Fundamentals Of Cost Accounting (6th Edition)

6th Edition

ISBN: 9781259969478

Author: WILLIAM LANEN, Shannon Anderson, Michael Maher

Publisher: McGraw Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 18, Problem 55P

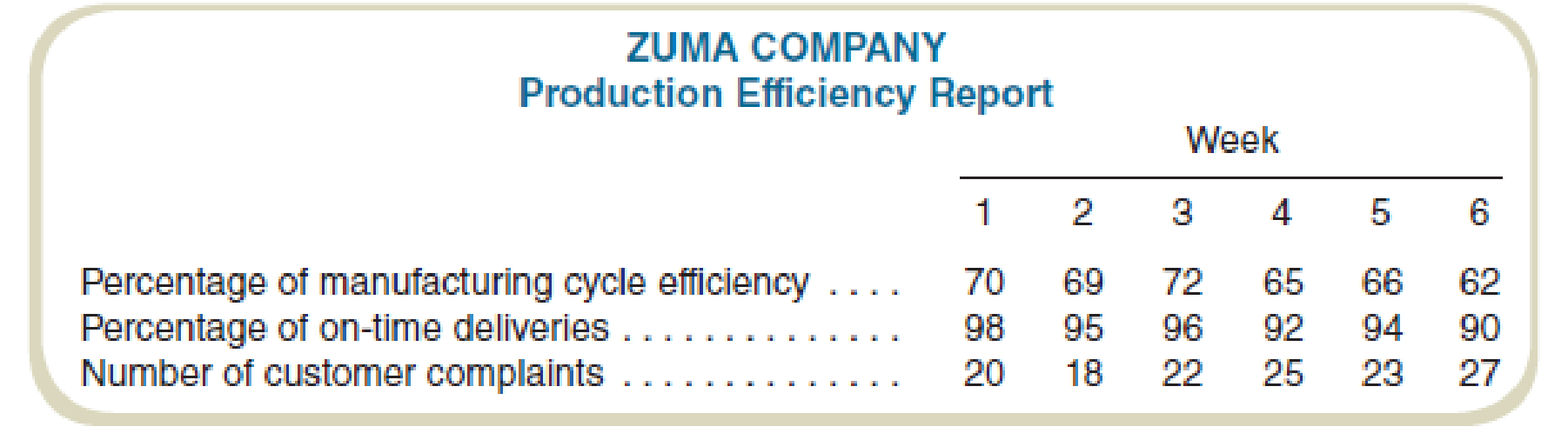

Operational Performance Measures

Zuma Company manufactures surfboards. The controller prepares a weekly production efficiency report and sends it to corporate headquarters. The data compiled in these reports for a recent six-week period follow:

Required

- a. Write a memo to the company president evaluating the plant’s performance.

- b. If you identify any areas of concern in your memo, indicate an appropriate action for management to take. Indicate any additional information you would like to have to make your evaluation.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Measures of Internal Business Process Performance

DataSpan. Inc., automated its plant at the start of the current year and installed a flexible manufacturing system. The company is also evaluating its suppliers and moving toward Lean Production. Many adjustment problems have been encountered, including problems relating to performance measurement. After much study, the company has decided to use the performance measures below, and it has gathered data relating to these measures for the first four months of operations.

Management has asked for your help in computing throughput time, delivery cycle time, and MCE. The following average times have been logged over the last four months:

Required:

1. For each month, compute the following:

a. The throughput time.

b. The delivery cycle time.

c. The manufacturing cycle efficiency (MCE).

2. Evaluate the company’s performance over the last four months.

3. Refer to the move lime, process time, and so forth, given above for month 4.

a. Assume that…

In August, Lannister Company introduced a new performance measurement system in manufacturing operations. One of the new performance measures is lead time, which is determined by tagging a random sample of items with a log sheet throughout the mouth. The log sheets recorded the time that the sample items started production and the time that they ended production, as well as all steps in between. At the end of the month, the controller collected the log sheets and calculated the average lead time of the tagged products. This number was reported to central management and was used to evaluate the performance of the plant manager. Because of the poor lead time results reported for August, the plant was under extreme pressure to reduce lead time in September.

The following memo was intercepted by the controller.

Date: September 3

To: Hourly Employees

From: Plant Manager

During last month, you may have noticed that some of the products were tagged with a log sheet. This sheet…

Ethics Case. At Symond Company, production workers in the Painting Department are paid on the basis of productivity. The labor time standard for a unit of production is established through periodic time studies conducted by Douglas Management Consultants. In a time actual time required to complete a specific task by a worker is observed. Allowances are then made for preparation time, rest periods, and cleanup time. Bill Carson is one of several veterans in the Painting Department .Bill is informed by Douglas that he will be used in the time study for the beginning of a new product . The findings will be the basis for establishing the labor time standard of the next 6 months.During the test, Bill deliberately slows his normal work pace in an effort to obtain a labor time standard that will be easy to meet. Because it is a new product, the Douglas representatives who conducted the test is unaware that Bill did not give the test his best effort.

Chapter 18 Solutions

Fundamentals Of Cost Accounting (6th Edition)

Ch. 18 - Why is it important for management accountants to...Ch. 18 - A balanced scorecard is a set of two or more...Ch. 18 - What is a business model?Ch. 18 - What are the advantages of financial measures of...Ch. 18 - Prob. 5RQCh. 18 - Why do effective performance evaluation systems...Ch. 18 - What is benchmarking?Ch. 18 - Prob. 8RQCh. 18 - Prob. 9RQCh. 18 - Prob. 10RQ

Ch. 18 - Prob. 11RQCh. 18 - Prob. 12RQCh. 18 - Prob. 13RQCh. 18 - Prob. 14RQCh. 18 - Prob. 15RQCh. 18 - Prob. 16CADQCh. 18 - Prob. 17CADQCh. 18 - Prob. 18CADQCh. 18 - Prob. 19CADQCh. 18 - Prob. 20CADQCh. 18 - Prob. 21CADQCh. 18 - Prob. 22CADQCh. 18 - Prob. 23CADQCh. 18 - Prob. 24CADQCh. 18 - Strategy and Management Accounting Systems Joes...Ch. 18 - Business Strategy Classification Consider the...Ch. 18 - Prob. 27ECh. 18 - Prob. 28ECh. 18 - Prob. 29ECh. 18 - Prob. 30ECh. 18 - Balanced Scorecards and Strategy Maps Crane...Ch. 18 - TechMasters, Inc., has the following mission...Ch. 18 - Benchmarks Match each of the following specific...Ch. 18 - Benchmarks Match each of the following specific...Ch. 18 - Prob. 35ECh. 18 - Manufacturing Cycle Time and Efficiency Bell ...Ch. 18 - Prob. 37ECh. 18 - Partial Productivity Measures Looking for cost...Ch. 18 - Partial Productivity Measures As the cost...Ch. 18 - Prob. 40ECh. 18 - Prob. 41ECh. 18 - Specifying Nonfinancial Measures Write a memo to...Ch. 18 - Manufacturing Cycle Time and Efficiency A...Ch. 18 - Prob. 44ECh. 18 - Core Assets and Capabilities Consider the...Ch. 18 - Write a memo discussing the advantages of each...Ch. 18 - Balanced Scorecards and Strategy Maps Hill Street...Ch. 18 - Balanced Scorecards and Strategy Maps Monroe...Ch. 18 - Benchmarks Write a report to the CEO of Delta...Ch. 18 - Prob. 50PCh. 18 - Performance Measures, Drawing a Business Model...Ch. 18 - Performance Measures, Drawing a Business Model...Ch. 18 - Functional Measures Write a report to the...Ch. 18 - Prob. 54PCh. 18 - Operational Performance Measures Zuma Company...Ch. 18 - Objective and Subjective Performance Measures A...Ch. 18 - Operational Performance Measures Mid-States Metal...Ch. 18 - Prob. 58PCh. 18 - Prob. 59PCh. 18 - Prob. 60PCh. 18 - Balanced Scorecards and Strategy Maps Following...

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Pareto chart and cost of quality report for a manufacturing company The president of Mission Inc. has been concerned about the growth in costs over the last several years. The president asked the controller to perform an activity analysis to gain a better insight into these costs. The activity analysis revealed the following: The production process is complicated by quality problems, requiring the production manager to expedite production and dispose of scrap. Instructions 1. Prepare a Pareto chart of the company activities. 2. Classify the activities into prevention, appraisal, internal failure, external failure, and not costs of quality (producing product). Classify the activities into value-added and non-value-added activities. 3. Use the activity cost information to determine the percentages of total costs that are prevention, appraisal, internal failure, external failure, and not costs of quality. 4. Determine the percentages of total costs that are value-added and non-value-added. 5. Interpret the information.arrow_forwardCommunications Jamarcus Bradshaw, plant manager of Georgia Paper Companys papermaking mill, was looking over the cost of production reports for July and August for the Papermaking Department. The reports revealed the following: Jamarcus was concerned about the increased cost per ton from the output of the department. As a result, he asked the plant controller to perform a study to help explain these results. The controller, Leann Brunswick, began the analysis by performing some interviews of key plant personnel in order to understand what the problem might be. Excerpts from an interview with Len Tyson, a paper machine operator, follow: Len: We have two papermaking machines in the department. I have no data, but I think paper machine No. 1 is applying too much pulp and, thus, is wasting both conversion and materials resources. We haven't had repairs on paper machine No. 1 in a while. Maybe this is the problem. Leann: How does too much pulp result in wasted resources? Len: Well, you see, if too much pulp is applied, then we will waste pulp material. The customer will not pay for the extra product; we just use more material to make the product. Also, when there is too much pulp, the machine must be slowed down in order to complete the drying process. This results in additional conversion costs. Leann: Do you have any other suspicions? Len: Well, as you know, we have two productsgreen paper and yellow paper. They are identical except for the color. The color is added to the papermaking process in the paper machine. I think that during August these two color papers have been behaving very differently. I don't have any data, but it just seems as though the amount of waste associated with the green paper has increased. Leann: Why is this? Len: I understand that there has been a change in specifications for the green paper, starting near the beginning of August. This change could be causing the machines to run poorly when making green paper. If this is the case, the cost per ton would increase for green paper. Leann also asked for a database printout providing greater detail on Augusts operating results. September 9 Requested by: Leann Brunswick Papermaking DepartmentAugust detail Prior to preparing a report, Leann resigned from Georgia Paper Company to start her own business. You have been asked to take the data that Leann collected, and write a memo to Jamarcus Bradshaw with a recommendation to management. Your memo should include analysis of the August data to determine whether the paper machine or the paper color explains the increase in the unit cost from July. Include any supporting schedules that are appropriate. Round any calculations to the nearest cent.arrow_forwardJoseph Fox, controller of Thorpe Company, has been in charge of a project to install an activity-based cost management system. This new system is designed to support the companys efforts to become more competitive. For the past six weeks, he and the project committee members have been identifying and defining activities, associating workers with activities, and assessing the time and resources consumed by individual activities. Now, he and the project committee are focusing on three additional implementation issues: (1) identifying activity drivers, (2) assessing value content, and (3) identifying cost drivers (root causes). Joseph has assigned a committee member the responsibilities of assessing the value content of five activities, choosing a suitable activity driver for each activity, and identifying the possible root causes of the activities. Following are the five activities with possible activity drivers: The committee member ran a regression analysis for each potential activity driver, using the method of least squares to estimate the variable and fixed cost components. In all five cases, costs were highly correlated with the potential drivers. Thus, all drivers appeared to be good candidates for assigning costs to products. The company plans to reward production managers for reducing product costs. Required: 1. What is the difference between an activity driver and a cost driver? In answering the question, describe the purpose of each type of driver. 2. For each activity, assess the value content and classify each activity as value-added or non-value-added (justify the classification). Identify some possible root causes of each activity, and describe how this knowledge can be used to improve activity performance. For purposes of discussion, assume that the value-added activities are not performed with perfect efficiency. 3. Describe the behavior that each activity driver will encourage, and evaluate the suitability of that behavior for the companys objective of becoming more competitive.arrow_forward

- For each of the activities listed, choose the manufacturing concept that applies: (i) just-in-time inventory, (ii) continuous improvement, or (iii) total quality management. A company receives inventory daily based on customer orders. Manufacturing factories have been arranged in such a fashion to reduce inefficiencies. Companies organize customer focus groups in order to look at customer needs and expectations. The entire production process is standardized and written down with procedures. Each customer receives a survey of satisfaction with their product. All orders are complete and shipped within three business days.arrow_forwardIndicate whether the statement describes reporting by the financial accounting function or the managerial accounting function of an organization. The users of the report are managers who need a daily summary of work done each shift. The report is a job cost sheet for jobs completed in a 24-hour period. The annual report is released each year on the companys website. The report is audited by the companys certified public accountant firm. The report is prepared every day because the customer service manager needs information about inventory ready to be shipped to customers.arrow_forwardGreiner Company makes and sells high-quality glare filters for microcomputer monitors. John Craven, controller, is responsible for preparing Greiners master budget and has assembled the following data for the coming year. The direct labor rate includes wages, all employee-related benefits, and the employers share of FICA. Labor saving machinery will be fully operational by March. Also, as of March 1, the companys union contract calls for an increase in direct labor wages that is included in the direct labor rate. Greiner expects to have 5,600 glare filters in inventory on December 31 of the current year, and has a policy of carrying 35 percent of the following month's projected sales in inventory. Information on the first four months of the coming year is as follows: Required: 1. Prepare the following monthly budgets for Greiner Company for the first quarter of the coming year. Be sure to show supporting calculations. a. Production budget in units b. Direct labor budget in hours c. Direct materials cost budget d. Sales budget 2. Calculate the total budgeted contribution margin for Greiner Company by month and in total for the first quarter of the coming year. Be sure to show supporting calculations. (CMA adapted)arrow_forward

- D: Measures of Internal Business Process PerformanceDataSpan, Inc., automated its plant at the start of the current year and installed a flexiblemanufacturing system. The company is also evaluating its suppliers and moving toward LeanProduction. Many adjustment problems have been encountered, including problems relating toperformance measurement. After much study, the company has decided to use the performancemeasures below, and it has gathered data relating to these measures for the first four months ofoperations.Month1 2 3 4Throughput time (days) ? ? ? ?Delivery cycle time (days) ? ? ? ?Manufacturing cycle efficiency (MCE) ? ? ? ?Percentage of on-time deliveries 91% 86% 82% 78%Total sales (units) 3460 3312 3143 3025Management has asked for your help in computing throughput time, delivery cycle time, and MCE.The following average times have been logged over the last four months: Average per Month (in days)1 2 3 4Move time per unit 0.7 0.5 0.6 0.6Process time per unit 2.8 2.7 2.6…arrow_forwardFollowing items belong to the revenue, expenditure, human resources/payroll, production, or financing cycle. Classify each item based on the cycle it belongs to. a. Pay pay-as-you-earn (PAYE) payroll taxes b. Send material requisition to inventory c. Issue stock to investors d. Borrow money from the bank to purchase a new factory e. Complete receiving report f. Appoint replacement purchasing clerk g. Measure employee performance using a performance management system h. Choose suitable supplier of raw materials i. Ensure employees are up to date with the latest tax provisions j. Record personal and tax information for new employeesarrow_forwardProblem: Ethics in Business Lisa Ronsin had recently been transferred to the Home Security Systems Division of National Home Products. Shortly after taking over her new position as divisional controller, she was asked to develop the division’s predetermined overhead rate for the upcoming year. The accuracy of the rate is important because it is usedthroughout the year and any underapplied or overapplied overhead is closed out to Cost of Goods Sold at the end of the year. National Home Products uses direct labor- hours in all of its divisions as the allocation base formanufacturing overhead. To compute the predetermined overhead rate, Lisa divided her estimate of the total manufacturing overhead for the coming year by the production manager’s estimate of the total direct labor-hours for the coming year. She took her computations to the division’s general manager for approval but was quite surprised when he suggested amodification in the base. Her conversation with the general manager…arrow_forward

- Pareto Chart and Cost of Quality Report for a Manufacturing Company The president of Mission Inc. has been concerned about the growth in costs over the last several years. The president asked the controller to perform an activity analysis to gain a better insight into these costs. The activity analysis revealed the following. The production process is complicated by quality problems, requiring the production manager to expedite production and dispose of scrap. Required: 1. Classify the activities into prevention, appraisal, internal failure, external failure, and not costs of quality (producing product). Classify the activities into value-added and non-value added activities. Activity Activity Cost Cost of Quality Classification VA/NVA Correcting invoice errors $7,500 Disposing of incoming materials with poor quality 15,000 Disposing of scrap 27,500 Expediting late production 22,500 Final inspection 20,000 Inspecting incoming…arrow_forwardEthics and quality. Weston Corporation manufactures auto parts for two leading Japanese automakers. Nancy Evans is the management accountant for one of Weston’s largest manufacturing plants. The plant’s general manager, Chris Sheldon, has just returned from a meeting at corporate headquarters where quality expectations were outlined for 2017. Chris calls Nancy into his office to relay the corporate quality objective that total quality costs will not exceed 10% of total revenues by plant under any circumstances. Chris asks Nancy to provide him with a list of options for meeting corporate headquarters’ quality objective. The plant’s initial budgeted revenues and quality costs for 2017 are as follows: Revenue 5,100,000 Quality costs: Testing of purchased materials 48,000 Quality control training for production staff 7,500 Warranty repairs 123,000 Quality design engineering 72,000 Customer support 55,500 Materials scrap 18,000 Product inspection 153,000 Engineering redesign of failed parts…arrow_forwardEthics and quality. Weston Corporation manufactures auto parts for two leading Japanese automakers. Nancy Evans is the management accountant for one of Weston’s largest manufacturing plants. The plant’s general manager, Chris Sheldon, has just returned from a meeting at corporate headquarters where quality expectations were outlined for 2017. Chris calls Nancy into his office to relay the corporate quality objective that total quality costs will not exceed 10% of total revenues by plant under any circumstances. Chris asks Nancy to provide him with a list of options for meeting corporate headquarters’ quality objective. The plant’s initial budgeted revenues and quality costs for 2017 are as follows: Revenue 5,100,000 Quality costs: Testing of purchased materials 48,000 Quality control training for production staff 7,500 Warranty repairs 123,000 Quality design engineering 72,000 Customer support 55,500 Materials scrap 18,000 Product inspection 153,000 Engineering redesign of failed parts…arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Managerial Accounting

Accounting

ISBN:9781337912020

Author:Carl Warren, Ph.d. Cma William B. Tayler

Publisher:South-Western College Pub

Financial And Managerial Accounting

Accounting

ISBN:9781337902663

Author:WARREN, Carl S.

Publisher:Cengage Learning,

Principles of Accounting Volume 2

Accounting

ISBN:9781947172609

Author:OpenStax

Publisher:OpenStax College

Cornerstones of Cost Management (Cornerstones Ser...

Accounting

ISBN:9781305970663

Author:Don R. Hansen, Maryanne M. Mowen

Publisher:Cengage Learning

Ethical Decision Making in Management; Author: GreggU;https://www.youtube.com/watch?v=6UrBO-cL27Q;License: Standard Youtube License