Videos

Variance interpretation

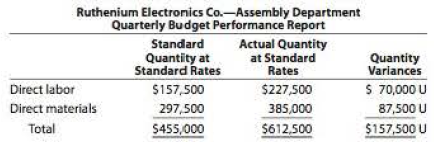

You have been asked to investigate some cost problems in the Assembly Department of Ruthenium Electronics Co., a consumer electronics company. To begin your investigation, you have obtained the following budget performance report for department for the last quarter:

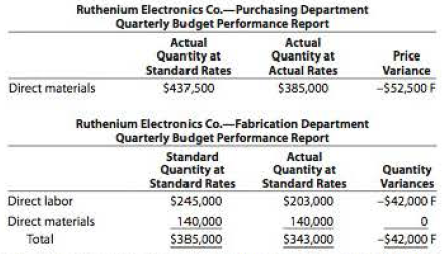

The following reports were also obtained:

You also interviewed the Assembly Department supervisor. Excerpts from the interview follow:

Q: What explains the poor performance in your department?

A: Listen, you've got to understand what it's been like in this department recently. Lately, it seems no matter how hard we try, we can't seem to make the standards. I'm not sure what is going on, but we've been having a lot of problems lately.

Q: What kind of problems?

A: Well, for instance, all this quarter we've been requisitioning purchased parts from the material storeroom, and the pans just didn't fit together very well I'm not sure what is going on. but during most of this quarter we've had to scrap and sort purchased pans—just to get our assemblies put together. Naturally, all this takes time and material. And that's not all.

Q: Go on.

A: All this quarter, the work that we've been receiving from the Fabrication Department has been shoddy. I mean, maybe around 20% of the stuff that comes in from Fabrication just can't be assembled. The fabrication is all wrong. As a result, we've had to scrap and rework a lot of the stuff. Naturally, this has just shot our quantity variances.

Interpret the variance reports in light of the comments by the Assembly Department supervisor.

Trending nowThis is a popular solution!

Chapter 22 Solutions

Financial & Managerial Accounting

- Flexible budgeting and variance analysis Im Really Cold Coat Company makes womens and mens coats. Both products require filler and lining material. The following planning information has been made available: Im Really Cold Coat Company does not expect there to be any beginning or ending inventories of filler and lining material. At the end of the budget year, Im Really Cold Coat Company experienced the following actual results: The expected beginning inventory and desired ending inventory were realized. Instructions 1. Prepare the following variance analyses for both coats and the total, based on the actual results and production levels at the end of the budget year: A. Direct materials price, quantity, and total variance. B. Direct labor rate, time, and total variance. 2. Why are the standard amounts in part (1) based on the actual production at the end of the year instead of the planned production at the beginning of the year?arrow_forwardVariance interpretation Vanadium Audio Inc. is a small manufacturer of electronic musical instruments. The plant manager received the following variable factory overhead report for the past month of operations: Actual units produced: 15,000 (90% of practical capacity) The plant manager is not pleased with the 12,320 unfavorable variable factory overhead controllable variance and has come to discuss the matter with the controller. The following discussion occurred: Plant Manager: I just received this factory report for the latest month of operations. Im not very pleased with these figures. Before these numbers go to headquarters, you and I need to reach an understanding. Controller: Go ahead. Whats the problem? Plant Manager: Whats the problem? Well, everything. Look at the variance. Its too large. If I understand the accounting approach being used here, you are assuming that my costs are variable to the units produced. Thus, as the production volume declines, so should these costs. Well, I dont believe these costs are variable at all. I think they are fixed costs. As a result, when we operate below capacity, the costs really dont go down. Im being penalized for costs I have no control over. I need this report to be redone to reflect this fact. If anything, the difference between actual and budget is essentially a volume variance. Listen, I know that youre a team player. You really need to reconsider your assumptions on this one. Assume you are the controller. Write a memo responding to the plant manager.arrow_forwardDirect labor time variance Maywood City Police uses variance analysis to monitor police staffing. The following table identifies three common police activities, the standard time to perform each activity, and their actual frequency to establish the expected cost to serve these activities. The police are paid 25 per hour. The actual amount of hours per activity for the year were as follows: A. Determine the total budgeted cost to perform the three police activities. B. Determine the total actual cost to perform the three police activities. C. Determine the direct labor time variance. D. What does the time variance suggest?arrow_forward

- Preparing a performance report Use the flexible budget prepared in P7-6 for the 31,000-unit level and the actual operating results listed below for the 31,000-unit level. Required: 1. Prepare a performance report. 2. List the major reasons why the actual operating income at 31,000 units differs from the master budget operating income at 30,000 units in Figure 7-12. 3. Given the level at which the company operated, how was its cost control? Item Direct materials: Direct labor:arrow_forwardRefer to Cornerstone Exercise 8.13. In March, Nashler Company produced 163,200 units and had the following actual costs: Required: 1. Prepare a performance report for Nashler Company comparing actual costs with the flexible budget for actual units produced. 2. What if Nashler Companys actual direct materials cost were 1,175,040? How would that affect the variance for direct materials? The total cost variance?arrow_forwardComputing materials variances D-List Calendar Co. specializes in manufacturing calendars that depict obscure comedians. The company uses a standard cost system to control its costs. During one month of operations, the direct materials costs and the quantities of paper used showed the following: Calculate the following: 1. Total cost of purchases for the month 2. Materials purchase price variance 3. Materials quantity variance 4. Net materials variancearrow_forward

- Refer to the data in Exercise 9.15. Required: 1. Compute overhead variances using a two-variance analysis. 2. Compute overhead variances using a three-variance analysis. 3. Illustrate how the two- and three-variance analyses are related to the four-variance analysis. Oerstman, Inc., uses a standard costing system and develops its overhead rates from the current annual budget. The budget is based on an expected annual output of 120,000 units requiring 480,000 direct labor hours. (Practical capacity is 500,000 hours.) Annual budgeted overhead costs total 787,200, of which 556,800 is fixed overhead. A total of 119,400 units using 478,000 direct labor hours were produced during the year. Actual variable overhead costs for the year were 230,600, and actual fixed overhead costs were 556,250. Required: 1. Compute the fixed overhead spending and volume variances. How would you interpret the spending variance? Discuss the possible interpretations of the volume variance. Which is most appropriate for this example? 2. Compute the variable overhead spending and efficiency variances. How is the variable overhead spending variance like the price variances of direct labor and direct materials? How is it different? How is the variable overhead efficiency variance related to the direct labor efficiency variance?arrow_forwardVariances Refer to Cornerstone Exercise 9.6. Required: 1. Calculate the variable overhead spending variance using the formula approach. (If you compute the actual variable overhead rate, carry your computations out to five significant digits and round the variance to the nearest dollar.) 2. Calculate the variable overhead efficiency variance using the formula approach. 3. Calculate the variable overhead spending variance and variable overhead efficiency variance using the three-pronged graphical approach. 4. What if 26,100 direct labor hours were actually worked in February? What impact would that have had on the variable overhead spending variance? On the variable overhead efficiency variance? Standish Company manufactures consumer products and provided the following information for the month of February: Required: 1. Calculate the fixed overhead spending variance using the formula approach. 2. Calculate the volume variance using the formula approach. 3. Calculate the fixed overhead spending variance and volume variance using the three-pronged graphical approach. 4. What if 129,600 units had actually been produced in February? What impact would that have had on the fixed overhead spending variance? On the volume variance?arrow_forwardFlexible budgeting, performance measurement, and ethics Montevideo Manufacturing, Inc. produces a single type of small motor. The bookkeeper who does not have an in-depth understanding of accounting principles prepared the following performance report with the help of the production manager. In a conversation with the sales manager, the production manager was overheard saying, You sales guys really messed up our May performance, and it is only because production did such a great job controlling costs that we arent in even worse shape. Required: 1. Do you agree with the production manager that the manufacturing area did a good job of controlling costs? 2. Prepare a flexible budget for Montevideo Manufacturings expenses at the following activity levels: 45,000 units, 50,000 units, and 55,000 units. 3. Prepare a revised performance report, using the most appropriate flexible budget from (2) above. 4. Now what is your response to the production managers claim? 5. Assume that you have just been hired as the new accountant. You observe that the production manager is about to receive a large bonus based on the favorable materials, labor, and factory overhead variances indicated in the flexible budget prepared by the bookkeeper. Using the IMA Statement of Ethical Professional Practice as your guide, what standards, if any, apply to your responsibilities in this matter?arrow_forward

- Factory overhead cost variance report Tannin Products Inc. prepared the following factory overhead cost budget for the Trim Department for July of the current year, during which it expected to use 20,000 hours for production: Tannin has available 25,000 hours of monthly productive capacity in the Trim Department under normal business conditions. During July, the Trim Department actually used 22,000 hours for production. The actual fixed costs were as budgeted. The actual variable overhead for July was as follows: Construct a factory overhead cost variance report for the Trim Department for July.arrow_forwardCalculating factory overhead: two variances Munoz Manufacturing Co. normally produces 10,000 units of product X each month. Each unit requires 2 hours of direct labor, and factory overhead is applied on a direct labor hour basis. Fixed costs and variable costs in factory overhead at the normal capacity are 2.50 and 1.50 per direct labor hour, respectively. Cost and production data for May follow: a. Calculate the flexible-budget variance. b. Calculate the production-volume variance. c. Was the total factory overhead under- or overapplied? By what amount?arrow_forwardRefer to the information for Cinturon Corporation on the previous page. Required: 1. Break down the total variance for materials into a price variance and a usage variance using the columnar and formula approaches. 2. CONCEPTUAL CONNECTION Suppose the Boise plant manager investigates the materials variances and is told by the purchasing manager that a cheaper source of leather strips had been discovered and that this is the reason for the favorable materials price variance. Quite pleased, the purchasing manager suggests that the materials price standard be updated to reflect this new, less expensive source of leather strips. Should the plant manager update the materials price standard as suggested? Why or why not?arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning

Excel Applications for Accounting PrinciplesAccountingISBN:9781111581565Author:Gaylord N. SmithPublisher:Cengage Learning