Concept explainers

Videos

Variance interpretation

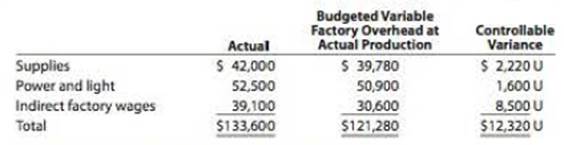

Vanadium Audio Inc. is a small manufacturer of electronic musical Instruments. The plant manager received the following variable factory overhead report for the period:

Actual units produced: 15,000 (90% of practical capacity)

The plant manager is not pleased with the $12,320 unfavorable variable factory overhead controllable variance and has come to discuss the matter with the controller. The following discussion occurred;

Plant Manager: I just received this factory report for the latest month of operator. I'm not very pleased with these figures. Before these numbers go to headquarters, you and I will need to reach an understanding.

Controller Go ahead, what's the problem?

Plant Manager: What's the problem? Well, everything. Look at the variance. It’s too large. If I understand the accounting approach being used here, you are assuming that my costs are variable to the units produced. Thus, as the production volume declines, so should these costs. Well I don't believe that these costs are variable at all. I think they are fixed costs. As a result when we operate below capacity, the costs really don't go down at all. I'm being penalized for costs I have no control over at all I need this report to be redone to reflect this fact, if anything, the difference between actual and budget is essentially a volume variance. Listen. I know that you're a tear-payer. You really need to reconsider your assumptions on this one.

If you were in the controller’s position, how would you respond to the plant manager?

Want to see the full answer?

Check out a sample textbook solution

Chapter 22 Solutions

EBK FINANCIAL & MANAGERIAL ACCOUNTING

- During June, the Conchran Manufacturing Company's costing system reported several variances that the production manager was surprised to see. Most of the company's monthly variances are under $125, even though they may be either favorable or unfavorable. The following information is for the manufacture of garden gates, its only product. (1) Direct materials price variance, S800 unfavorable. (2) Direct materials efficiency variance, $1,800 favorable. (3) Direct manufacturing labor price variance, $4,000 favorable. (4) Direct manufacturing labor efficiency variance, S600 unfavorable. Provide the manager with some ideas as to what may have caused the pricearrow_forwardQuality Motor Company is an auto repair shop that uses standards to control its labor time and labor cost. The standard labor cost for a motor tune-up is given below: Motor tune-up Standard Hours 2.50 The record showing the time spent in the shop last week on motor tune-ups has been misplaced. However, the shop supervisor recalls that 54 tune-ups were completed during the week, and the controller recalls the following variance data relating to tune-ups: Labor rate variance. Labor spending variance Standard Rate Standard Cost $72.50 $29.00 1. Actual labor hours 2. Actual hourly rate $ 120 F $ 170 U Required: 1. Determine the number of actual labor-hours spent on tune-ups during the week. 2. Determine the actual hourly pay rate for tune-ups last week. (Round your answer to 2 decimal places.) hours per hourarrow_forward[The following information applies to the questions displayed below.] The director of cost management for Odessa Company uses a statistical control chart to help management determine when to investigate variances. The critical value is 1 standard deviation. The company incurred the following direct-labor efficiency variances during the first six months of the current year. January February March. April May June $ 250 F 800 U 700 U 908 U 1,050 U 1,200 U The standard direct-labor cost during each of these months was $19,000. The controller has estimated that the firm's monthly direct-labor variances have a standard deviation of $950. Required: 1-a. Draw a statistical control chart and plot the variance data given above. 1-b. Which variances will be investigated?arrow_forward

- Critiquing a Variance Report; Preparing a Performance Report Several years ago, Westmont Corporation developed a comprehensive budgeting system for planning and control purposes. While departmental supervisors have been happy with the system, the factory manager has expressed considerable dissatisfaction with the information being generated by the system. A report for the company’s Assembly department for the month of march follows: After receiving a copy of this cost report, the supervisor of the assembly department started, “These reports are super. It makes me feel really good to see how well things are going in my department. I can’t understand why those people upstairs complain so much about the reports.” For the last several years, the company’s marketing department has chronically failed to meet the sales goals expressed in the company’s monthly budgets. Required: 1. The company’s president is uneasy about the cost reports and would like you to evaluate their usefulness to the…arrow_forwardAnders Painting Service specializes in painting tall office buildings. During a recent month, the company worked on three painting projects (the Arrow Building, the Besler Building and the Cartrwright Building). The company is interested in controlling the materials costs, namely the paint, used for these painting contracts. In order to provide management with useful cost control information, the company uses standard costs and prepares monthly variance reports. Analysis reveals that the purchasing agent mistakenly purchased poor-quality paint for the Arrow Building project. The Besler Building project, however, received higher-than-standard-quality paint that was on sale. The Cartwright Building project received standard-quality paint. However, the price had increased and a new employee was used to paint the building. Shown below are quantity and cost data for each project. Actual Project Arrow Building Besler Building Cartwright Building 4,500 Total variance Quantity 3,750 gallons…arrow_forwardGigil Company has asked you to reconstruct their record after a fire. You were given the following variances: Favorable Spending variance, P400,000; Unfavorable varaible effieciency variance, P200,000; Favorable Volume variance P40,000. Total fixed overhead is P200,000 at normal capacity. The company's standard variable overhead is P40 per direct labor hour. In the given period, the company incurred a total overhead cost of P2,400,000. Compute for the standard factory overhead rate.arrow_forward

- Vincent Bassani has come to the accounting department for help in interpreting his variance report. He says that he understands that last month was not a very good one for output, but he really thought everyone put forth good effort, so he is confused about the existence of an unfavorable labor efficiency variance. He cites as an example of the workers' effort their willingness to work extra hours to get full output, even when a whole week's worth of production had to be scrapped. He knew that his materials costs would be higher, and that overtime would make his rate variance unfavorable, but he certainly didn't think his workers had been inefficient. Required: Write a short note to Vincent explaining the probable cause of the unfavorable labor efficiency variancearrow_forwardLily Painting Service specializes in painting tall office buildings. During a recent month, the company worked on three painting projects (the Arrow Building, the Besler Building and the Cartrwright Building). The company is interested in controlling the materials costs, namely the paint, used for these painting contracts. In order to provide management with useful cost control information, the company uses standard costs and prepares monthly variance reports. Analysis reveals that the purchasing agent mistakenly purchased poor-quality paint for the Arrow Building project. The Besler Building project, however, received higher-than-standard-quality paint that was on sale. The Cartwright Building project received standard-quality paint. However, the price had increased and a new employee was used to paint the building. Shown below are quantity and cost data for each project. Project Arrow Building Besler Building Total variance (a) Cartwright Building 4,540 Project Arrow Building Besler…arrow_forwardLily Painting Service specializes in painting tall office buildings. During a recent month, the company worked on three painting projects (the Arrow Building, the Besler Building and the Cartrwright Building). The company is interested in controlling the materials costs, namely the paint, used for these painting contracts. In order to provide management with useful cost control information, the company uses standard costs and prepares monthly variance reports. Analysis reveals that the purchasing agent mistakenly purchased poor-quality paint for the Arrow Building project. The Besler Building project, however, received higher-than-standard-quality paint that was on sale. The Cartwright Building project received standard-quality paint. However, the price had increased and a new employee was used to paint the building. Shown below are quantity and cost data for each project. Project Arrow Building Costs 3,720 gallons $275,280 3,500 gallons $273,000 bring $290,320 4,000 $363,200 4,220…arrow_forward

- The auto repair shop of Quality Motor Company uses standards to control the labor time and labor cost in the shop. The standard labor cost for a motor tune-up is given below: Motor tune-up Standard Hours 2.50 The record showing the time spent in the shop last week on motor tune-ups has been misplaced. However, the shop supervisor recalls that 60 tune-ups were completed during the week, and the controller recalls the following variance data relating to tune-ups: Labor rate variance Labor spending variance Standard Rate Standard Cost $ 35.00 $ 87.50 1. Actual labor hours 2. Actual hourly rate $ 50 F $ 55 U Required: 1. Determine the number of actual labor-hours spent on tune-ups during the week. 2. Determine the actual hourly rate of pay for tune-ups last week. (Round your answer to 2 decimal places.) hours per hourarrow_forwardQuality Motor Company established the standard labor cost for a motor tune-up shown below: Standard Rate $ 25.00 Standard Cost $ 62.50 Motor tune-up Standard Hours 2.50 The record showing the time spent in the shop last week on motor tune-ups has been misplaced. However, the shop supervisor recalls 50 tune-ups were completed during the week, and the controller recalls the following variance data relating to tune-ups: Labor rate variance Labor spending variance Required: 1. Actual labor hours 2. Actual hourly rate $ 150 F $ 200 U 1. Determine the number of actual labor-hours spent on tune-ups during the week. 2. Determine the actual hourly pay rate for tune-ups last week. Note: Round your answer to 2 decimal places. hours per hourarrow_forwardKrueger Corporation in Washington, D.C., U.S., recently implemented a standard cost system. The company's cost accountant has gathered the following information needed to perform a variance analysis at the end of the month: Standard Cost Information Direct materials.... Quantity allowed per unit . Direct labor rate .... Hours allowed per unit.. Fixed overhead budgeted Normal level of production Variable overhead application rate Fixed overhead application rate ($12,000 _ 1,200 units) . .. 10.00 per unit Total overhead application rate.. $5 per pound .100 pounds per unit $20.00 per hour 2 hours per unit $12,000 per month . 1,200 units $ 2.00 per unit $12.00 per unit Actual Cost Information Cost of materials purchased and used .... Pounds of materials purchased and used. Cost of direct labor.... $468,000 .104,000 pounds $46,480 2,240 hours Hours of direct labor . anr$2,352 .$12,850 .1,000 units Cost of variable overhead . Cost of fixed overhead . Volume of production . Instructions 1.…arrow_forward

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning, Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 2AccountingISBN:9781947172609Author:OpenStaxPublisher:OpenStax College