Videos

Western States Supply, Inc. (WSS), consists of three divisions—California, Northwest, and Southwest—that operate as if they were independent companies. Each division has its own sales force and production facilities. Each division manager is responsible for sales, cost of operations, acquisition and financing of divisional assets, and

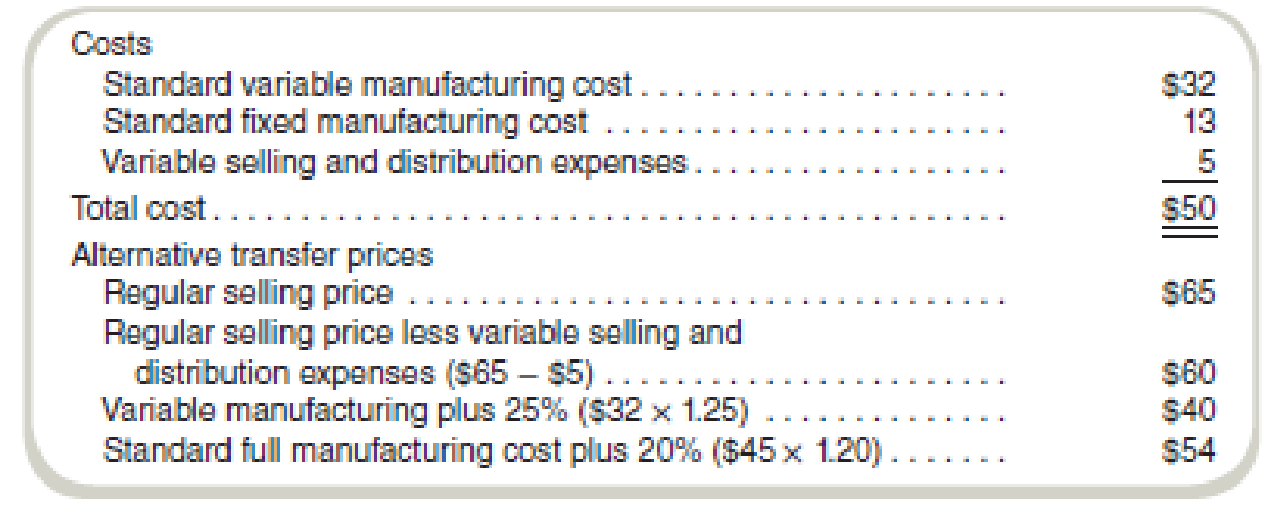

Southwest has just been awarded a contract for a product that uses a component manufactured by outside suppliers as well as by Northwest, which is operating well below capacity. Southwest used a cost figure of $37 for the component in preparing its bid for the new product. Northwest supplied this cost figure in response to Southwest’s request for the

Northwest’s regular selling price for the component that Southwest needs is $65. Northwest’s management indicated that it could supply Southwest the required quantities of the component at the regular selling price less variable selling and distribution expenses. Southwest management responded by offering to pay standard variable manufacturing cost plus 25 percent.

The two divisions have been unable to agree on a transfer price. Corporate management has never established a transfer price policy. The corporate controller suggested a price equal to the standard full manufacturing cost (that is, no selling and distribution expenses) plus a 20 percent markup. The two division managers rejected this price because each considered it grossly unfair.

The unit cost structure for the Northwest component and the suggested prices follow

Required

- a. Discuss the effect that each of the proposed prices could have on the attitude of Northwest’s management toward intracompany business.

- b. Is the negotiation of a price between Northwest and Southwest a satisfactory method to solve the transfer price problem? Explain your answer.

- c. Should WSS’s corporate management become involved in this transfer price controversy? Explain your answer.

Want to see the full answer?

Check out a sample textbook solution

Chapter 15 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Grate Care Company specializes in producing products for personal grooming. The company operates six divisions, including the Hair Products Division. Each division is treated as an investment center. Managers are evaluated and rewarded on the basis of ROI performance. Only those managers who produce the best ROIs are selected to receive bonuses and to fill higher-level managerial positions. Fred Olsen, manager of the Hair Products Division, has always been one of the top performers. For the past two years, Freds division has produced the largest ROI; last year, the division earned an operating income of 2.56 million and employed average operating assets valued at 16 million. Fred is pleased with his divisions performance and has been told that if the division does well this year, he will be in line for a headquarters position. For the coming year, Freds division has been promised new capital totaling 1.5 million. Any of the capital not invested by the division will be invested to earn the companys required rate of return (9 percent). After some careful investigation, the marketing and engineering staff recommended that the division invest in equipment that could be used to produce a crimping and waving iron, a product currently not produced by the division. The cost of the equipment was estimated at 1.2 million. The divisions marketing manager estimated operating earnings from the new line to be 156,000 per year. After receiving the proposal and reviewing the potential effects, Fred turned it down. He then wrote a memo to corporate headquarters, indicating that his division would not be able to employ the capital in any new projects within the next eight to 10 months. He did note, however, that he was confident that his marketing and engineering staff would have a project ready by the end of the year. At that time, he would like to have access to the capital. Required: 1. Explain why Fred Olsen turned down the proposal to add the capability of producing a crimping and waving iron. Provide computations to support your reasoning. 2. Compute the effect that the new product line would have on the profitability of the firm as a whole. Should the division have produced the crimping and waving iron? 3. Suppose that the firm used residual income as a measure of divisional performance. Do you think Freds decision might have been different? Why? 4. Explain why a firm like Grate Care might decide to use both residual income and return on investment as measures of performance. 5. Did Fred display ethical behavior when he turned down the investment? In discussing this issue, consider why he refused to allow the investment.arrow_forwardThe Mega Supply Corporation has three divisions: Commercial Products, Consumer Products, and Corporate Offices, which are located in Hatfield, South Carolina; Palo Alto, California; and Tulsa, Oklahoma, respectively. The Commercial Products division deals exclusively in sales of industrial products and supplies to business organizations. The Consumer Products division sells nonindustrial products to private consumers. Both divisions have dedicated inventory warehouses at their respective locations in Hatfield and Palo Alto. Because of the dissimilar nature of the commercial and consumer division product lines, they do not share customers or vendors. Currently Mega Supply uses a centralized database, which is located at their Corporate Division in Tulsa. Some relevant database tables and attributes are presented in the figure designated Problem 1. When customers contact their respective sales division, the sales clerk logs into the corporate database, checks credit, determines product availability, and creates a sales invoice. The corporate office typically bills the customer within 3 or 4 days and extends terms of net 30. Inventory control, AR processing, cash receipts, purchases from vendors and AP processing, and cash disbursements are performed by the corporate office. Due to Megas rapid growth, the company has seen a significant increase in sales and purchase transactions, which has resulted in excessive delays in processing transactions from the central database. Since customer service, including rapid response to customer inquiries and sales order processing, is a cornerstone of Megas business model, these delays are unacceptable. Required Mega wants to improve response time by distributing some parts of the corporate database while keeping other parts of it centralized. (A) Develop a schema for distributing Mega Supply Corporations database. Add new tables and attributes as needed but limit the schema to the tables needed to support sales, cash receipts, purchases/AP, and cash disbursements. In your schema, indicate whether tables are centralized, replicated, or partitioned. (B) Explain how the new system will operate.arrow_forwardFor the following situations identify whether the description is a centralized or decentralized organization. A. the United States Navy B. Farahs Dominos franchise store C. Dominos Pizza D. Middies Furniture, which is divided into separate operating units, such as living room, kitchen, flooring E. the local community college, which has a single payroll department, a single administrative headquarters, and a single human resources department since it flattened its organization structure F. Conner Corporation, which promotes managers from within the organization whenever possible and which has formal training programs for lower-level managersarrow_forward

- The three divisions of Yummy Foods are Snack Goods, Cereal, and Frozen Foods. The divisions are structured as investment centers. The following responsibility reports were prepared for the three divisions for the prior year: a. Which division is making the best use of invested assets and should be given priority for future capital investments? b. b. Assuming that the minimum acceptable return on new projects is 19%, would all investments that produce a return in excess of 19% be accepted by the divisions? Explain. c. c. Identify opportunities for improving the companys financial performance.arrow_forwardProfit center responsibility reporting for a service company Red Line Railroad Inc. has three regional divisions organized as profit centers. The chief executive officer (CEO) evaluates divisional performance, using operating income as a percent of revenues. The following quarterly income and expense accounts were provided from the trial balance as of December 31: The company operates three support departments: Shareholder Relations, Customer Support, and Legal. The Shareholder Relations Department conducts a variety of services for shareholders of the company. The Customer Support Department is the companys point of contact for new service, complaints, and requests for repair. The department believes that the number of customer contacts is a cost driver for this work. The Legal Department provides legal services for division management. The department believes that the number of hours billed is a cost driver for this work. The following additional information has been gathered: Instructions 1. Prepare quarterly income statements showing operating income for the three divisions. Use three column headings: East, West, and Central. 2. Identify the most successful division according to the profit margin. Round to the nearest whole percent. 3. Provide a recommendation to the CEO for a better method for evaluating the performance of the divisions. In your recommendation, identify the major weakness of the present method.arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forward

- The Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forwardThe Kelly-Elias Corporation, manufacturer of tractors and other heavy farm equipment, is organized along decentralized product lines, with each manufacturing division operating as a separate profit center. Each division manager has been delegated full authority on all decisions involving the sale of that division’s output both to outsiders and to other divisions of Kelly-Elias. Division C has in the past always purchased its requirement of a particular tractor-engine component from division A. However, when informed that division A is increasing its selling price to $135, division C’s manager decides to purchase the engine component from external suppliers. Division C can purchase the component for $115 per unit in the open market. Division A insists that, because of the recent installation of some highly specialized equipment and the resulting high depreciation charges, it will not be able to earn an adequate return on its investment unless it raises its price. Division A’s manager…arrow_forwardPhoenix Inc., a cellular communication company, has multiple business units, organized as divisions. Each division’s management is compensated based on the division’s operating income. Division A currently purchases cellular equipment from outside markets and uses it to produce communication systems. Division B produces similar cellular equipment that it sells to outside customers—but not to division A at this time. Division A’s manager approaches division B’s manager with a proposal to buy the equipment from division B. If it produces the cellular equipment that division A desires, division B will incur variable manufacturing costs of $60 per unit. Relevant Information about Division B Sells 90,000 units of equipment to outside customers at $130 per unit Operating capacity is currently 80%; the division can operate at 100% Variable manufacturing costs are $70 per unit Variable marketing costs are $8 per unit Fixed manufacturing costs are $900,000 Income per Unit for Division A…arrow_forward

- Goodworks Software operates stores within five regions. Regional managers are held accountable for marketing, advertising, and sales decisions, and all costs incurred within their region. In addition, regional managers decide whether new stores will open, where the stores will be located, and whether the stores will lease or purchase the facilities. Store managers, in contrast, are accountable for marketing, advertising, and sales decisions, and costs incurred within their stores. Ideally, on the basis of this information, what type of responsibility center should the software company use to evaluate its regions and stores? (1) Regions; (2) Stores (1) Profit center; (2) Profit center (1) Profit center; (2) Revenue center (1) Investment center; (2) Cost center (1) Investment center; (2) Profit center (1) Profit center; (2) Cost centerarrow_forwardGrael Technology has two divisions, Consumer and Commercial, and two corporate service departments, Tech Support and Purchasing. The corporate costs for the year ended December 31, 20Y7, are as follows: Tech Support Department $336,000 Purchasing Department 67,500 Other corporate administrative costs 448,000 Total corporate costs $851,500 The other corporate administrative costs include officers’ salaries and miscellaneous smaller costs required by the corporation. The Tech Support Department allocates the divisions for services rendered, based on the number of computers in the department, and the Purchasing Department allocates divisions for services, based on the number of purchase orders for each department. The usage of service by the two divisions is as follows: Tech Support Purchasing Consumer Division 300 computers 1,800 purchase orders Commercial Division 180 2,700 Total 480 computers 4,500 purchase orders The service department allocations…arrow_forwardBersatu Berhad splits into two divisions, A and B, each with their own cost and revenue streams. Each of the divisions is managed by a divisional manager who has the power to make all investment decisions within the division. The cost of capital for both divisions is 12%. Historically, investment decisions have been made by calculating the return on investment (ROI) of any opportunities and at present.A new manager who has recently been appointed in division A has argued that using residual income (RI) to make investment decisions would result in ‘better goal congruence’ throughout the company. Each division is currently considering the following separate investments: Project for Division A Project for Division B Capital requirement for investment RM 82.8 million RM40.6 million Sales generated by investment Rm44.6 million Rm21.8 million Net profit margin 28% 33% The company is seeking to maximise shareholder wealth. Required: Calculate both the return on investment and…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,