Fundamentals Of Cost Accounting (6th Edition)

6th Edition

ISBN: 9781259969478

Author: WILLIAM LANEN, Shannon Anderson, Michael Maher

Publisher: McGraw Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 17, Problem 43P

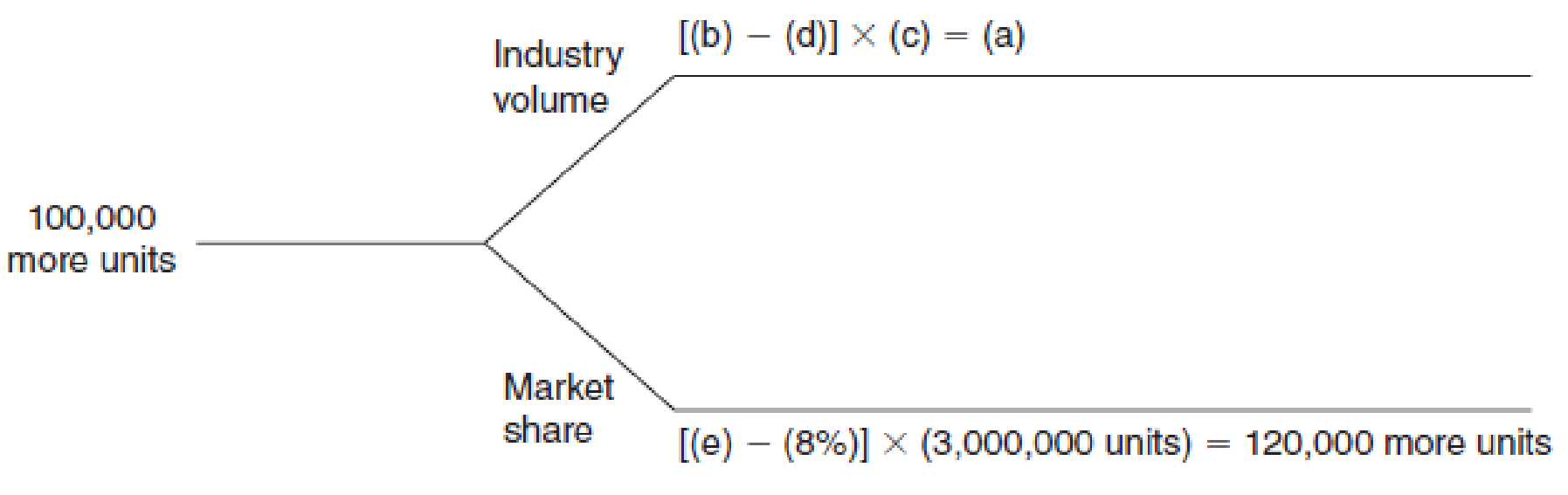

Industry Volume and Market Share: Missing Data

The following graph is similar to that in Exhibit 17.4.

Required

Find the missing amounts:

- a. Industry volume variance.

- b. Actual industry volume.

- c. Budgeted market share.

- d. Budgeted industry volume.

- e. Actual market share.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Management Accounting

Question (Qualitative Short Answer)

a. Why is the sales forecast the starting point in budgeting?

b. What is a perpetual budget?

c. Which is a better basis for evaluating actual results: budgeted performance or past performance? Why?

d. The materials price variance can be computed at what two different points in time? Which point is better and why?

e. What effect, if any, would you expect purchasing poor-quality materials to have on direct labor variances?

f. Distinguish between ideal and practical standards.

g. Costs associated with the quality of conformance can be broken down into four broad groups. What are these four groups and how do they differ?

h. What is likely the most effective way to reduce a company's total quality costs?

i. What are the three main uses of quality cost reports?

Which of the following is a limitation of the gross profit variance analysis?

a. The level of efficiency of asset management department can be computed and shown

b. It includes the amount invested in working capital

c. Measurement of the impact on gross profit due changes in sales volume cannot be determined

d. The gross profit variance analysis is limited only on the product attributable cost

Match the definition the term.

Terms:

Cost variance

Overhead cost variance

Price variance

Quantity variance

Standard costs

Sales budget

Production Budget

Balanced scorecard

Profit center

Cost center

Definitions:

1. A plan showing the units of goods to be sold and sales to be derived; usually starting pointing the budgeting process.

2. A system of performance measures, including the nonfinancial measures, used to asses manager performance.

3. A department that incurs cost and genrate revenues, such as a selling department

4. The difference between actual and budgeted sales or cost caused by the difference between the actual per unit and the budgeted price per unit.

5. The difference between actual cost and standard cost, made up of a price variance and a quantity variance.

6. The difference between the total overhead cost actually incurred and the total overhead cost applied to products

7. The difference between the actual budgeted cost caused by…

Chapter 17 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Ch. 17 - What complication arises in variance analysis when...Ch. 17 - Variance analysis can be useful in a manufacturing...Ch. 17 - How would you recommend accounting for variances...Ch. 17 - What does a manager learn by computing an industry...Ch. 17 - Why is there no efficiency variance for revenues?Ch. 17 - For what decisions would a manager want to know...Ch. 17 - If the sales activity or materials efficiency...Ch. 17 - Prob. 8RQCh. 17 - Prob. 9RQCh. 17 - What is the advantage of recognizing materials...

Ch. 17 - How could a professional sports firm use the mix...Ch. 17 - Prob. 12CADQCh. 17 - How could a hospital firm use the mix variance to...Ch. 17 - Prob. 14CADQCh. 17 - There is no reason to investigate favorable...Ch. 17 - Prob. 16CADQCh. 17 - Consider a firm in the sharing economy, such as...Ch. 17 - Prob. 18ECh. 17 - Prob. 19ECh. 17 - Prob. 20ECh. 17 - Variable Cost Variances: Materials Purchased and...Ch. 17 - Prob. 22ECh. 17 - Industry Volume and Market Share Variances DB Ice...Ch. 17 - Olive Tree Products sold 72,000 units during the...Ch. 17 - Prob. 25ECh. 17 - Sales Mix and Quantity Variances A-Zone Media...Ch. 17 - Prob. 27ECh. 17 - Sales Mix and Quantity Variances The restaurant at...Ch. 17 - Sales Mix and Quantity Variances Chow-4-Hounds...Ch. 17 - Materials Mix and Yield Variances Stacy, Inc.,...Ch. 17 - Materials Mix and Yield Variances Johns...Ch. 17 - Labor Mix and Yield Variances Matts Eat N Run has...Ch. 17 - Flexible Budgeting, Service Organization KB is a...Ch. 17 - Prob. 34ECh. 17 - Prob. 35ECh. 17 - Sales Price and Activity Variances EZ-Tax is a tax...Ch. 17 - Write a memo to the senior manager of EZ-Tax...Ch. 17 - Variable Cost Variances The standard direct labor...Ch. 17 - Refer to the information in Exercise...Ch. 17 - Prob. 40PCh. 17 - Variable Cost Variances: Materials Purchased and...Ch. 17 - Industry Volume and Market Share Variances:...Ch. 17 - Industry Volume and Market Share: Missing Data The...Ch. 17 - Sales Mix and Quantity Variances Lake Cellars...Ch. 17 - Analyze Performance for a Restaurant Dougs Diner...Ch. 17 - Nonmanufacturing Cost Variances FSBCU is a...Ch. 17 - Performance Evaluation in Service Industries Bay...Ch. 17 - Refer to the information in Problem...Ch. 17 - Prob. 49PCh. 17 - Refer to the data for the Peninsula Candy Company...Ch. 17 - Materials Mix and Yield Variances Plano Products...Ch. 17 - Pinnuck Products makes a liquid solvent using two...Ch. 17 - Labor Mix and Yield Variances Matthews Bros, is a...Ch. 17 - Refer to the information in Problem...Ch. 17 - Derive Amounts for Profit Variance Analysis...Ch. 17 - Flexible Budget Oak Hill Township operates a motor...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- The budget variance for variable production costs is broken down into quantity and price variances. Explain why the quantity variance is more useful for control purposes than the price variance.arrow_forwardA flexible budget______. A. predicts estimated revenues and costs at varying levels of production B. gives actual figures for selling price C. gives actual figures for variable and fixed overhead D. is not used in overhead variance calculationsarrow_forward(Appendix 10A) Which of the following items describes practices surrounding the recording of variances? a. All inventories are typically carried at standard. b. Unfavorable variances appear as debits. c. Favorable variances appear as credits. d. Immaterial variances are typically closed to Cost of Goods Sold. e. All of these.arrow_forward

- (Appendix 10A) Which of the following is true concerning labor variances that are not material in amount? a. They are closed to Cost of Goods Sold. b. They are prorated among Work in Process, Finished Goods, and Cost of Goods Sold. c. They are prorated among Materials, Work in Process, Finished Goods, and Cost of Goods Sold. d. They are reported on the balance sheet at the end of the year. e. All of these.arrow_forwardContinuous improvement is the governing principle of a lean accounting system. Following are several performance measures. Some of these measures would be associated with a traditional standard-costing accounting system, and some would be associated with a lean accounting system. a. Materials price variances b. Cycle time c. Comparison of actual product costs with target costs d. Materials quantity or efficiency variances e. Comparison of actual product costs over time (trend reports) f. Comparison of actual overhead costs, item by item, with the corresponding budgeted costs g. Comparison of product costs with competitors product costs h. Percentage of on-time deliveries i. First-time through j. Reports of value- and non-value-added costs k. Labor efficiency variances l. Days of inventory m. Downtime n. Manufacturing cycle efficiency (MCE) o. Unused (available) capacity variance p. Labor rate variance q. Using a sister plants best practices as a performance standard Required: 1. Classify each measure as lean or traditional (standard costing). If traditional, discuss the measures limitations for a lean environment. If it is a lean measure, describe how the measure supports the objectives of lean manufacturing. 2. Classify the measures into operational (nonfinancial) and financial categories. Explain why operational measures are better for control at the shop level (production floor) than financial measures. Should any financial measures be used at the operational level? 3. Suggest some additional measures that you would like to see added to the list that would be supportive of lean objectives.arrow_forwardWhich of the following underlying assumptions form(s) the basis for grossprofit variance analysis? A. Sales and costs behave in a linear manner.B. Costs can be categorized as variable.C. All of the choices are assumptions that underlie gross profit variance analysis.D. In multiproduct organizations, the sales mix remains discretionary.arrow_forward

- Which of the following statements is false? Standard costs (e.g., how much should be paid for each unit of input) are benchmarks for measuring performance. Managers should investigate only unfavorable variances. Variance analysis enhances responsibility accounting. A variance is the difference between the budgeted amount and actual amount.arrow_forward1) Why do companies develop flexible budgets for variance analysis? Because actual activity level may not be the same as the budgeted activity level. Because flexible budgets reflect the normal production capacity. Because flexible budgets are more accurate than static budgets. Because static budgets become obsolete in the end of year when variance analysis are performed. 2) If excessive direct hours are used in the current operations, what variance would be resulted under the standard cost accounting? Unfavorable labor efficiency variance Favorable labor quality variance Favorable labor efficiency variance Unfavorable labor rate variance 3) The following actual and standard cost data for direct material and direct labor relate to the production of 4,000 units of product: Actual Costs Standard Costs Direct Material 4,900 lb. $5.85 per pound 5,000 lb. $5.90 per pound Direct Labor 1,900 hrs. $20.50 per hour 2,000 hrs. $20.00 per hour What is the materials price…arrow_forwardThe performance evaluation of a cost center is typically based on its a. sales volume variance. b. ROI. c. static budget variance. d. flexible budget variance.arrow_forward

- Which of the following statement(s) is/are true regarding standard costs and cost variances? i. they can be used in performance evaluation of managers and divisions. ii. management by exception is used by managers in deciding whether to investigate cost variances. iii. variance investigation involves looking at only unfavourable variances. iv. a shorter product life cycle means that standard cost data are only relevant for a shorter time period. v. using unskilled workers may result in a favourable labour efficiency variance. Multiple Choice i, ii, iii, iv and v i and ii i only i, iii and v i, ii and ivarrow_forward9. A company using direct costing in its performance evaluation would normally include the following variance in its report, except a)Budget variance b)Price variance c)Efficiency variance d)Volume variancearrow_forwardWhich of the following about gross profit variance analysis is most correct? a. Results of the gross variance analysis should be published at least annually to improve the company’s transparency. b. All of the choices are correct. c. Gross profit variance analysis is a management tool used to track gross profit and improve its performance and profitability in the future. d. A zero-gross profit variance absolutely indicates that the company is able to sell its products at the same price and at the same volume as budgeted or as previous year’s.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...

Accounting

ISBN:9781337115773

Author:Maryanne M. Mowen, Don R. Hansen, Dan L. Heitger

Publisher:Cengage Learning

Principles of Cost Accounting

Accounting

ISBN:9781305087408

Author:Edward J. Vanderbeck, Maria R. Mitchell

Publisher:Cengage Learning

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

What is Risk Management? | Risk Management process; Author: Educationleaves;https://www.youtube.com/watch?v=IP-E75FGFkU;License: Standard youtube license