Videos

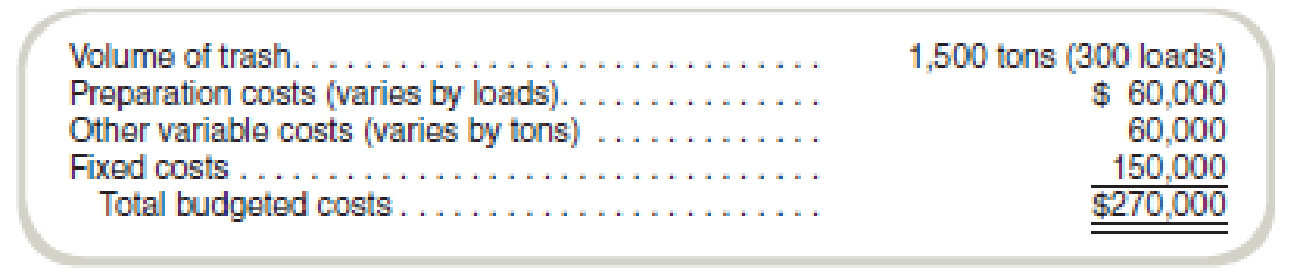

Mathes Corporation manufactures paper products. The company operates a landfill, which it uses to dispose of nonhazardous trash. The trash is hauled from the two nearby manufacturing facilities in trucks that can carry up to five tons of trash in a load. The landfill operation requires certain preparation activities regardless of the amount of trash in a truck (i.e., for each load). The budget for the landfill for next year follows:

Mathes is considering making the landfill a profit center and charging the manufacturing plants for disposal of the trash. The landfill has sufficient capacity to operate for at least the next 20 years. Other landfills are available in the area (both private and municipal), and each plant would be free to decide which landfill to use.

Required

- a. What transfer pricing rule should Mathes implement at the landfill so that its plant managers would independently make decisions regarding landfill use that would be in the company’s best interests?

- b. Illustrate your rule by computing the transfer price that would be applied to a four-ton load of trash from one of the plants.

Want to see the full answer?

Check out a sample textbook solution

Chapter 15 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Biotechtron, Inc., has two research laboratories in the Southwest, one in Yuma, Arizona, and the other in Bernalillo, New Mexico. The owner of Biotechtron centralized the legal services function in the Yuma office and had both laboratories send any legal questions or issues to the Yuma office. The legal services support center has budgeted fixed costs of 160,000 per year and a budgeted variable rate of 65 per hour of professional time. The normal usage of the legal services center is 2,600 hours per year for the Yuma office and 1,400 hours per year for the Bernalillo office. This corresponds to the expected usage for the coming year. Required: 1. Determine the amount of legal services support center costs that should be assigned to each office. 2. Since the offices produce services, not tangible products, what purpose is served by allocating the budgeted costs? 3. Now, assume that during the year, the legal services center incurred actual fixed costs of 163,000 and actual variable costs of 272,400. It delivered 4,180 hours of professional time2,580 hours to Yuma and 1,600 hours to Bernalillo. Determine the amount of the legal services centers costs that should be allocated to each office. Explain the purposes of this allocation. 4. Did the costs allocated differ from the costs incurred by the legal services center? If so, why?arrow_forwardNovo, Inc., wants to develop an activity flexible budget for the activity of moving materials. Novo uses eight forklifts to move materials from receiving to stores. The forklifts are also used to move materials from stores to the production area. The forklifts are obtained through an operating lease that costs 18,000 per year per forklift. Novo employs 25 forklift operators who receive an average salary of 50,000 per year, including benefits. Each move requires the use of a crate. The crates are used to store the parts and are emptied only when used in production. Crates are disposed of after one cycle (two moves), where a cycle is defined as a move from receiving to stores to production. Each crate costs 1.80. Fuel for a forklift costs 3.60 per gallon. A gallon of gas is used every 20 moves. Forklifts can make three moves per hour and are available for 280 days per year, 24 hours per day (the remaining time is downtime for various reasons). Each operator works 40 hours per week and 50 weeks per year. Required: 1. Prepare a flexible budget for the activity of moving materials, using the number of cycles as the activity driver. 2. Calculate the activity capacity for moving materials. Suppose Novo works at 80 percent of activity capacity and incurs the following costs: Prepare the budget for the 80 percent level and then prepare a performance report for the moving materials activity. 3. Calculate and interpret the volume variance for moving materials. 4. Suppose that a redesign of the plant layout reduces the demand for moving materials to one-third of the original capacity. What would be the budget formula for this new activity level? What is the budgeted cost for this new activity level? Has activity performance improved? How does this activity performance evaluation differ from that described in Requirement 2? Explain.arrow_forwardIngles Corporation is a manufacturer of tables sold to schools, restaurants, hotels, and other institutions. The table tops are manufactured by Ingles, but the table legs are purchased from an outside supplier. The Assembly Department takes a manufactured table top and attaches the four purchased table legs. It takes 16 minutes of labor to assemble a table. The company follows a policy of producing enough tables to ensure that 40 percent of next months sales are in the finished goods inventory. Ingles also purchases sufficient materials to ensure that materials inventory is 60 percent of the following months scheduled production. Ingless sales budget in units for the next quarter is as follows: Ingless ending inventories in units for July 31 are as follows: Required: 1. Calculate the number of tables to be produced during August. 2. Disregarding your response to Requirement 1, assume the required production units for August and September are 2,100 and 1,900, respectively, and the July 31 materials inventory is 4,000 units. Compute the number of table legs to be purchased in August. 3. Assume that Ingles Corporation will produce 2,340 units in September. How many employees will be required for the Assembly Department in September? (Fractional employees are acceptable since employees can be hired on a part-time basis. Assume a 40-hour week and a 4-week month.) (CMA adapted)arrow_forward

- Bienestar, Inc., has two plants that manufacture a line of wheelchairs. One is located in Kansas City, and the other in Tulsa. Each plant is set up as a profit center. During the past year, both plants sold their tilt wheelchair model for 1,620. Sales volume averages 20,000 units per year in each plant. Recently, the Kansas City plant reduced the price of the tilt model to 1,440. Discussion with the Kansas City manager revealed that the price reduction was possible because the plant had reduced its manufacturing and selling costs by reducing what was called non-value-added costs. The Kansas City manufacturing and selling costs for the tilt model were 1,260 per unit. The Kansas City manager offered to loan the Tulsa plant his cost accounting manager to help it achieve similar results. The Tulsa plant manager readily agreed, knowing that his plant must keep pacenot only with the Kansas City plant but also with competitors. A local competitor had also reduced its price on a similar model, and Tulsas marketing manager had indicated that the price must be matched or sales would drop dramatically. In fact, the marketing manager suggested that if the price were dropped to 1,404 by the end of the year, the plant could expand its share of the market by 20 percent. The plant manager agreed but insisted that the current profit per unit must be maintained. He also wants to know if the plant can at least match the 1,260 per-unit cost of the Kansas City plant and if the plant can achieve the cost reduction using the approach of the Kansas City plant. The plant controller and the Kansas City cost accounting manager have assembled the following data for the most recent year. The actual cost of inputs, their value-added (ideal) quantity levels, and the actual quantity levels are provided (for production of 20,000 units). Assume there is no difference between actual prices of activity units and standard prices. Required: 1. Calculate the target cost for expanding the Tulsa plants market share by 20 percent, assuming that the per-unit profitability is maintained as requested by the plant manager. 2. Calculate the non-value-added cost per unit. Assuming that non-value-added costs can be reduced to zero, can the Tulsa plant match the Kansas City per-unit cost? Can the target cost for expanding market share be achieved? What actions would you take if you were the plant manager? 3. Describe the role that benchmarking played in the effort of the Tulsa plant to protect and improve its competitive position.arrow_forwardQuality Clothing, Inc., produces skorts and jumper uniforms for schoolchildren. In the process of cutting out the cloth pieces for each product, a certain amount of scrap cloth is produced. Quality has been selling this cloth scrap to Jorges Scrap Warehouse for $3.25 per pound. Last year, the company sold 40,000 lb. of scrap, which would be enough to make 10,000 teddy bears that the management of Quality is now interested in producing. Their processes would need some reprogramming, particularly in the cutting and stitching processes, but it would require no additional worker training. However, new packaging would be needed. The total variable cost to produce the teddy bears $3.85. Fixed costs would increase by $95,000 per year for the lease of the packaging equipment and Quality estimates it could produce and sell 10,000 teddy bears per year. Finished teddy bears could be sold for $18.00 each. Should Quality continue to sell the scrap cloth or should Quality process the scrap into teddy bears to sell?arrow_forwardVenus Creations sells window treatments (shades, blinds, and awnings) to both commercial and residential customers. The following information relates to its budgeted operations for the current year. Commercial Residential Revenues $300,700 $483,000 Direct materials costs $29,500 $50,500 Direct labor costs 100,400 289,500 Overhead costs 90,900 220,800 150,000 490,000 Operating income (loss) $79,900 $(7,000) The controller, Peggy Kingman, is concerned about the residential product line. She cannot understand why this line is not more profitable given that the installations of window coverings are less complex for residential customers. In addition, the residential client base resides in close proximity to the company office, so travel costs are not as expensive on a per client visit for residential customers. As a result, she has decided to take a closer look at the overhead costs assigned to…arrow_forward

- Biotechtron, Inc., has two research laboratories in the Southwest, one in Yuma, Arizona, and theother in Bernalillo, New Mexico. The owner of Biotechtron centralized the legal services functionin the Yuma office and had both laboratories send any legal questions or issues to the Yuma office. The legal services support center has budgeted fixed costs of $160,000 per year and a budg-eted variable rate of $65 per hour of professional time. The normal usage of the legal services cen-ter is 2,600 hours per year for the Yuma office and 1,400 hours per year for the Bernalillo office. This corresponds to the expected usage for the coming year.Required:1. Determine the amount of legal services support center costs that should be assigned to eachoffice. 2. Since the offices produce services, not tangible products, what purpose is served by allocat-ing the budgeted costs? 3. Now, assume that during the year, the legal services center incurred actual fixed costs of$163,000 and actual variable…arrow_forwardThe F Inc.’s materials manager is considering the installation of a just-in-time (JIT) inventory system for L-20, one of the chemicals used in the production process. Currently, the chemical is purchased for $30 each pound. The firm uses 4,800 pounds L-20 per year. The controller estimates that it costs $150 to place and receive a typical order of L-20. The annual cost of storing L-20 is $1 per pound. F Inc.’s manufacturing engineering team identifies the following effects of adopting a JIT inventory system: 1) F Inc. will order 100 pounds L-20 each time. 2) The cost of placing an order for L-20 will be reduced to $20. 3) Suppliers would add $4 to the price per pound for frequent deliveries. 4) Currently there is a defect-assessment cost of $120,000 per year. This cost is expected a reduction of 20% under the JIT system. F Inc. requires a 10% annual rate of return on investment Required: From a financial perspective, determine whether it is in the best interest of F to…arrow_forwardThe Johnson Company pays $1,650 a month to a trucker to haul wastepaper and cardboard to the city dump. The material could be recycled if the company were to buy a $50,000 press baler and spend $20,000 a year for one worker to operate the baler. The baler has an estimated useful life of 14 years, with no şalvage value. Strapping material would cost $1600 per year for the estimated 650 bails a year that would be produced. A wastepaper company will pick up the bales at the plant and pay Johnson for them. In order to justify the baler, how much should Johnson charge the wastepaper company for each bale? Use an interest rate of 8% per year.________.arrow_forward

- The Science Institute has three departments: Biology, Chemistry, and Physics. The institute's controller wants to estimate the cost of operating each department. He has identified several indirect costs that must be allocated to each department including $52,000 of indirect salaries, $9,000 of office supplies, and $41,000 of office rent. There are 500 students in the biology department, 200 in chemistry and 300 in physics. The director of the Institute wants to know how much of the indirect cost to allocate to each department. Based on this informationarrow_forwardThe Science Institute has three departments: Biology, Chemistry, and Physics. The institute's controller wants to estimate the cost of operating each department. He has identified several indirect costs that must be allocated to each department including $52,000 of indirect salaries, $9,000 of office supplies, and $41,000 of office rent. There are 500 students in the biology department, 200 in chemistry and 300 in physics. The director of the Institute wants to know how much of the indirect cost to allocate to each department. Based on this information the amount of the cost to be allocated is $102,000. the indirect cost is the "allocation base". the students are the "cost objects". All of the answers are correct.arrow_forwardThe head of operations of a manufacturing company has conducted an analysis with respect to the capacity of his production line. The major findings are the following: Theoretical capacity is 530 units per day. The effective capacity is 515 units per day The process capacity is 450 units per day. Two projects have been proposed to increase the capacity. The first proposal focuses on improving maintenance in order to reduce machine breakdowns. The second proposal focuses on increasing the capacity of the inventory buffer between various stages. Given that there is only enough budget to implement one of the proposals, which proposal should be selected based on the given information. Clearly motivate your answer. Please do fast.. ASAP ..fast pleasearrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College