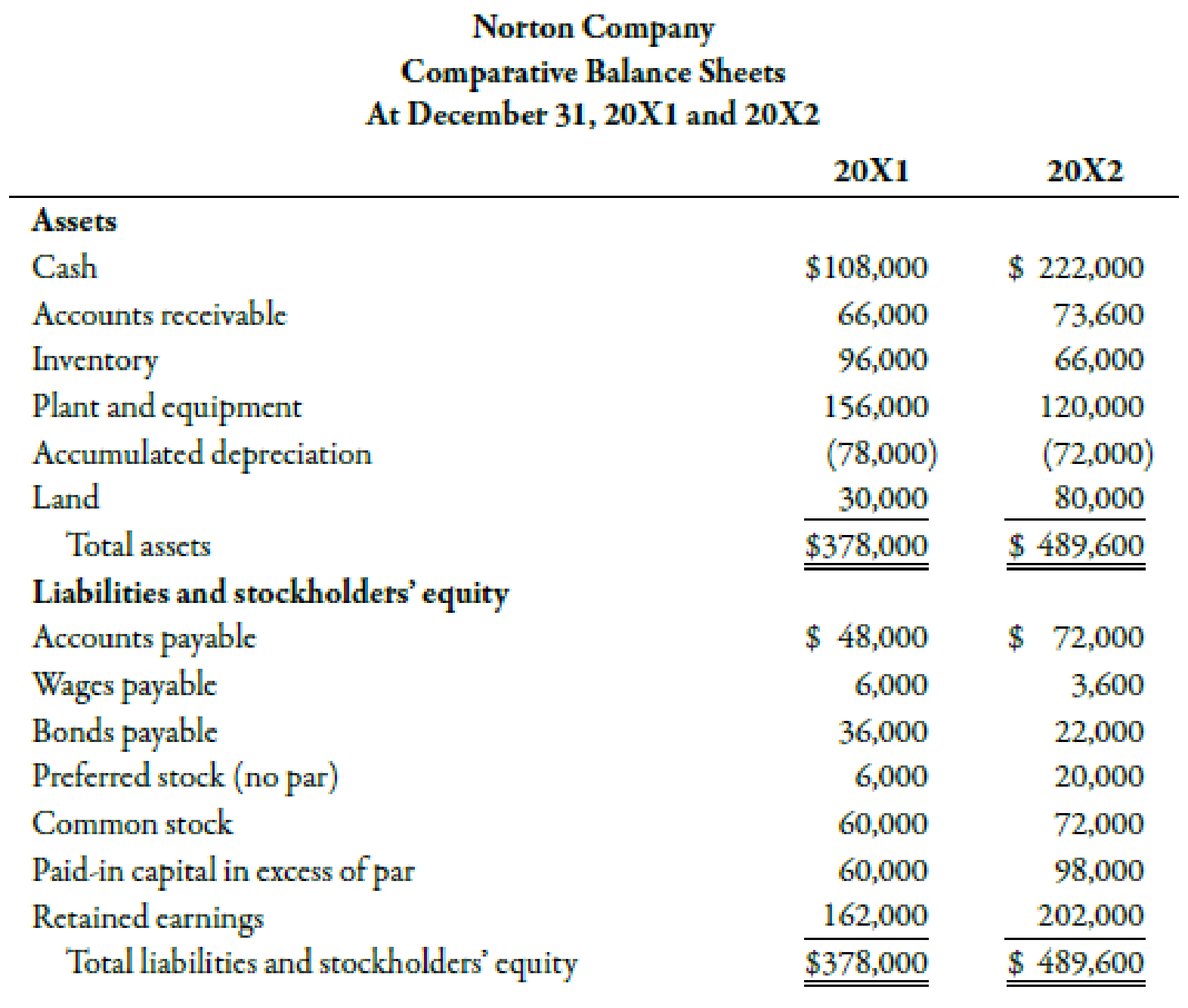

During 20X2, Norton Company had the following transactions:

- a. Cash dividends of $20,000 were paid.

- b. Equipment was sold for $9,600. It had an original cost of $36,000 and a book value of $18,000. The loss is included in operating expenses.

- c. Land with a fair market value of $50,000 was acquired by issuing common stock with a par value of $12,000.

- d. One thousand shares of

preferred stock (no par) were sold for $14 per share.

Norton provided the following income statement (for 20X2) and comparative balance sheets:

Required:

Prepare a worksheet for Norton Company.

Construct a worksheet for the N Company.

Explanation of Solution

Worksheet:

The chart prepared in a spreadsheet format as a helping tool in accounting is known as worksheet. With the help of worksheet, a cash flow statement can be prepared with less confusion and complexity.

The worksheet for the N Company is shown in the table below:

| Worksheet: N Company | ||||

| At December 31, 20X2 | ||||

| Transactions | ||||

| Particulars | 20X1 ($) | Debit ($) | Credit ($) | 20X2 ($) |

| Assets: | ||||

| Cash | 108,000 | (1) 114,000 | 222,000 | |

| Accounts receivable | 66,000 | (2) 7,600 | 73,600 | |

| Inventory | 96,000 | (3) 30,000 | 66,000 | |

| Plant and equipment | 156,000 | (4) 36,000 | 120,000 | |

| Accumulated depreciation | (78,000) | (4) 18,000 | (5) 12,000 | (72,000) |

| Land | 30,000 | (6) 50,000 | 80,000 | |

| Total assets | 378,000 | 489,600 | ||

| Liabilities and stockholder’s equity: | ||||

| Accounts payable | 48,000 | (7) 24,000 | 72,000 | |

| Wages payable | 6,000 | (8) 2,400 | 3,600 | |

| Bonds payable | 36,000 | (9) 14,000 | 22,000 | |

| Preferred stock | 6,000 | (10) 14,000 | 20,000 | |

| Common stock | 60,000 | (11) 12,000 | 72,000 | |

| Paid-in capital in excess of par | 60,000 | (11) 38,000 | 98,000 | |

| Retained earnings | 162,000 | (13) 20,000 | (12) 60,000 | 202,000 |

| Total liabilities and stockholder’s equity | 378,000 | 489,600 | ||

Table (1)

The analysis of transactions is as follows:

(1). Change in cash:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cash | 114,000 | ||

| Net increase in cash | 114,000 | ||

| (Being the change in cash recorded) |

Table (2)

Increase in accrual cash balance by $114,000 from the beginning to the end of the year is recorded.

(2). Change in accounts receivable:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Accounts receivable | 7,600 | ||

| Operating cash | 7,600 | ||

| (Being the increase in accounts receivable recorded) |

Table (3)

Increase in accounts receivable by $7,600 is recognized on the income statement but is not collected. This cash inflow should be adjusted in the net income.

(3). Decrease in inventory:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Operating cash | 30,000 | ||

| Inventory | 30,000 | ||

| (Being the increase in inventory recorded) |

Table (4)

With decrease in inventory by $30,000, the operating cash is increased. The decrease in inventory does not show an outflow of cash.

(4). Sale of equipment:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Operating cash | 8,400 | ||

| Cash from investing activities | 9,600 | ||

| Accumulated depreciation | 18,000 | ||

| Plant and equipment | 36,000 | ||

| (Being the loss on sale of equipment recorded) |

Table (5)

The operating cash flows are increased by $8,400; so, the loss on sale should be added back to the net income for the adjustment. The cash from investing activities records the value at which the equipment is sold which is $9,600. The accumulated depreciation is debited to record the expense. The plant and equipment account is credited to record the original cost of the equipment.

(5). Accumulated depreciation expense:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Operating cash | 6,000 | ||

| Accumulated depreciation | 6,000 | ||

| (Being the accumulated depreciation recorded) |

Table (6)

There is net decrease in accumulated depreciation of $6,000

(6). Land for common stock:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Land | 50,000 | ||

| Noncash investing activities | 50,000 | ||

| (Being fair value of land recorded) |

Table (7)

Land account is debited with the fair value at which land is acquired. The noncash investing activities is credited with the amount to record the cash inflow by investing activities.

(7). Accounts payable:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Operating cash | 24,000 | ||

| Accounts payable | 24,000 | ||

| (Being the increase in accounts payable recorded) |

Table (8)

The increase in accounts payable by $24,000 shows that all the purchases were not from cash. The increase in accounts payable should be added back to the net income. The increase in liability is recorded, hence it is credited.

(8). Wages payable:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Wages payable | 2,400 | ||

| Operating cash | 2,400 | ||

| (Being the decrease in wages payable recorded) |

Table (9)

The decrease in accounts payable shows that the cash outflow is more than the wages expense recognized in the year by $2,400. The decrease in liability is recorded, hence wages payable is debited and operating cash is credited.

(9). Bonds payable:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Bonds payable | 14,000 | ||

| Cash flow from financing activities | 14,000 | ||

| (Being the decrease in bonds payable recorded) |

Table (10)

The decrease in bonds payable by $14,000 shows a cash outflow from financing activities. With the decrease in bonds payable there is a reduction in debt.

(10). Preferred stock:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Cash flow from financing activities | 14,000 | ||

| Preferred stock | 14,000 | ||

| (Being the issuance of preferred stock recorded) |

Table (11)

The cash flow from financing activities records an inflow with the issuance of preferred stock.

(11). Land for common stock:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Noncash investing activities | 50,000 | ||

| Common stock | 12,000 | ||

| Paid-in capital in excess of par | 38,000 | ||

| (Being the amount of acquisition of land recorded) |

Table (12)

The noncash investing activity is recorded with the fair value of the land. The amount which is obtained by issuing the common stock is credited and the excess amount is credited in the paid-in capital.

(12). Net income:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Operating cash | 60,000 | ||

| Retained earnings | 60,000 | ||

| (Being the amount of net income recorded) |

Table (13)

The value of net income is recorded in the section of operating cash flows.

(13). Payment of dividends:

| Date | Account Title and Explanation |

Debit ($) |

Credit ($) |

| Retained earnings | 20,000 | ||

| Cash flow from financing activities | 20,000 | ||

| (Being the payment of dividends recorded) |

Table (14)

The amount by which payment of dividends is made is debited from the retained earnings. As payment of dividends is a cash outflow as financing activity, cash flow from financing activity is credited.

The final step is the cash flow statement which is prepared from the worksheet. The worksheet derived statement is shown in the table below:

| N Company | ||

| Statement of Cash Flows | ||

| For the year ended December 31, 20X2 | ||

| Cash flows from operating activities: | ||

| Debit ($) | Credit ($) | |

| Net income | (12) 60,000 | |

| Depreciation expense | (5) 12,000 | |

| Loss on sale of equipment | (4) 8,400 | |

| Decrease in inventory | (3) 30,000 | |

| Increase in accounts payable | (7) 24,000 | |

| Increase in accounts receivable | (2) 7,600 | |

| Decrease in wages payable | (8) 2,400 | |

| Cash flows from investing activities: | ||

| Sale of equipment | (4) 9,600 | |

| Cash flows from financing activities: | ||

| Reduction in bonds payable | (9) 14,000 | |

| Payment of dividends | (13) 20,000 | |

| Issuance of preferred stock | (10) 14,000 | |

| Net increase in cash | (1) 114,000 | |

| Noncash investing and financing activities: | ||

| Land acquired with common stock | (11) 50,000 | (6) 50,000 |

Table (15)

Want to see more full solutions like this?

Chapter 14 Solutions

Bundle: Managerial Accounting: The Cornerstone of Business Decision-Making, Loose-Leaf Version, 7th + CengageNOWv2, 1 term (6 months) Printed Access Card

- During 20X2, Evans Company had the following transactions: a. Cash dividends of 6,000 were paid. b. Equipment was sold for 2,880. It had an original cost of 10,800 and a book value of 5,400. The loss is included in operating expenses. c. Land with a fair market value of 15,000 was acquired by issuing common stock with a par value of 3,600. d. One thousand shares of preferred stock (no par) were sold for 4.20 per share. Evans provided the following income statement (for 20X2) and comparative balance sheets: Required: Prepare a worksheet for Evans Company.arrow_forwardBalance sheets for Brierwold Corporation follow: Additional transactions were as follows: a. Purchased equipment costing 50,000. b. Sold equipment costing 60,000, with a book value of 25,000, for 40,000. c. Retired preferred stock at a cost of 110,000. (The premium is debited to Retained Earnings.) d. Issued 10,000 shares of common stock (par value, 4) for 10 per share. e. Reported a loss of 15,000 for the year. f. Purchased land for 50,000. Required: Prepare a statement of cash flows using the worksheet approach. Use the indirect method to prepare the statement.arrow_forwardBalance sheets for Brierwold Corporation follow: Additional transactions were as follows: a. Purchased equipment costing 50,000. b. Sold equipment costing 60,000, with a book value of 25,000, for 40,000. c. Retired preferred stock at a cost of 110,000. (The premium is debited to Retained Earnings.) d. Issued 10,000 shares of common stock (par value, 4) for 10 per share. e. Reported a loss of 15,000 for the year. f. Purchased land for 50,000. Required: Prepare a statement of cash flows using the indirect method.arrow_forward

- Assume that as of January 1, 20Y8, Sylvester Con- suiting has total assets of $500,000 and total assets of $150,000. As of December 31, 20Y8, Sylvester has total liabilities of $200,000 and total stockholders’ equity of $400,000. (a) What was Sylvester’s stockholders’ equity as of January 1, 20Y8? (b) Assume that Sylvester did not pay any dividends during 20Y8. What was the amount of net income for 20Y8?arrow_forwardFor the current year, Vidalia Company reported revenues of 250,000 and expenses of 225,000. At the beginning of the year, its retained earnings had a balance of 95,000. During the year, Vidalia paid 11,000 dividends to shareholders. Its contributed capital was 56,000 at the beginning of the year, and it did not issue any new stock during the year. Vidalias assets total 237,500 on December 31 of the current year. What are Vidalias total liabilities on December 31 of the current year?arrow_forwardMontana Incorporated began the year with a retained earnings balance of $50,000. The company paid a total of $5,000 in dividends and experienced a net loss of $25,000 this year. What is the ending retained earnings balance?arrow_forward

- During 20X1, Craig Company had the following transactions: a. Purchased 300,000 of 10-year bonds issued by Makenzie Inc. b. Acquired land valued at 105,000 in exchange for machinery. c. Sold equipment with original cost of 810,000 for 495,000; accumulated depreciation taken on the equipment to the point of sale was 270,000. d. Purchased new machinery for 180,000. e. Purchased common stock in Lemmons Company for 82,500. Required: 1. Prepare the net cash from investing activities section of the statement of cash flows. 2. CONCEPTUAL CONNECTION Usually, the net cash from investing activities is negative. How can Craig cover this negative cash flow? What other information would you like to have to make this decision?arrow_forwardFarmington Corporation began the year with a retained earnings balance of $20,000. The company paid a total of $3,000 in dividends and earned a net income of $60,000 this year. What is the ending retained earnings balance?arrow_forwardChasse Building Supply Inc. reported net cash provided by operating activities of $243,000, capital expenditures of $112,900, cash dividends of $35,800, and average maturities of long-term debt over the next 5 years of $122,300. What is Chasses free cash flow and cash flow adequacy ratio? a. $94,300 and 0.77, respectively c. $130,100 and 1.06, respectively b. $94,300 and 0.82, respectively d. $165,900 and 1.36, respectivelyarrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning

Intermediate Accounting: Reporting And AnalysisAccountingISBN:9781337788281Author:James M. Wahlen, Jefferson P. Jones, Donald PagachPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning

Survey of Accounting (Accounting I)AccountingISBN:9781305961883Author:Carl WarrenPublisher:Cengage Learning