Concept explainers

Videos

Balanced Scorecards and Strategy Maps

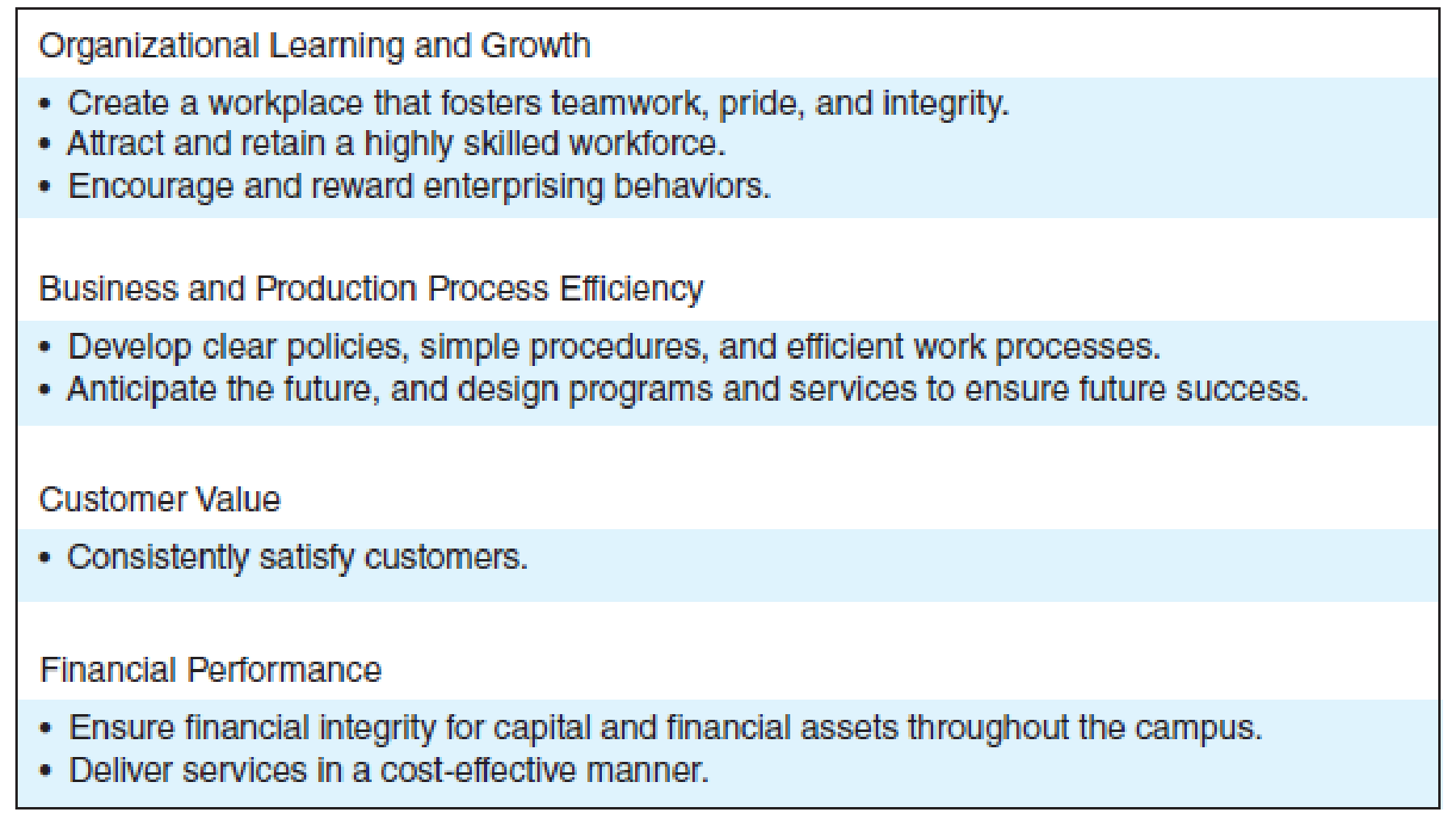

Following several years of tight budgets, administrators at the University of California, Davis, looked for ways “to do more with less.” Janet Hamilton, vice chancellor of administration, researched books and articles, met with consultants, and talked to her counterparts at universities across the United States to find new management methods that could change the university from a bureaucratic organization to one that is customer-oriented. She learned about reengineering, total quality, and a variety of other management techniques. None of the management techniques appealed to her, until she came across articles about the balanced scorecard. She believed that the balanced scorecard was the right tool for the Davis campus, and she set about implementing it.

At first, Hamilton did not call her approach a “balanced scorecard,” because she feared that employees would think of this as just another management fad to endure until the administration went on to something new. Instead, she pilot-tested the balanced scorecard ideas in one service department, environmental health and safety (EHS), until it worked. With the success of EHS behind her, she moved to implement the balanced scorecard in other service departments, such as police, fire, and printing services.

Each department developed its own particular performance measures to achieve the following objectives (we have shortened the list to save space):

Required

- a. Was the vice chancellor overly cautious in not calling her approach a “balanced scorecard”?

- b. Comment on the wisdom of beginning a balanced scorecard with a pilot project. Would it be possible to extrapolate the experience of a service department, such as environmental health and safety, to an academic unit, such as a college of business?

- c. What opportunities and difficulties do you see in applying a balanced scorecard to a university setting?

Want to see the full answer?

Check out a sample textbook solution

Chapter 18 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Scorecard Measures, Strategy Translation At the end of 20x1, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Mejorar undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Mejorar wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered: 20x1 20x3 Theoretical annual capacity* 249,600 249,600 Actual production** 208,000 234,000 Market size (in units sold) 1,300,000 1,300,000 Production hours available (40 workers) 104,000 104,000 Very satisfied customers 62,400 117,000 Actual cost per unit $340 $272 Days of inventory 14 7 Number of defective…arrow_forwardScorecard Measures, Strategy Translation At the end of 20x1, Mejorar Company implemented a low-cost strategy to improve its competitive position. Its objective was to become the low-cost producer in its industry. A Balanced Scorecard was developed to guide the company toward this objective. To lower costs, Mejorar undertook a number of improvement activities such as JIT production, total quality management, and activity-based management. Now, after two years of operation, the president of Mejorar wants some assessment of the achievements. To help provide this assessment, the following information on one product has been gathered: 20x1 20x3 Theoretical annual capacity* 249,600 249,600 Actual production** 208,000 234,000 Market size (in units sold) 1,300,000 1,300,000 Production hours available (40 workers) 104,000 104,000 Very satisfied customers 62,400 117,000 Actual cost per unit $340 $272 Days of inventory 14 7 Number of defective…arrow_forwardDetermine if the selection of system 1 or 2 is sensitive to variation in the return required by management. The corporate MARR ranges from 8% to16% per year on different projects. Use tabulated factors or a spreadsheet, as requested by your instructor.arrow_forward

- Mastery Problem: Evaluating Decentralized Operations BOR CPAs, Inc. BOR, a decentralized organization, is interested in evaluating the performance of the two divisions. The stockholders are responsible for deciding on investment in the two divisions. Cyrus Bailey is in charge of the performance evaluation, and turns to you for assistance. Mr. Bailey is only interested in evaluating operations at the profit center (division) level, and not at the cost center (department) level. Mr. Bailey is considering temporarily using some of the staff from the Tax Division to assist the Audit Division during the upcoming busy audit season, and would like to evaluate the effect of this on net income. The Tax Division is estimated to have 800 hours of excess capacity. The unit for determining sales revenue in both divisions is the "engagement", which means the total agreed-upon work for a given client in either audit or tax for a given year. The company charges on average a fee of $75,000 per…arrow_forwardEye Swear Inc. has a balanced scorecard that includes the following relationships: Actual results for this year and last year are as follows: Instructions 1.Analyze these statistics to verify whether they support the expected relationships between the strategic objectives and performance metrics. 2.Identify three possible reasons for any unsupported relationship you identified in part (1). 3.Which of the three possibilities you identified in part (2) is the most likely reason for the unsupported relationship you identified in part (1)?arrow_forwardHyperflash Inc. has a balanced scorecard that includes the following relationships: Actual results for this month and last month are as follows: Instructions 1.Analyze these data to verify whether they support the expected relationship between the strategic objectives and performance metrics. 2.Identify three possible reasons for any unsupported relationship you identified in part (1). 3.Which of the three possibilities you identified in part (2) is the most likely reason for the unsupported relationship you identified in part (1)?arrow_forward

- Coral Creations has strategic plans that call for rapid growth, a limited number of units for each design to enhance exclusivity, designs for the perfect fit, on-time delivery to customers, retention of highly trained employees with innovative skills, and excellent inventory control. A. Suggest one performance measure for each dimension of the balanced scorecard for Coral Creations. B. Take one of your measures and discuss the linkage it has to multiple strategies in Corals plan.arrow_forwardFlexible budgeting, performance measurement, and ethics Montevideo Manufacturing, Inc. produces a single type of small motor. The bookkeeper who does not have an in-depth understanding of accounting principles prepared the following performance report with the help of the production manager. In a conversation with the sales manager, the production manager was overheard saying, You sales guys really messed up our May performance, and it is only because production did such a great job controlling costs that we arent in even worse shape. Required: 1. Do you agree with the production manager that the manufacturing area did a good job of controlling costs? 2. Prepare a flexible budget for Montevideo Manufacturings expenses at the following activity levels: 45,000 units, 50,000 units, and 55,000 units. 3. Prepare a revised performance report, using the most appropriate flexible budget from (2) above. 4. Now what is your response to the production managers claim? 5. Assume that you have just been hired as the new accountant. You observe that the production manager is about to receive a large bonus based on the favorable materials, labor, and factory overhead variances indicated in the flexible budget prepared by the bookkeeper. Using the IMA Statement of Ethical Professional Practice as your guide, what standards, if any, apply to your responsibilities in this matter?arrow_forwardCarson Wellington, president of Mallory Plastics, was considering a report sent to him by Emily Sorensen, vice president of operations. The report was a summary of the progress made by an activity-based management system that was implemented three years ago. Significant progress had indeed been realized. At the conclusion of the report, Emily urged Carson to consider the adoption of the Balanced Scorecard as a logical next step in the companys efforts to establish itself as a leader in its industry. Emily clearly was impressed by the Balanced Scorecard and intrigued by the possibility that the change would enhance the overall competitiveness of Mallory. She requested a meeting of the executive committee to explain the similarities and differences between the two approaches. Carson agreed to schedule the meeting but asked Emily to prepare a memo in advance, listing the most important similarities and differences between the two approaches to responsibility accounting. Required: Prepare the memo requested by Carson.arrow_forward

- Instructions 1.Based on the balanced scorecard and the following descriptions of the predicted relationships between strategic objectives, draw the scorecards strategy map. a.Training employees effectively and reducing employee turnover can both be expected to improve returns processing and reduce shipping errors. b.Both improving returns processing and reducing shipping errors can be expected to delight the customer. c.Delighting the customer can be expected to increase market share. 2.Based on the balanced scorecard and the following descriptions of the predicted relationships between performance metrics, draw the scorecards measure map. a.Median training hours per employee and average employee tenure will both influence hours from returned to refunded and number of erroneous shipments. b.Both hours from returned to refunded and number of erroneous shipments will affect percentage of customers who shop again and online customer satisfaction rating. c.Both percentage of customers who shop again and online customer satisfaction rating will influence the companys market share. 3.Label each element of the balanced scorecard.arrow_forwardThe following if-then statements were taken from a Balanced Scorecard: a. If employee capabilities increase, then process time decreases. b. If process time decreases, then customer retention will increase. c. If customer retention increases, then market share will increase. d. If market share increases, then revenues will increase. Required: 1. Identify the lead and lag variables, and explain your reasoning. 2. Discuss the implications of Requirement 1 for the financial and learning and growth perspectives. 3. Using the first if-then statement, explain the concept of double-loop feedback.arrow_forwardCoulson and Company is a large retail business that has a firm-wide balanced scorecard. Recently, management has discussed the need for the balanced scorecard to be more relevant to each individual department of the company. Specifically, management wants to come up with unique scorecards for its Public Relations and Inventory Management departments. For both departments, management recognizes that properly and efficiently training employees is important. For these purposes, management gathers data on the median training hours per employee and new employee performance review ratings. For the Inventory Management Department, management is focused on reducing stockouts (running out of certain inventory items) and keeping accurate inventory counts. For these purposes, the company tracks the number of back orders and discrepancies between the physical and record counts of inventory, respectively. For the Public Relations Department, management is focused on improving the publics CSR image of the company and attracting new customers. Management measures these objectives using Forbes CSR Rating of Coulson and Company and the number of new customers, respectively. a. Identify the term for Coulson and Companys plan to create unique balanced scorecards for its individual departments. b. Draw the unique balanced scorecards of each department. Identify the departments common and unique measures, and include all the elements of the balanced scorecard that you can in your drawings, given the information provided.arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning