Intermediate Accounting

9th Edition

ISBN: 9781259722660

Author: J. David Spiceland, Mark W. Nelson, Wayne M Thomas

Publisher: McGraw-Hill Education

expand_more

expand_more

format_list_bulleted

Videos

Textbook Question

Chapter 20, Problem 20.10E

Change in

• LO20–3

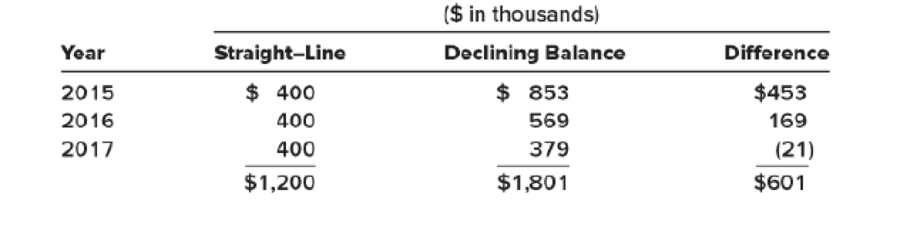

For financial reporting, Clinton Poultry Farms has used the declining-balance method of depreciation for conveyor equipment acquired at the beginning of 2015 for $2,560,000. Its useful life was estimated to be six years with a $160,000 residual value. At the beginning of 2018, Clinton decides to change to the straight-line method. The effect of this change on depreciation for each year is as follows:

Required:

- 1. Briefly describe the way Clinton should report this accounting change in the 2017–2018 comparative financial statements.

- 2. Prepare any 2018

journal entry related to the change.

Expert Solution & Answer

Want to see the full answer?

Check out a sample textbook solution

Students have asked these similar questions

Exercise 20-16 (Static) Accounting change [LO20-4]

The Peridot Company purchased machinery on January 2, 2019, for $800,000. A five-year life was estimated and no residual value was anticipated. Peridot decided to use the straight-line depreciation method and recorded $160,000 in depreciation in 2019 and 2020. Early in 2021, the company revised the total estimated life of the machinery to eight years.Required:1. What type of change is this?2. Is Peridot required to revise prior years’ financial statements as a result of the change?3. Is Peridot required to provide a disclosure note to report the change?4. Determine depreciation for 2021.

P11.1

(LO 2 ) (Depreciation for Partial Period—SL, SYD, and DDB) Alladin Company purchased Machine #201 on May 1, 2020. The following information relating to Machine #201 was gathered at the end of May.

Price

$85,000

Credit terms

2/10, n/30

Freight-in

$ 800

Preparation and installation costs

$ 3,800

Labor costs during regular production operations

$10,500

It is expected that the machine could be used for 10 years, after which the salvage value would be zero. Alladin intends to use the machine for only 8 years, however, after which it expects to be able to sell it for $1,500. The invoice for Machine #201 was paid May 5, 2020. Alladin uses the calendar year as the basis for the preparation of financial statements.

Instructions

a.

Compute the depreciation expense for the years indicated using the following methods. (Round to the nearest dollar.)

1.Straight-line method for 2020.

2.Sum-of-the-years'-digits method for 2021.…

P10.1

(LO 1 ) (Classification of Acquisition and Other Asset Costs) At December 31, 2019, certain accounts included in the property, plant, and equipment section of Reagan Company's balance sheet had the following balances.

Land

$230,000

Buildings

890,000

Leasehold improvements

660,000

Equipment

875,000

During 2020, the following transactions occurred.

1.Land site number 621 was acquired for $850,000. In addition, to acquire the land Reagan paid a $51,000 commission to a real estate agent. Costs of $35,000 were incurred to clear the land. During the course of clearing the land, timber and gravel were recovered and sold for $13,000.

2.A second tract of land (site number 622) with a building was acquired for $420,000. The closing statement indicated that the land value was $300,000 and the building value was $120,000. Shortly after acquisition, the building was demolished at a cost of $41,000. A new building was constructed for $330,000 plus the…

Chapter 20 Solutions

Intermediate Accounting

Ch. 20 - Prob. 20.1QCh. 20 - There are three basic accounting approaches to...Ch. 20 - Prob. 20.3QCh. 20 - Lynch Corporation changes from the...Ch. 20 - Sugarbaker Designs Inc. changed from the FIFO...Ch. 20 - Most changes in accounting principles are recorded...Ch. 20 - Southeast Steel, Inc., changed from the FIFO...Ch. 20 - Prob. 20.8QCh. 20 - Its not easy sometimes to distinguish between a...Ch. 20 - For financial reporting, a reporting entity can be...

Ch. 20 - Prob. 20.11QCh. 20 - Describe the process of correcting an error when...Ch. 20 - Prob. 20.13QCh. 20 - If it is discovered that an extraordinary repair...Ch. 20 - Prob. 20.15QCh. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in inventory methods; average cost method...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in depreciation methods LO203 Irwin, Inc.,...Ch. 20 - Prob. 20.5BECh. 20 - Book royalties LO204 Three programmers at Feenix...Ch. 20 - Warranty expense LO204 In 2017, Quapau Products...Ch. 20 - Change in estimate; useful life of patent LO204...Ch. 20 - Prob. 20.9BECh. 20 - Error correction LO206 In 2018, internal auditors...Ch. 20 - Prob. 20.11BECh. 20 - Error correction LO206 In 2018, the internal...Ch. 20 - Change in principle; change in inventory methods ...Ch. 20 - Change in principle; change in inventory methods ...Ch. 20 - Change from the treasury stock method to retired...Ch. 20 - Change in principle; change to the equity method ...Ch. 20 - Prob. 20.5ECh. 20 - FASB codification research LO202 Access the FASB...Ch. 20 - Change in principle; change in inventory cost...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in inventory methods; FIFO method to the...Ch. 20 - Change in depreciation methods LO203 For...Ch. 20 - Change in depreciation methods LO203 The Canliss...Ch. 20 - Book royalties LO204 Dreighton Engineering Group...Ch. 20 - Loss contingency LO204 The Commonwealth of...Ch. 20 - Warranty expense LO204 Woodmier Lawn Products...Ch. 20 - Prob. 20.15ECh. 20 - Accounting change LO204 The Peridot Company...Ch. 20 - Change in estimate; useful life and residual value...Ch. 20 - Classifying accounting changes LO201 through...Ch. 20 - Error correction; inventory error LO206 During...Ch. 20 - Error corrections; investment LO206 Required: 1....Ch. 20 - Prob. 20.21ECh. 20 - Prob. 20.22ECh. 20 - Prob. 20.23ECh. 20 - Inventory errors LO206 Indicate with the...Ch. 20 - Classifying accounting changes and errors LO201...Ch. 20 - Change in inventory costing methods; comparative...Ch. 20 - P 20-2 Change in principle; change in method of...Ch. 20 - Change in inventory costing methods; comparative...Ch. 20 - Change in inventory methods LO202 The Rockwell...Ch. 20 - Change in inventory methods LO202 Fantasy...Ch. 20 - Change in principle; change in depreciation...Ch. 20 - Depletion; change in estimate LO204 In 2018, the...Ch. 20 - Accounting changes; six situations LO201, LO203,...Ch. 20 - Prob. 20.9PCh. 20 - Inventory errors LO206 You have been hired as the...Ch. 20 - Error correction; change in depreciation method ...Ch. 20 - Accounting changes and error correction; seven...Ch. 20 - Prob. 20.13PCh. 20 - Prob. 20.14PCh. 20 - Prob. 20.15PCh. 20 - Prob. 20.16PCh. 20 - Prob. 20.17PCh. 20 - Integrating Case 201 Change to dollar-value LIFO ...Ch. 20 - Prob. 20.2BYPCh. 20 - Prob. 20.3BYPCh. 20 - Analysis Case 204 Change in inventory methods;...Ch. 20 - Prob. 20.5BYPCh. 20 - Prob. 20.6BYPCh. 20 - Analysis Case 208 Various changes LO201 through...Ch. 20 - Analysis Case 209 Various changes LO201 through...Ch. 20 - Prob. 20.10BYPCh. 20 - Prob. 20.11BYPCh. 20 - Prob. 20.12BYPCh. 20 - Prob. 1CCTC

Knowledge Booster

Learn more about

Need a deep-dive on the concept behind this application? Look no further. Learn more about this topic, accounting and related others by exploring similar questions and additional content below.Similar questions

- Exercise 8-25 (LO. 4) On April 5, 2020, Kinsey places in service a new automobile that cost $60,000. He does not elect § 179 expensing, and he elects not to take any available additional first-year depreciation. The car is used 70% for business and 30% for personal use in each tax year. Kinsey chooses the MACRS 200% declining-balance method of cost recovery (the auto is a 5-year asset). Click here to access the depreciation table to use for this problem. Assume the following luxury automobile limitations: year 1: $10,100; year 2: $16,100. Compute the total depreciation allowed for: 2020: $fill in the blank 1 2021: $fill in the blank 2 Exhibit 8.5 MACRS Straight-Line Depreciation for Personal Property Assuming Half-Year Convention For Property Placed in Service after December 31, 1986 Other Recovery Years Last Recovery Year MACRS Class % First Recovery Year Years % Year % 3-year 16.67 2–3 33.33 4 16.67 5-year 10.00 2–5 20.00 6…arrow_forwardQ.4 Swanson & Hiller, Inc., purchased a new machine on September 1, 2008 at a cost of $108,000. The machine’s estimated useful life at the time of the purchase was five years, and its residual value was $8,000. Instructions a. Prepare a complete depreciation schedule, beginning with calendar year 2008, under each of the methods listed below (assume that the half-year convention is used): 1. Straight-line. 2. 200 percent declining-balance. 3. 150 percent declining-balance, switching to straight-line when that maximizes the expense.arrow_forwardQ.5 R&R, Inc., purchased a new machine on September 1, 2009, at a cost of $180,000. The machine’s estimated useful life at the time of the purchase was five years, and its residual value was $10,000. Instructions Prepare a complete depreciation schedule, beginning with calendar year 2009, under each of the methods listed below (assume that the half-year convention is used): Straight-line. 200 percent declining-balance. 150 percent declining-balance (not switching to straight-line).arrow_forward

- Exercise 9.3 (Algo) Depreciation for Partial Years (LO9-3) On August 3, Cinco Construction purchased special-purpose equipment at a cost of $7,600,000. The useful life of the equipment was estimated to be eight years, with an estimated residual value of $20,000. a. Compute the depreciation expense to be recognized each calendar year for financial reporting purposes under the straight-line depreciation method (half-year convention). b. Compute the depreciation expense to be recognized each calendar year for financial reporting purposes under the 200 percent declining-balance method (half-year convention) with a switch to straight-line when it will maximize depreciation expense. c. Which of these two depreciation methods (straight-line or double-declinin.arrow_forwardIntermediate Accounting ll ch 16 5. On January 1, 2021, Ameen Company purchased major pieces of manufacturing equipment for a total of $48 million. Ameen uses straight-line depreciation for financial statement reporting and MACRS for income tax reporting. At December 31, 2023, the book value of the equipment was $42 million and its tax basis was $32 million. At December 31, 2024, the book value of the equipment was $40 million and its tax basis was $25 million. There were no other temporary differences and no permanent differences. Pretax accounting income for 2024 was $30 million. Required: Prepare the appropriate journal entry to record Ameen’s 2024 income taxes. Assume an income tax rate of 25%. What is Ameen’s 2024 net income?arrow_forwardProblem # 1 (30): Given: On Sep 1, 2017 General Assembly (GA) purchased for $980,000 an ANSONIA 7300 wide-corridor stacking modulator with the expectation that its economic life would be exhausted at 2024 12 31 and that the unit’s salvage value would be $320,000. On 2020 11 01 GA exchanged the equipment for a 4-year, zero-coupon note with a face value of $900,000. GA recognized a loss of $16,100 on the transaction. GA uses SLN for depreciation and prorating for partial periods. Required: Book the 12/31/2020 interest accrual for the note.arrow_forward

- CHPT#9_5 Depreciation Methods On January 2, 2018, Skyler, Inc. purchased a laser cutting machine to be used in the fabrication of a part for one of its key products. The machine cost $120,000, and its estimated useful life was four years or 920,000 cuttings, after which it could be sold for $5,000. Required a. Calculate each year’s depreciation expense for the machine's useful life under each of the following depreciation methods (round all answers to the nearest dollar):1. Straight-line.2. Double-declining balance.3. Units-of-production. (Assume annual production in cuttings of 200,000; 350,000; 260,000; and 110,000.)arrow_forwardEffect of depreciation on net income Tuttle Construction Co. specializes in building replicas of historic houses. Tim Newman, president of Tuttle Construction, is considering the purchase of various items of equipment on July 1, 2014, for 400,000. The equipment would have a useful life of five years and no residual value. In the past, all equipment has been leased. For tax purposes, Tim is considering depreciating the equipment, by the straight-line method. He discussed the matter with his CPA and learned that, although the straight-line method could be elected, it was to his advantage to use the Modified Accelerated Cost Recovery System (MACKS) for tax purposes, lie asked for your advice as to which method to use for tax purposes. 1. Compute depreciation for each of the years (2014, 2015, 2016, 2017, 2018, and 2019) of useful life by (a) the straight-line method and (b) MACRS. In using the straight-line method, one-half year's depreciation should be computed for 2014 and 2019.Use the MACRS rates presented in Exhibit 9. 2. Assuming that income before depreciation and income tax is estimated to be 750,000 uniformly per year and that the income tax rate is 40%, compute the net income for each of the years 2014, 2015, 2016, 2017, 2018, and 2019 if (a) the straight-line method is used and (b) MACRS is used. 3. What factors would you present for Tim's consideration in the selection of a depreciation method?arrow_forwardexercise 8-25 (LO. 4) On April 5, 2020, Kinsey places in service a new automobile that cost $60,000. He does not elect § 179 expensing, and he elects not to take any available additional first-year depreciation. The car is used 70% for business and 30% for personal use in each tax year. Kinsey chooses the MACRS 200% declining-balance method of cost recovery (the auto is a 5-year asset). Assume the following luxury automobile limitations: year 1: $10,100; year 2: $16,100. Compute the total depreciation allowed for: 2020: $ 2021: $arrow_forward

- Exercise 8-19 (LO. 2) Euclid acquires a 7-year class asset on May 9, 2020, for $80,000 (the only asset acquired during the year). Euclid does not elect immediate expensing under § 179. He does not claim any available additional first-year depreciation. Click here to access the depreciation table to use for this problem. If required, round your answers to the nearest dollar. Calculate Euclid's cost recovery deduction for 2020 and 2021.2020: $2021: $ 8-7cCost Recovery Tables Summary of Tables Exhibit 8.3 Regular MACRS table for personalty. Depreciation methods: 200 or 150 percent declining-balance switching to straight-line. Recovery periods: 3, 5, 7, 10, 15, 20 years. Convention: half-year. Exhibit 8.4 Regular MACRS table for personalty. Depreciation method: 200 percent declining-balance switching to straight-line. Recovery periods: 3, 5, 7 years. Convention: mid-quarter. Exhibit 8.5 MACRS optional straight-line table for personalty.…arrow_forwardProblem 7-51 (LO 7-5) Kwan acquired a warehouse for business purposes on August 30, 2002. The building cost $420,000. Kwan took $227,600 of depreciation on the building, and then sold it for $500,000 on July 1, 2021. Required: What is the adjusted basis for the warehouse? What amount of the gain or loss is realized on the sale of the warehouse? What amount of the gain or loss is unrecaptured? At what rate is the unrecaptured gain or loss taxed? What amount of the gain or loss qualifies as a § 1231 gain or loss?arrow_forwardCP 8‐4 Mayr Inc. purchased a machine for its factory on June 6, 2019 for $110,000. The machine is expected to have an estimated useful life of ten years with a salvage value of $10,000. Assume the company uses the ½ year rule to calculate depreciation expense in the year of acquisition and disposal. Required: Compute the depreciation for 2019 and 2020 using 1. The straight‐line method 2. The double‐declining balance method.arrow_forward

arrow_back_ios

SEE MORE QUESTIONS

arrow_forward_ios

Recommended textbooks for you

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial AccountingAccountingISBN:9781305653535Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial & Managerial AccountingAccountingISBN:9781285866307Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Accounting (Text Only)AccountingISBN:9781285743615Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Corporate Financial Accounting

Accounting

ISBN:9781305653535

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Financial & Managerial Accounting

Accounting

ISBN:9781285866307

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Accounting (Text Only)

Accounting

ISBN:9781285743615

Author:Carl Warren, James M. Reeve, Jonathan Duchac

Publisher:Cengage Learning

Depreciation -MACRS; Author: Ronald Moy, Ph.D., CFA, CFP;https://www.youtube.com/watch?v=jsf7NCnkAmk;License: Standard Youtube License